It seems too good to be true: You’re shopping online, eyeing a pair of shoes that are just a little more than you’d like to spend right now. A small icon next to the price (and that enticing add to cart button) gives you the best possible news you don’t have to pay all that money right now. You can pay for it in installments, breaking up the high price into payments that seem dare we say it positively affordable.

Offers to buy now and pay later are more and more common online with the rise of installment payment services (technically point-of-sale loan providers) such as Affirm, Afterpay, and Klarna, all rising buy now, pay later (BNPL) stars in the U.S. With some 23,000 retail partners in the U.S. between the three services, these payment options are almost ubiquitous sights for online shoppers. You may recognize the names, but understanding how Affirm, Afterpay, and Klarna (and services like them) work is a whole other matter.

First: That instinct that it’s too good to be true isn’t completely off-base. Of course there are certain terms you must abide by to use these services making your installment payments on-time, for example. They’re not consequence-free loans. But these services aren’t necessarily a dangerous scam, either, even if they are a little unfamiliar. (They are certainly less likely to land you in a cycle of debt than payday loans.)

In practice, installment payment services operate much like credit cards or store financing. When you make a purchase and choose to use the service, it essentially pays the full price of your purchase to the store or merchant. You then pay regular installments to the service, not the merchant, from a credit card, debit card, or bank account until you’ve repaid the full cost of your purchase. Your order will be shipped right away no waiting until your purchase is paid off to get your goods, as with the old-school layaway system.

The size and frequency of your payments will depend on the service you use, though many rely on a system in which the purchase price is broken into four payments made over about six weeks. With this system, your first payment is due at the time of purchase, and then you have a payment due every two weeks until all three remaining payments are made (six weeks). For the most part, if you make all your payments on time, you’ll pay no fees or interest.

You’re likely used to the monthly billing used by credit cards and utility companies: Why two-week increments? “It really coincides with how often people are paid, and how they’re budgeting out their expenses,” says Melissa Davis, chief revenue officer at Afterpay. Instead of budgeting monthly, based on your credit card or bank statement, rent due date, and other bills, many BNPL services allow people to budget based on when they’re paid.

If you’re not paying fees or interest, you may be thinking, how do these services make money? (Fair question.)

Mainly, services such as Affirm, Afterpay, and Klarna make money from the online stores you're shopping from. They charge retail partners a fee, and in return, those retailers tend to see higher sales and larger purchases from people using the services to make their online splurges more affordable. Unlike lenders or credit card companies, the bulk of these companies' earnings are coming from other companies, not from borrowers, though some do take in a small amount of money from late fees and interest payments (more on that later).

Listen to Real Simple's "Money Confidential" podcast to get expert advice on starting a business, how to stop being 'bad with money,' discussing secret debt with your partner, and more!

Anyone 18 or older with a credit card, debit card, or bank account can sign up for a BNPL service. You can make an account with the service of your choice for quicker shopping with participating retailers or simply select the option at checkout, but all services have encryption technology to keep your information safe and secure.

Generally speaking, Affirm, Afterpay, and Klarna are very similar, but they do each have their own distinct offerings, terms, and processes that may make one more appealing than the others. Read on to learn how Affirm, Afterpay, and Klarna work.

How Affirm works

Affirm differentiates itself from credit cards by rejecting late fees, hidden fees, and compound interest all common contributors to credit card debt. (Launched in 2012, it’s also the oldest U.S. BNPL service.) When you purchase something through Affirm, you pay no late fees (even if you have a late payment) but Affirm does charge interest.

Affirm approves users through a soft credit check, which won’t affect your credit score, though it can show up on your credit report, where it has no impact. Qualifying to use Affirm takes just a minute; once you’re approved, Affirm will show you exactly how much you owe, with no gimmicks. The price includes the cost of your purchase and any interest you’re charged; Affirm does offer 0 percent interest, but be aware that rates can go much higher, depending on several factors. You’re given the option to repay your loan over three, six, or 12 months the length of your loan could affect your interest rate, but Affirm allows you to consider all the options to find the repayment process that’s best for you.

Users can connect their Affirm account to a credit card, debit card, or bank account; payments will be deducted automatically from the payment method on the agreed-upon basis. The important shift is that Affirm will show users how much they owe, including interest, before they buy: You won’t have to pull out a calculator to figure out how much financing will end up costing you, and you’ll pay less than you would have on a credit card, thanks to Affirm’s commitment to simple interest instead of compound interest, which can build on itself. (No

deferred interest here, either.)

The appeal of Affirm over a credit card is that users know exactly how much they’ll end up paying from the start. If they miss a payment, they’ll be nudged to make up the payment as soon as possible, but no late fee will be charged. Unlike other services, Affirm will report on-time payments back to Experian, a credit bureau. On-time payments and responsible borrowing can actually improve your credit score. At the same time, making a very large purchase or using too much of your credit with Affirm (also called having a too-high credit utilization ratio) can hurt your credit score.

How Afterpay works

With some 15,000 retail partners in the U.S.,

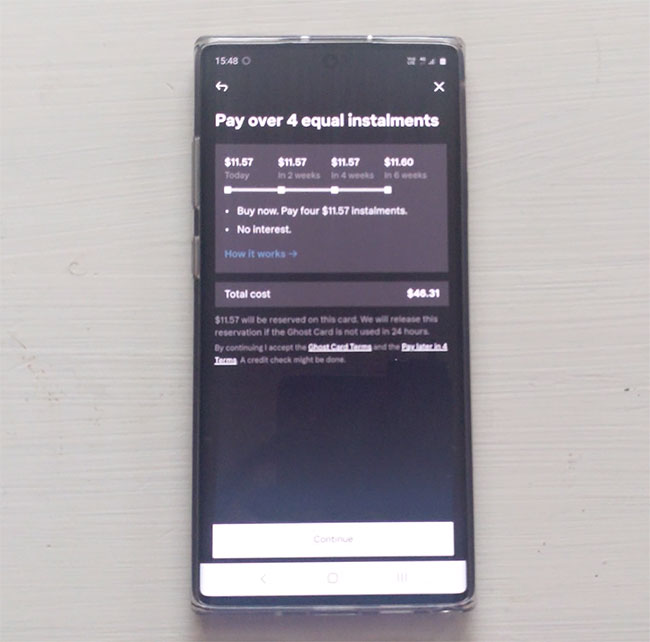

Afterpay has the furthest shopping reach of these BNPL services or point-of-sale loan providers. (Afterpay even just announced a new in-store shopping feature that allows shoppers to use the service for in-person purchases at participating retailers.) Afterpay offers interest-free installment payments spread over six weeks, with a payment due every two weeks (and one due at the time of sale). The cost of the item is divided evenly across those four payments, with no added interest.

When a payment is due, it will be automatically deducted from your payment method. You’ll receive a reminder ahead of time, so you can double-check that the payment will go through. After a brief grace period, Afterpay does charge late fees for delayed or missed payments: $8 for a late payment, with fees capped at 25 percent of the purchase price if multiple payments are missed. (Borrowers will be unable to use Afterpay again until they make any outstanding payments.) With capped fees, accumulating a huge mountain of debt through Afterpay would be difficult.

Afterpay does not run a credit check not even a soft one and approval is instantaneous. When you sign up for an account or apply to use Afterpay (essentially applying for a point-of-sale loan from Afterpay), you’ll enter your email address, phone number, billing address, payment method, and birthday, Davis says; you don’t have to share a social security number, and your credit score will not be affected. (Afterpay will text you a code to confirm your phone number.) If you miss payments, it will not hurt your credit score; on the other hand, if you’re a responsible borrower and always make your payments on time, your credit score will not increase, because Afterpay does not report to any credit bureaus.

How Klarna works

Klarna gives users the most flexibility in deciding how they want to pay for their online purchases. Klarna offers three options, though not all are available at all retailers. The first (and most popular, offered by all Klarna retail partners) is interest-free installments. This 'Pay in 4' system breaks a purchase into four equal payments that users make every two weeks. (The first is due at the time of purchase.) Late fees of up to $7 are charged if a second attempt to deduct the payment is unsuccessful. The second, Pay Later, allows users to receive their order immediately and pay later (within 30 days) in full, with no interest or fees. Pay Later is not offered by all retail partners, and if they go unpaid past the due date, customers can be blocked from using Klarna in the future, a Klarna spokesperson says.

The third option is offered only by select retail partners and is often used for large purchases. Similar to traditional store financing, it pays for a purchase in full and allows users to repay Klarna over anywhere from six to 36 months. Klarna’s monthly financing does charge interest—

Klarna’s annual percentage rate is 19.99 percent, though rates can vary for special offers or promotions—but users may be able to go interest-free by paying off the purchase in full within six months. A late fee of up to $35 can be charged if a monthly financing payment is missed.

Klarna may perform a soft credit check if you apply for the installment or pay later options; a soft credit check will not hurt your credit score, though it may appear as a (harmless) soft inquiry on your credit report. If you apply for Klarna financing, Klarna will run a hard credit check, which could hurt your credit score and will appear as a hard inquiry on your credit report. In both cases, you’ll know almost instantly if you’re approved.

Should you try Affirm, Afterpay, or Klarna?

It’s up to you to decide whether any of these BNPL services is right for you. Before you sign up, you should consider a few things.

Firstly, why do you need to break your purchase up into installments? If it’s because you cannot truly afford the item, you may want to rethink your online shopping habit and learn how to budget so you can be sure your purchases are within your range of affordability.

Second, take a look at any debt you may already have. If you already have a substantial amount of credit card debt and you’re looking for another way to keep spending, your time and energy will likely be better spent paying down that debt. If you are working to reduce your credit card debt or want to avoid that high-interest debt all together, a BNPL service might be the right alternative for you.

Davis says the vast majority of Afterpay users put debit cards down as their payment method. Having a credit card and using one of these services is close enough to the same thing that you may not want to do both. (And using a credit card to fund installment payments can just land you in more debt.) Affirm, Afterpay, and Klarna are presented as alternatives to credit cards; those wary of landing in deep credit card debt (or those trying to climb out of it) can still enjoy the convenience and budgeting of buying now and paying later, without the same fees and compound interest.

“We’re all about making sure people aren’t getting into debt,” Davis says.

Lastly, think about your overall financial picture. Credit cards come with risks, but they do have one huge benefit: building credit. Building credit early on (often with a credit card, though there are other methods) can help people get higher credit scores and lower interest rates on loans (think mortgages and car loans) later on in life. If you don’t have a credit card (and don’t want one), consider what that means for your credit: Do you have another method of building credit? If not, you may want to find one, or pick a service that allows you to build credit.

If you do want to wade into the world of buying now and paying later, do your research and try to pick one service that is available at many retailers you know and love. All services place individualized limits on purchase amounts based on a number of factors, including shopping and spending habits. New users may have a lower limit, but most services increase that limit for repeat users who make on-time payments. If you’re a big spender (and you can afford to pay it all off), sticking with one service will make it easier for you to make bigger purchases responsibly.

Affirm, Klarna, AfterPay and more: Online installment plans, explained

These alternative payment options let you buy goods now without paying full price for them right away.

If you've ever started adding things to your online shopping cart and then balked at the total, there are ways of easing the blow. You can try paying a little bit now, then paying your final bill off little by little.

Companies such as Affirm, AfterPay and Klarna tout the buy-now, pay-later system by giving you micro installment loans. You get your product right away without completely paying for it right away. Today, AfterPay has more than 8.4 million customers all over the world and two-thirds of them are millennials and Gen Z shoppers. Of Affirm's 4.5 million users, over half are in the same demographic.

But what are these installment plans and how are they different from traditional credit accounts? Here's the breakdown of these alternative financing options and how to use them.

What are installment services?

If you've ever bought a car, home or education, you've probably used an installment loan. Installment loans are lump-sum loans that you pay off over a set amount of months or years. For products like cars and homes, they're often funded by well-known banks, like Chase or Wells Fargo.

Mini installment plans from companies like AfterPay and Affirm act like microloans for everyday purchases, like clothes, makeup, electronics, and gym equipment (like Peloton). Affirm, for example, also supports unexpected purchases, like car repairs through YourMechanic. But unlike new car or home purchase loans, which you typically pay off over the course of many years, products and services financed through these services are typically paid off in a few weeks or months.

How do they work?

Each online installment plan offers different setups, but the general gist is: You buy your item now, select the plan at checkout with a qualifying retailer, create an account and complete your purchase. With Klarna and AfterPay, you get your goods right away and then pay for them over four installment payments: one when you check out and typically every other week or once a month thereafter. Affirm has payment options that usually range from three to 12 months, although some plans have terms as high as 48 months.

For AfterPay, as long as you make your four payments, you won't get charged late fees. Klarna has different payment options and some of them charge interest. Affirm charges 0-30% in interest depending on your payment plan.

To take advantage of these interest-free installment plans, the retailer you're shopping with needs to support them. Anthropologie, DSW and Fenty Beauty are AfterPay partners, for example. You might see the installment service's logo when you're viewing a product, letting you know the partnership exists and you can select a payment plan at checkout. From there, you'll usually pay the first installment and the next one will come out about two weeks later. Otherwise, the product or service will arrive on time, just like it would if you paid in full at checkout.

You can also shop through each company's app.

Affirm,

AfterPay and

Klarna all have apps in the App Store and Google Play, which let you shop, monitor your orders and make payments.

While they aren't like traditional loans, they're different from other types of alternative payment methods. For instance:

They aren't credit cards. Credit cards are a revolving credit line that you get approved for. You use your card to pay for your purchase in full and then at the end of the billing period, you'll pay off your bill or make payments until you pay it off in full. Typically, if you don't pay your balance off at the end of the billing period, interest will accrue, which can be 20% or more. CNET always recommends paying off your credit in full.

They aren't the same as layaway. Layaway is when you agree to pay off an item over the course of a few months and once you've paid it off, you can take it home. Layaway usually requires an upfront deposit and a service fee, and you don't get your goods until you've paid for them in full. Some installment plan companies require an upfront deposit, but you don't have to wait to get your item; you get it right away.

How does an installment service affect my credit score?

When you apply for a loan or a credit card, that hard credit check looks at your credit history to see if you're responsible enough with credit to lend to. With buy-now, pay-later apps, there's no hard credit inquiry. If the app checks your credit, it'll be a soft credit check, which won't hurt your credit score. The services don't specify the credit score you need to shop with them.

If you aren't diligent with payments, your credit score might be affected. For most micro installment loans, you're required to make payments about every two weeks and in four total installments. So if you don't pay your bill on time, that triggers a late payment for some companies. The three major credit bureaus will get notified and you could see your credit score take a dip. Late payments are one of the biggest factors in determining your credit score, and a drop of which could hurt your chances of borrowing money in the future.

Should I use these services?

It depends on what kind of shopper you are and your mentality about money. Weigh the pros and cons first:

Pros

- You can get it even if you can't afford it right away: If you have things you need or want to buy, you're not obligated to pay full price at checkout. Micro installment loans let you pay out your purchase over a few weeks.

- You don't need great credit to use it: Most services do a soft credit check, which won't hurt your credit score. If you don't have great credit or a long credit history, this is a good alternative payment option.

- It's simpler than a loan or credit card: If you've had trouble with credit cards or don't like using them, this is an easier method than applying for a credit card or personal loan. You can apply at checkout, whereas if you want a credit card or loan, you'll need to wait a few days before you can use those funds.

Cons

- You might believe you're spending less: If you balk at a $400 couch, seeing payments broken up into $100 every other week, for example, tricks you into believing you're paying less for an item. In reality, you're still paying the same amount and you're borrowing money to do it.

- You might not get approved for the full amount: Even if you don't have a strong credit history, it's still a factor in determining if you're eligible for the full amount requested. There's a chance you might not get approved for the full amount you're requesting.

- Not all purchases are eligible: Even if the retailer is a partner, not all purchases are qualifying. For instance, AfterPay has a $35 minimum installment payment, so if your order equals less than that, it's not eligible.

- It's still a loan: Remember you're still taking out a loan, even if you pay it off sooner than you would a traditional loan. Not paying on time could result in interest fees, late payment fees or not being able to use the service in the future.

While the convenience of delayed payment sounds appealing to get something now, you're still on the hook for paying your bill in full. If you need something now but can't afford it, micro installment loans might be a good idea. But if you don't think you'll be able to afford payments, you may want to consider another payment method or waiting until you have cash on hand to make your purchase.

Affirm has 4.5 million users, not the 3 million we previously quoted. It also has repayment options ranging from three to 12 months, not six to 18. Clarified that AfterPay does not charge late fees as long as you make four payments.

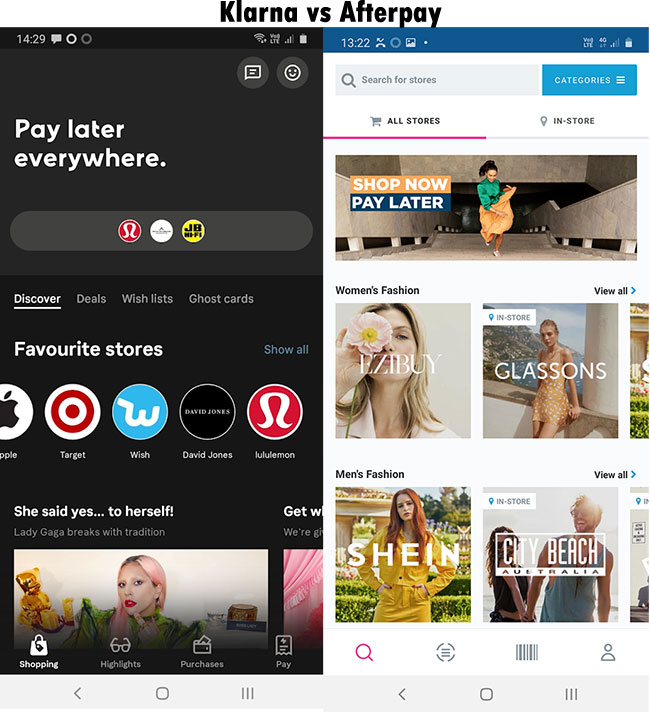

Quick Klarna vs. Afterpay comparison

| Feature | Klarna | Afterpay |

|---|

| Availability | US, UK, Australia, Finland, Spain, Italy, and 9 more | Australia, US, UK, Canada, New Zealand |

| Starting limit | $200 to $500 | $500 to $1,000 |

| Type | Online (Klarna app) | In-store / online |

| Repayments | 6 weeks | 8 weeks |

| Missed payment | Additional 7 days (varies by location) | $10 fee |

Video

Let’s bring this chapter with a quick comparison video.

Sign up process

The sign-up process is straight forward. To register on Klarna, you need a valid phone number and an email address for the initial registration.

After signing up, you can browse the app and add products to cart, but you will need to verify your payment information before purchasing your first item.

Afterpay requires:

- email address

- phone number

- Credit or debit card

The app charges a small amount to verify the payment method.

How do both work?

Interface – Klarna vs. Afterpay

Klarna

Klarna app is actually a browser with additional functionalities. The app comes with an interface where you can browse stores. You can add more stores by tapping on the add new button. When you open a store, the website opens up.

You will need the normal store account to purchase anything. For example, if you are purchasing something on Amazon, you will still need your Amazon account.

You can add the items to the cart which is within your account limits. On the app, you will have an option to pay with Klarna. The app will automatically detect the cart’s payment, but if for any reason it can’t, there is an option to add the payment manually.

Before the payment processes, you get to see the dues and dates. The app creates a ghost card which is only valid for this purchase. After you have purchased the item, the ghost card details are no longer valid. To see the app in action, check out the video: What is Klarna?

Afterpay

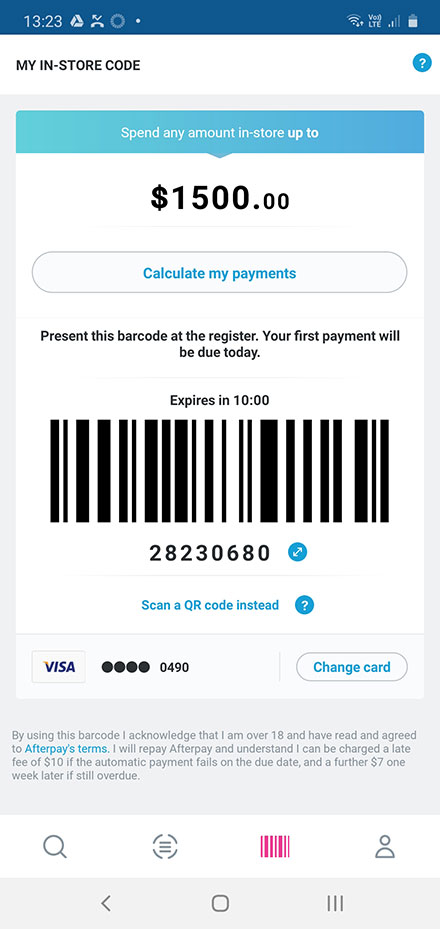

A part of over 11 million customers worldwide, Afterpay is different. After you have signed up, you get to see stores in the app. Tapping 0n one goes to their website. Unlike Klarna, Afterpay offers both online and in-store shopping.

To pay online, you log in with your Afterpay credentials while to pay in-store, the app generates a barcode. The barcode may not show if there is a problem with the payment method. It also expires every ten minutes, so you have to refresh to generate a new code.

Limits

Barcode and Limit – Afterpay

Klarna depending on your location gives you a good amount to spend while you can increase that by repaying on time. Also, depending on your region, there is a minimum spending limit. For example, here in Australia, the minimum cart amount is $35.

Afterpay also offers a maximum limit, but there isn’t any minimum limit. Here in Land Down Under, you get to spend $500 initially, and the limit automatically increases as you use the app.

Repayments

Repayments – Klarna App

Repayments with Klarna are also location dependent. The first payment is the day of the purchase. The next three payments are every fortnight. In total it gives you six weeks to pay back.

If you can’t pay on time, you get additional seven days, and if you can’t pay in the extra period, you are charged a fee. In some regions, you get more than seven days. You can read about the rules in your region on the

Klarna website.

Afterpay, on the other hand, used to charge the first payment on the day of the purchase (may still charge to new customers), but now the first payment is after two weeks. This gives the customer 8 weeks to pay back. Of course, if you miss a payment, you are charged a $10 fee.

Afterpay does not use any rating system, but not paying the required amount may lead to no limit increase. They also send an SMS reminder and an email four days and a day before.

How to pay with Klarna

Payment methods.

Payment via Klarna.

If you have chosen to pay through Klarna, after checking the transfer data, this interface will open automatically - you do not need to go anywhere.

After checking.

Choose your bank.

You will need to select your bank and enter it through Klarna.

You can choose exactly how to enter your bank: by the bank card number (you can enter it manually or scan the card if it is at hand), by your client number or by the QR code.

You can also register if you don't have a Klarna account yet.

Bank entrance.

Accounts.

After logging in, your accounts with this bank will be displayed on the screen. Select the account from which you want to pay for the transfer.

Enter one-time password from SMS or push.

Confirm payment.

Translation sent.

As you probably already know, Afterpay works by splitting the cost of your shop into four, equal payments, which are made every fortnight. But if you miss a payment, or don't have enough money in your account for a direct debit, you'll then be charged a $10 late payment fee.

How do you check out on Afterpay?

How it works

- Browse your favorite stores.

- Choose Afterpay as your payment method at checkout.

- Instantly create your account and complete your purchase.

Why did I get declined for Afterpay?

Here are a few reasons why a payment can be declined with Afterpay: Your first payment amount must be available at the time of purchase - even if you have nothing to pay today. Your Afterpay account has overdue payments owing. The Afterpay risk management department has declined your payment.

Do you need to be approved for Afterpay?

Since Afterpay isn't a loan company or credit union, you don't need to be approved for an account like you would to get a credit card or personal loan. The only criteria are that you must be 18 and have a credit or debit card you can link your account to.

How long does AfterPay take to pay merchants?

48 hours. Although AfterPay is a lay-buy service, merchants receive immediate payment minus the commission and flat fee of 30 cents. Unfortunately, though, this “immediate” payment is not so immediate. The company can take up to 48 hours to compensate the merchant for the transaction.

Does Afterpay ship after first payment?

For all of your future orders using Afterpay, your first installment will be deducted within 14 days. At the time of purchase, the full Afterpay schedule will be outlined for you. WILL MY ORDER BE SHIPPED STRAIGHT AWAY? Absolutely, your order will be shipped straight away.

What happens if you never pay Afterpay?

Afterpay allows you to pay for your purchase over 4 instalments due every 2 weeks. If a payment is not processed on or before the due date, late fees will apply – initial $10 late fee, and a further $7 if the payment remains unpaid 7 days after the due date.

What is my Afterpay limit?

Retailers on the Afterpay platform provide a limit per transaction, which at its maximum is $1,500. The maximum outstanding limit is $2,000, which is reserved only for customers who have previously demonstrated strong repayment capability behaviour over time with Afterpay.

Can you Afterpay over $1000?

Afterpay allows your total order amount to be split into 4 equal portions, and automatically charge fortnightly from your existing credit or debit card. Afterpay caters for order total (price + shipping) up to $1000.

What's better klarna vs Afterpay?

Afterpay: There are no interest charges on Afterpay purchases. Klarna: Financing plans with Klarna do charge an interest fee depending on the method of repayment you select. Month-to-month payments will set a standard interest rate, whereas a planned repayment will offer a more competitive APR.

How much do merchants pay for Afterpay?

The online shop is charged a flat fee of 30 cents and a commission that varies with the value and volume of transactions processed using Afterpay. The more you sell, at a higher value, the lower the percentage fee will be. The fee ranges from just over 6 percent per transaction down to 4 percent per transaction.

Can I use Klarna to pay bills?

If you use a Klarna financing account, you can't use a credit card to pay your bill — you must use your bank account or debit card.

How do I apply for klarna credit?

You can sign up for Klarna's Financing Account at the checkout of our partnering online stores. The Klarna Account is a credit option that provides you with a revolving account and is similar to a traditional credit card, but without the physical card.

Which payment methods are accepted by Klarna?

Klarna currently accepts all major debit and credit cards (i.e. Mastercard, Visa, AMEX, Discover). Please note that AMEX cards are not accepted when creating a One-time card.

Good to know: Prepaid cards are not accepted.

Is it hard to get approved for Afterpay?

Since Afterpay isn't a loan company or credit union, you don't need to be approved for an account like you would to get a credit card or personal loan. The only criteria are that you must be 18 and have a credit or debit card you can link your account to.

How is Afterpay different to a credit card?

The major difference here is that Afterpay lends to the business during the transaction, and the customer repays the money to Afterpay. Whereas consumers can shop around for credit cards that offer them rewards points, free flights, gift vouchers and so much more, Afterpay doesn't provide any of that.

Why is Afterpay declining my payment method?

Here are a few reasons why a payment can be declined with Afterpay: Your first payment amount must be available at the time of purchase - even if you have nothing to pay today. Your Afterpay account has overdue payments owing. The Afterpay risk management department has declined your payment.

Can I pay Afterpay with credit card?

Afterpay accepts debit or credit cards, including Mastercard, Visa, and American Express.

How do you register for Klarna?

In order to use Klarna no fees are charged. Just download the Klarna app and once you are logged in you can shop with Klarna or choose one of our payment options in your favored stores' checkout.

How do I register for Afterpay?

Yay! All you need to do now is visit

www.afterpay.com and set up your password. The next time you purchase with Afterpay, just log in securely when you checkout. Or you can download the Afterpay App to make the whole process even easier!

Does everyone get approved for Afterpay?

No. You'll be automatically approved as long as you're 18 and have a working credit or debit card.

Why can't I verify my Afterpay account?

Take care to key in the information correctly it must match what you have keyed in to your Afterpay Account Profile exactly. If you try and are not able to complete the verification, you can contact us and provide a copy of your ID.