Carding Forum

Professional

- Messages

- 2,788

- Reaction score

- 1,323

- Points

- 113

In a few months of 2021, the global cross-border payments market has changed more than in the last decade. This was discussed at Global Payments Day - a conference dedicated to the global payments market

Global Payments Day is a response to the explosive development of the cross-border payments market. For the first time, the conference was held last year, and today this topic is leading at the top financial events in the world and is fixed as a priority at the G20 level. The conference partners this year were the largest companies-leaders in the payment industry and innovations in the financial sector:

Global trends in the cross-border (global) payments market cover a fairly wide range of topics - from open banking to digital currencies.

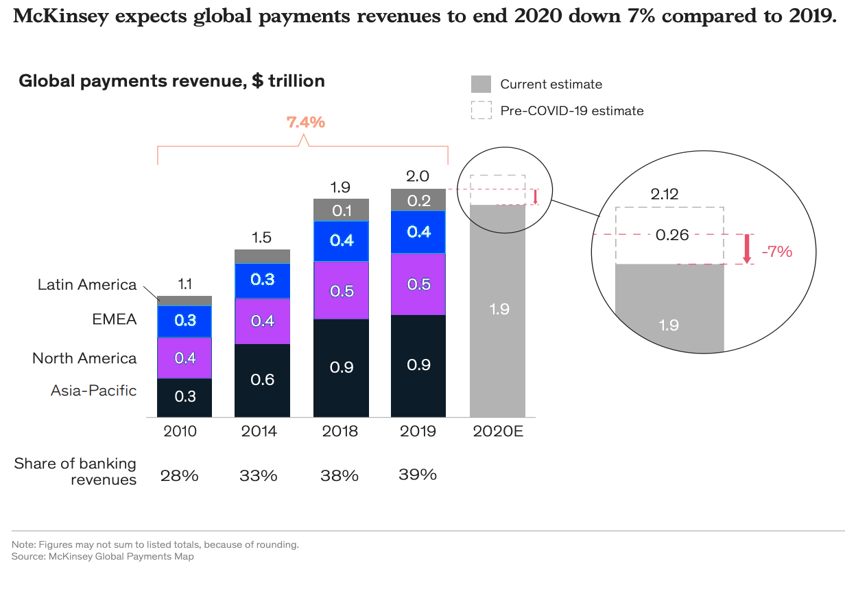

Covid19 has had a significant impact on the market. Closed borders, which have limited the flow of tourists and workers, have led to a 22% contraction in the volume and revenue of the cross-border payments market in the first half of this year. Although, the researchers believe, the second half of the year should be softer and the market will show only a 7% drop in revenues over the year (this is about $ 140 billion). In total, in 2019, revenues from the cross-border payments market amounted to $ 2 trillion.

At the same time, the study notes that the pandemic has significantly increased the importance of having fast, cheap and transparent global transactions and is driving innovation in this area and e-commerce. This is confirmed by the fact that this year the G20 has raised the priority of the development of cross-border payments, explaining this decision by the fact that this segment of the economy is very important for economic growth, global development and inclusion, especially considering that today global payments are more expensive, slower, not too available and less transparent than local ones.

Revenues from global payments, $ trillion

Against the backdrop of a global decline in global payments market revenues due to a ban on departures and a decrease in employment and volumes of tourism (business tourism), cross-border e-commerce has become an exception and has shown significant global growth. In the first half of 2020, consumers spent $ 347 billion online shopping from American retailers, up 30% from the same period in 2019. Amazon sales figures for Q2 2020 showed 40% growth compared to the same period in 2019 and a triple increase in sales in the grocery category. UPS and PayPal reported double growth in cross-border transactions and value of goods sold. According to Finanso.se, the European digital payments market will record a record $ 802 billion in 2020 (an increase of 9,

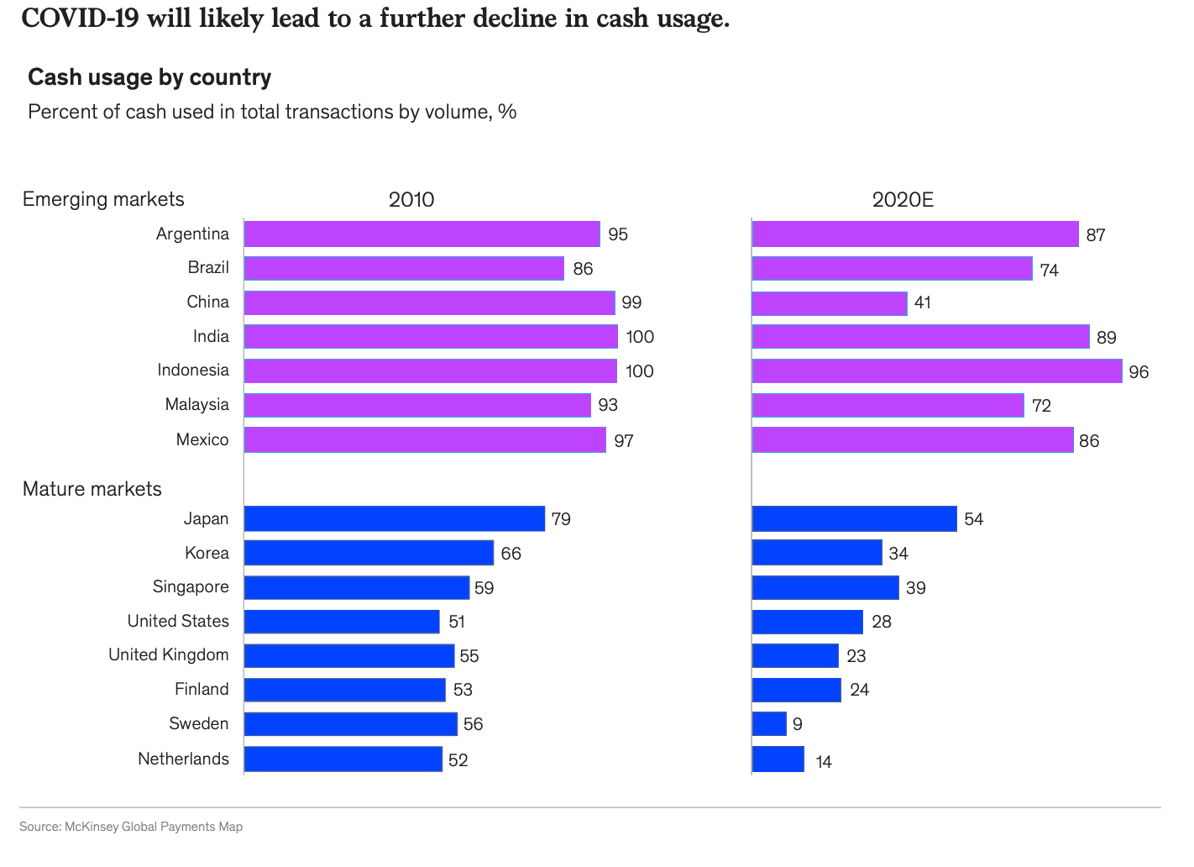

In general, the global crisis and the rapid change in consumer behavior have led to a rethinking of operating models in business around the world, to the growth of e-commerce and a reduction in cash transactions.

COVID-19 leads to a decrease in the use of cash in the world.

When will CBDCs go global.

Recommendations and foreign experience of CBDC development, which were shared by the regulators of Canada, France and China during the SIBOS payment conference:

Global Payments Day is a response to the explosive development of the cross-border payments market. For the first time, the conference was held last year, and today this topic is leading at the top financial events in the world and is fixed as a priority at the G20 level. The conference partners this year were the largest companies-leaders in the payment industry and innovations in the financial sector:

- Platinum Partner - Mastercard company

- General partner - Raiffeisen bank Aval

- Innovative partner - Concord Bank

- Partners - Adorsys and NovaPay

- Media partners: PaySpace Magazine, Banker Club, Ukrainian Fintech Hub, Fuete

“This market has changed a lot under the influence of the pandemic. Today, participants in the global payments market are changing operating models, investing in new technologies and striving to meet the needs of the “new normal” as much as possible. As a result, the rapid development of e-commerce, especially in mature markets with a developed fintech segment, the emergence of new cross-border financial products and the intensification of the role of central banks in issuing digital currencies (CBDC)”, - Keith Scheglova, co-organizer of the conference and TOP50 Fintech Global.

Global trends in the cross-border (global) payments market cover a fairly wide range of topics - from open banking to digital currencies.

Let's take a look at the main trends and drivers of the global payments market over the past years and this year to understand what to expect in the near future and in the years to come.“From the speakers' reports, we saw that all these topics are relevant for Ukraine as well. In particular, the NBU developed and submitted to Parliament the Law on Payment Services, market participants are already building a digital infrastructure based on API, the number of cross-border offers and market capacity are growing, and the financial regulator is expanding the range of innovative projects (including open banking, remote identification and verification, CBDC etc. etc.). So, we can say that the Ukrainian market is well prepared for the new normal and global trends in the global payments market, ”said Alexander Karpov, CEO of EMA.

Impact of the pandemic

Market size and cross-border transactions have grown steadily since 2011, according to a BIS study. At the same time, the researchers say, just a few months of this year have changed the market more than the last decade.Covid19 has had a significant impact on the market. Closed borders, which have limited the flow of tourists and workers, have led to a 22% contraction in the volume and revenue of the cross-border payments market in the first half of this year. Although, the researchers believe, the second half of the year should be softer and the market will show only a 7% drop in revenues over the year (this is about $ 140 billion). In total, in 2019, revenues from the cross-border payments market amounted to $ 2 trillion.

At the same time, the study notes that the pandemic has significantly increased the importance of having fast, cheap and transparent global transactions and is driving innovation in this area and e-commerce. This is confirmed by the fact that this year the G20 has raised the priority of the development of cross-border payments, explaining this decision by the fact that this segment of the economy is very important for economic growth, global development and inclusion, especially considering that today global payments are more expensive, slower, not too available and less transparent than local ones.

“The pandemic has become a significant challenge for business and every consumer, but at the same time has accelerated digitalization in all its forms. From the point of view of cashless technologies, the growth of contactless and online payments, tokenization and the development of payments by wearable means - all this has become a stable trend both in Europe and in Ukraine. For example, in Europe, tokenized payments in September grew by 30% compared to the pre-crisis period, and the share of payments in e-commerce during the year reached 41% of the total volume of purchase transactions using Mastercard cards. However, along with the growing popularity of digital commerce, security issues become even more important, and this is where technologies come to the rescue - biometric authentication, tokenization in e-commerce, and the like. These are the decisions

Revenues from global payments, $ trillion

Changes in consumer behavior

Just a few months of 2020 dramatically changed the persistent landscape of the global payments market over the previous decade, researchers at McKinsey say.Against the backdrop of a global decline in global payments market revenues due to a ban on departures and a decrease in employment and volumes of tourism (business tourism), cross-border e-commerce has become an exception and has shown significant global growth. In the first half of 2020, consumers spent $ 347 billion online shopping from American retailers, up 30% from the same period in 2019. Amazon sales figures for Q2 2020 showed 40% growth compared to the same period in 2019 and a triple increase in sales in the grocery category. UPS and PayPal reported double growth in cross-border transactions and value of goods sold. According to Finanso.se, the European digital payments market will record a record $ 802 billion in 2020 (an increase of 9,

In general, the global crisis and the rapid change in consumer behavior have led to a rethinking of operating models in business around the world, to the growth of e-commerce and a reduction in cash transactions.

COVID-19 leads to a decrease in the use of cash in the world.

The role of banks in the global payments market-2025

The most global payment conference SIBOS, which took place in October this year, paid a lot of attention to the topic of cross-border payments. Leading global market players who took part in presentations and discussion panels expressed key messages:- The development of open banking in the world is very important for the formation of the market for cross-border payments: “Open banking = Open data = Open finance,” notes Paul Stoddart, President, New Payment Platform Mastercard.

- For the cross-border payments market, it is important to develop global and local cooperatives. For example, we can talk about the acquisition of local clearing houses by large international players, which increases the efficiency of the entire system, provides access to BIGDATA and allows to increase the speed of payments.

- The role of the central bank in the development of the market for cross-border payments is enormous - from the development of a local settlement system to the introduction of innovative standards (including psd2, iso20022, GDPR, cybersecurity, etc.), noted Victoria Cleland, Chair | CPMI Task Force on cross-border payments.

- It is important to test innovations that improve the customer experience. An example is the recent experiment of HSBC, when 4 million customers received a token to access online banking instead of a card reader. “Experiments with digital currencies through public-private partnerships are helping to accelerate the search for new solutions in the crossborder,” said Diane S Reyes, Group General Manager and Global Head of Liquidity and Cash Management HSBC. As an example - the Jasper project (a joint experiment with digital currencies of the Bank of England, Bank of Canada, MAS and a number of commercial banks, including HSBC. You can read the report of the fourth phase of the experiment here).

- BIGDATA and speed of payments. An important standardization to improve big data analytics and secure access globally and across international payment ecosystems, says David Watson, Chief Strategy Officer of SWIFT.

CBDC and the global payments market

Today more than 80 central banks of the world study, develop and test digital currencies. However, there are still many unanswered questions - what is the real goal, is it possible to build cross-border infrastructure on this basis, what are the risks and benefits, centralized or decentralized path, what is the impact on the structure of liquidity and exchange rates.When will CBDCs go global.

“CBDC is like a train traveling at high speed and we don't know where exactly, but we understand that we must be part of this journey ...”, says Scott Hendry, Senior Director of Financial Technology at the Bank of Canada.

Recommendations and foreign experience of CBDC development, which were shared by the regulators of Canada, France and China during the SIBOS payment conference:

- The implementation of CBDC should not undermine the existing payment system.

- When introducing digital currencies, you need to take into account the necessary changes in the legislation. As an example, a change in the procedure for signing transactions and the transition to fully digital formats.

- Using CBDC can improve crossborder efficiency. At the same time, there are many issues that need to be resolved - for example, the issue with the exchange rate, which can significantly increase the cost of such transactions and CBDC will not solve this problem. The issue of efficiency for all participants in the new system is key.

- During the development of the CBDC project, it is very important for the Central Bank to ensure equal access to the financial system for all segments of the population, so that the project does not become inclusive and exclusive. It is necessary to think over the formats of identification and admission to the system of those who have smartphones and those who do not.

- Launching a CBDC requires an advanced digital population identification system - ideally, launching such a project with a national population identification system in place, as well as a regulated KYC procedure for remote onboarding of new clients. It is also important to ensure equal access for all participants in the banking market to work with CBDC.

- Centralized versus decentralized models are open discussion for now. Which format will be the best for the private sector and the central bank - the choice of a specific jurisdiction.

- Scaling CBDC in retail is a key issue during the launch of such a project. The People's Bank of China decided to build on the permanent infrastructure of the Alibaba Group and launch CBDCs with them in partnership. “Availability of ready infrastructure and partnership of the central bank with the private sector is a key issue of efficiency and speed of project scaling in the retail market ...”, - said Changchun Mu, Director of Digital Currency Institute of the People's Bank of China.