Father

Professional

- Messages

- 2,602

- Reaction score

- 837

- Points

- 113

All new technologies are based on knowledge and analysis of where they came from and how they have changed over time. When we start creating an object recognition engine in Smart Engines, we seriously delve into the history of this object and its evolutionary path of development. This information directly affects the choice of speech recognition approaches. Today we will tell you where bank cards come from as a technology, and how they have developed over a hundred years.

In the modern world, instant payment using a bank card or even exclusively its electronic counterpart in a mobile phone will not surprise anyone. At the same time, the card itself — a piece of plastic or, for extra — premium options, a valuable metal — continues to develop as an independent product. Today, for most people on the planet, it may seem surprising that bank cards appeared long before the creation of the Internet, and the embossed inscription, which is now used, rather, to protect the card from forgery and give it a "status", was the first prototype of automatic customer data entry.

In the early 1920s, payment cards began to spread in the fuel trade. In 1924, the General Petroleum Corporation of California began issuing what they called "courtesy cards," and other chain gas stations quickly followed suit. Cardboard payment cards were issued to regular customers across the United States. With this card, the customer could pay for gasoline, as well as buy related products at any of the network stations that could be located at a significant distance from each other, which allowed them to keep the customer traveling around the country.

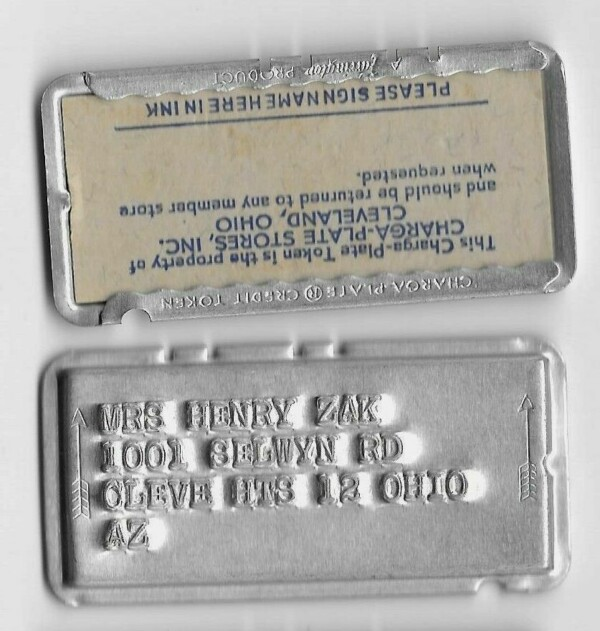

The first maps, like other documents, were made of cardboard. Since they were used much more often than, say, a passport, they quickly fell into disrepair and had to be changed, which caused inconvenience to both organizations that issued cards and customers. A large-scale modernization of the cards occurred in 1928, when the Boston company Farrington Manufacturing, specializing in the manufacture of metal engraved boxes and cases, released a prototype of the metal loyalty card-Charga Plate, which quickly became commonplace in retail chains.

The innovation, according to the advertisement, saved time on dictating the name to the seller, allowed identifying the customer in any store, and reduced the likelihood of errors when filling out the delivery address and invoicing. And Char Plates existed right up to the introduction of real credit cards into everyday use. Here is a card (never used!), which has become a rarity today, you can buy at auction:

www.ebay.com/itm/Vintage-1950s-Metal-Charga-Plate-Stores-Cleveland-Ohio-charge-plate-UNUSED-/143019942181

A hand-held embossing device, a method for applying lettering to metal plates, and a device for making an impression on the slip were patented, as was the proprietary Farrington OCR 7b font. In fact, with the developed and patented technology for manufacturing metal embossed tokens, the history of image recognition — Optical Character Recognition, OCR-began on which the principles of bank card recognition are based even today.

In terms of their shape and appearance, maps have not evolved significantly until recently. Created in the format of a standard business card-approximately 55*90 mm in size (today the standard specifies the exact size of 85.6 X 53.98 x 0.76 mm), they still exist today, conveniently fitting into a wallet. On the card, as before, the main banking details remain the client's name and the card number linked to the current account. The account number contains the type of payment system used, the bank's identification number, and the client's personal number.

The format of a credit card number is now defined by the international standard ISO 7812. In most cases, the credit card number consists of 16 digits. These numbers are used by the world's most popular payment systems, VISA and MasterCard. At the same time, there are card numbers consisting of 19 or 13 digits.

In this case, the first sign of the number applied to the payment card identifies the payment system in which this card operates. The card numbers of the founder of Diners Club credit cards, as well as the American Express system, or the regional Japanese payment system JCB start with the number 3, the number 4 indicates that the card belongs to the VISA system, and 5-belongs to MasterCard (with the same number in the first position, Diners Club cards are issued in the United States and Canada). With the number 6 in the first place, cards are issued by the Discover, Laser and InstaPayment payment systems. The Russian payment system MIR uses the number 2 in the first position.

The numbers in positions 7 through 15 form the Account Number-the account holder's number, which is unique for each client. The last digit of the number is a Checksum, calculated using a specific algorithm and necessary to verify the correctness of the entered data.

Most cards have the cardholder's name and surname printed on the front side. The name is usually written in Latin characters in the international transcription, sometimes duplicated in the national language. As a rule, the card's validity period is also indicated on the front side of the card.

The first four or 6 digits of the payment card number that are displayed on receipts and payment receipts are duplicated under the first four digits printed in the "OCR 7b" font. The front side of the card may also contain other information that makes it easier to identify the card. On the reverse side of the card is a verification code: in the VISA system, it is called CVV (card verification value), Master Card CVC (card validation code), in the MIR system — card verification parameter), consisting of three digits. They are an additional step in protecting the card from misuse, but now they are no longer relevant due to the development of multi-factor authentication methods.

It is important that with the development of the field of remote payments using a mobile phone, again, as a hundred years ago, there is a need to develop and improve technologies for automating the entry of card data into payment systems where interaction at the chip level is impossible. The card again becomes a carrier of visual information that is important for making a payment. Only now the task is to simplify entering data into the system not for the seller, but for the user.

The modern technology of automatic recognition of bank cards Smart CardReader, as well as the first mechanical machines that put a card impression on the slip, is aimed at automating the recognition and input of banking details from various bank cards. The system automatically finds and recognizes the card number, expiration date, and owner's name on cards of different formats and printing types.

Despite the complexity of electronic identification systems in bank cards, visually they do not allow us to significantly differentiate the client as a cardholder. In the fight for customers and emphasizing their premium status, banks issue non-standard cards using special color and design solutions, creating a textured and mirrored surface, using various methods of lamination and foiling.

New materials — transparent and textured plastic-have been used in the production of maps. And again — as a hundred years ago — there were metal cards, but no longer copper, but from precious and simply expensive alloys. In addition, some banks issue cards of non-standard size, as well as with atypical placement of basic banking details: in a vertical orientation or on the reverse side.

All these non-standard moves, of course, have a positive effect on attracting customers, but they cause trouble to the systems associated with processing such cards. We are constantly developing our Smart CardReader technology and have taught it quite successfully to cope with the difficulties of card recognition associated with artefacts that occur when using unusual materials and with non-standard location of banking details. Even if the map is held "upside down".

In the modern world, instant payment using a bank card or even exclusively its electronic counterpart in a mobile phone will not surprise anyone. At the same time, the card itself — a piece of plastic or, for extra — premium options, a valuable metal — continues to develop as an independent product. Today, for most people on the planet, it may seem surprising that bank cards appeared long before the creation of the Internet, and the embossed inscription, which is now used, rather, to protect the card from forgery and give it a "status", was the first prototype of automatic customer data entry.

About what a bank card and eyeglass case have in common

The first prototypes of payment cards appeared at the beginning of the XX century and were made of cardboard. They were not required to be too hard-wearing: they were not inserted into ATMs or other reading devices. They only needed to be presented when making a purchase in a store, cafe, or gas station. There was no need to talk about any integration of the card with the unified information banking system: the task of the first cards is to identify the owner and indicate their solvency in a particular network of stores, gas stations or food chains. Today, we would call these cards loyalty cards.In the early 1920s, payment cards began to spread in the fuel trade. In 1924, the General Petroleum Corporation of California began issuing what they called "courtesy cards," and other chain gas stations quickly followed suit. Cardboard payment cards were issued to regular customers across the United States. With this card, the customer could pay for gasoline, as well as buy related products at any of the network stations that could be located at a significant distance from each other, which allowed them to keep the customer traveling around the country.

The first maps, like other documents, were made of cardboard. Since they were used much more often than, say, a passport, they quickly fell into disrepair and had to be changed, which caused inconvenience to both organizations that issued cards and customers. A large-scale modernization of the cards occurred in 1928, when the Boston company Farrington Manufacturing, specializing in the manufacture of metal engraved boxes and cases, released a prototype of the metal loyalty card-Charga Plate, which quickly became commonplace in retail chains.

Embossing as a step towards artificial intelligence

On the issued cards, the owner's data was stamped (embossed). The buyer, when making a purchase, handed the card to the seller, who used a special press — an imprinter — to make an imprint of the buyer's card on the receipt. In other words, the card served as an impression confirming the purchase of goods by the cardholder. Embossing simplified and accelerated the interaction between the buyer and the seller, as it saved the seller from having to manually fill out the sales receipt and enter the buyer's data in it. If you imagine this operation in the modern world, then, in fact, with the help of such a card, a seal was placed on the receipt confirming the purchase of goods by a specific client.The innovation, according to the advertisement, saved time on dictating the name to the seller, allowed identifying the customer in any store, and reduced the likelihood of errors when filling out the delivery address and invoicing. And Char Plates existed right up to the introduction of real credit cards into everyday use. Here is a card (never used!), which has become a rarity today, you can buy at auction:

www.ebay.com/itm/Vintage-1950s-Metal-Charga-Plate-Stores-Cleveland-Ohio-charge-plate-UNUSED-/143019942181

A hand-held embossing device, a method for applying lettering to metal plates, and a device for making an impression on the slip were patented, as was the proprietary Farrington OCR 7b font. In fact, with the developed and patented technology for manufacturing metal embossed tokens, the history of image recognition — Optical Character Recognition, OCR-began on which the principles of bank card recognition are based even today.

Cards with the owner's name and individual number stamped out are still preserved today and are used in places where trade is conducted in the absence of the Internet: as before, the card is "rolled" in a specialized device that leaves an impression of the data on a paper "slip". The cardholder leaves with the purchase, and the seller goes to the phone and authorizes the payment by phone. Such procedures are encountered by travelers in countries where the development of trade outstrips the development of information technology.

The chip is not a luxury

Bank cards, which appeared in the middle of the 20th century, were already a more complex payment tool, the task of which was not only to identify the client, but also to provide the seller with information about the state of his bank account, as well as to ensure as fast interaction with the bank and conduct a transaction. Magnetic strips containing the necessary data appeared on the cards, and later the cards were equipped with an electronic chip that provides faster interaction with the cash register.In terms of their shape and appearance, maps have not evolved significantly until recently. Created in the format of a standard business card-approximately 55*90 mm in size (today the standard specifies the exact size of 85.6 X 53.98 x 0.76 mm), they still exist today, conveniently fitting into a wallet. On the card, as before, the main banking details remain the client's name and the card number linked to the current account. The account number contains the type of payment system used, the bank's identification number, and the client's personal number.

The format of a credit card number is now defined by the international standard ISO 7812. In most cases, the credit card number consists of 16 digits. These numbers are used by the world's most popular payment systems, VISA and MasterCard. At the same time, there are card numbers consisting of 19 or 13 digits.

What's in my inscription to you?

The first 6 digits of the number are the unique number of the bank that issued the cards-the Issuer Identification Number (IIN) or Bank Identification Number (BIN).In this case, the first sign of the number applied to the payment card identifies the payment system in which this card operates. The card numbers of the founder of Diners Club credit cards, as well as the American Express system, or the regional Japanese payment system JCB start with the number 3, the number 4 indicates that the card belongs to the VISA system, and 5-belongs to MasterCard (with the same number in the first position, Diners Club cards are issued in the United States and Canada). With the number 6 in the first place, cards are issued by the Discover, Laser and InstaPayment payment systems. The Russian payment system MIR uses the number 2 in the first position.

The numbers in positions 7 through 15 form the Account Number-the account holder's number, which is unique for each client. The last digit of the number is a Checksum, calculated using a specific algorithm and necessary to verify the correctness of the entered data.

Most cards have the cardholder's name and surname printed on the front side. The name is usually written in Latin characters in the international transcription, sometimes duplicated in the national language. As a rule, the card's validity period is also indicated on the front side of the card.

The first four or 6 digits of the payment card number that are displayed on receipts and payment receipts are duplicated under the first four digits printed in the "OCR 7b" font. The front side of the card may also contain other information that makes it easier to identify the card. On the reverse side of the card is a verification code: in the VISA system, it is called CVV (card verification value), Master Card CVC (card validation code), in the MIR system — card verification parameter), consisting of three digits. They are an additional step in protecting the card from misuse, but now they are no longer relevant due to the development of multi-factor authentication methods.

When electronics don't help out

Automation of the interaction processes between bank cards and payment terminals allowed banks to move away from the principle of embossing when issuing mass-use cards, simplifying the process of personifying a plastic blank, while expanding the possibilities of its electronic filling. Today, the magnetic stripe on the card is duplicated by a contact and contactless chip, which allows interaction with terminals without having to insert them into a reader. The user's bank details are plotted on the map using laser printing, indent and flat printed methods that are less expensive than embossing.It is important that with the development of the field of remote payments using a mobile phone, again, as a hundred years ago, there is a need to develop and improve technologies for automating the entry of card data into payment systems where interaction at the chip level is impossible. The card again becomes a carrier of visual information that is important for making a payment. Only now the task is to simplify entering data into the system not for the seller, but for the user.

The modern technology of automatic recognition of bank cards Smart CardReader, as well as the first mechanical machines that put a card impression on the slip, is aimed at automating the recognition and input of banking details from various bank cards. The system automatically finds and recognizes the card number, expiration date, and owner's name on cards of different formats and printing types.

Non-standard map: marketing or something else?

A bank card has long been an everyday item used by billions of people around the world. The bank card market is developing independently, and therefore banks are trying to attract customers with cards that are significantly different from those of competitors.Despite the complexity of electronic identification systems in bank cards, visually they do not allow us to significantly differentiate the client as a cardholder. In the fight for customers and emphasizing their premium status, banks issue non-standard cards using special color and design solutions, creating a textured and mirrored surface, using various methods of lamination and foiling.

New materials — transparent and textured plastic-have been used in the production of maps. And again — as a hundred years ago — there were metal cards, but no longer copper, but from precious and simply expensive alloys. In addition, some banks issue cards of non-standard size, as well as with atypical placement of basic banking details: in a vertical orientation or on the reverse side.

All these non-standard moves, of course, have a positive effect on attracting customers, but they cause trouble to the systems associated with processing such cards. We are constantly developing our Smart CardReader technology and have taught it quite successfully to cope with the difficulties of card recognition associated with artefacts that occur when using unusual materials and with non-standard location of banking details. Even if the map is held "upside down".