Content:

DIFFERENTIATED LOAN PAYMENT

Differentiated payment is one of the options for repayment of loans/credits, where the amount of payment decreases closer to the end of the loan term.

The word comes from the Latin differentia (difference, difference).

The discrepancy (difference) in the amounts of payments on differentiated payments arises primarily due to the fact that after the next payment is made, the body of the debt decreases, and therefore the amount that is calculated as interest for the use of the loan.

And the more the debt body decreases, the less the total payment becomes.

Differences from annuity

The easiest to understand and the most popular in the banking environment is the annuity method of repaying loans (in equal installments). Differentiated calculation is used as the only alternative to the well-established approach.

Benefits of differentiated payments

Disadvantages

Formula for calculation

Each payment consists of two main parts:

Then the monthly payment ("EP") will be calculated as follows:

EP = OD + Pr

The payment of the principal debt (“OD”) is calculated as follows:

OD = SK/No,

Where:

The charge on accrued interest ("Pr") is calculated based on the balance of the debt for the current period and the interest rate.

Pr = OZ * St/12

Where "St" is the rate in percent per annum, expressed in decimal form, and "OZ" is the remaining amount of debt.

OZ = SK - (OD * N)

The general formula is then as follows.

EP = SK/No + (SK - (SK/No) * N) * St/12

Calculation example

Let the loan amount be 260,000 $, the interest rate is 13.9% per annum, the loan term is 5 years (60 months).

The principal payment will be calculated as follows:

260,000/60 = 4333.33 $/month.

Then the final payment for the first month will be equal to

EP = 4333.33 + (260000-4333.33 * 0) * 0.139/12 = 7345 $

In the second month

EP = 4333.33 + (260000-4333.33 * 1) * 0.139/12 = 7294.81 $

In third

EP = 4333.33 + (260000-4333.33 * 2) * 0.139/12 = 7244.61 $

Etc.

In the last

EP = 4333.33 + (260000-4333.33 * 59) * 0.139/12 = 4383.53 $

The total loan amount will be 351,855, 83 $. (overpayment 91,855.83 $). For comparison, with an annuity calculation, the total loan amount will be 362,177.4 $. (overpayment - 102,177.4 $), the monthly payment will be fixed - 6036.3 $.

An example of a payment schedule for a loan with differentiated payments

The data in the table below corresponds to the loan mentioned above (260 thousand rubles at 13.9% for 5 years).

ANNUITY LOAN PAYMENT

An annuity payment is a loan/loan payment option that involves the payment of the principal amount and interest on it in equal installments throughout the entire loan period at regular intervals.

The word "annuity" is borrowed from the French language. Annuite - "annuity".

An annuity can mean either a loan agreement (in some cases, an insurance agreement), or the payment itself under such an agreement.

An alternative to annuity is differentiated payment.

Types of annuities

When making calculations, banks can use the following annuities:

The procedure for calculating the annuity payment

First of all, borrowers must understand that the amount and procedure for payment of the loan is established by the bank in the agreement (the payment schedule can be drawn up in a separate application). And therefore, the bank has the right to independently determine the formula by which the next payment will be calculated.

Banking formula

For example, some bank uses the following calculation formula (clause 3.1.1 of the General Conditions for Consumer Lending):

Bank annuity payment formula.

Here:

Pl = (260,000 * 13.9/(12 * 100))/(1- (1 + 13.9/(12 * 100)) -5 * 12 = 3011.6667/(1-1.0115833 -60 ) = 3011.6667/(1-0.501073) = 6036.29 $

The total amount is 6036.29 * 12 months * 5 years = 362177.4 $ (overpayment - 102,177.4 $).

A variant of the repayment schedule for such a loan.

Formula according ("On consumer loans)

Defines a formula of the following type.

Formula of annuity payment on consumer loan.

The smallest positive solution to the equation is the base period interest rate.

Here:

General formula with coefficient for annuity

Monthly payment = annuity rate * loan amount.

The greatest difficulty is the calculation of the coefficient (K):

Calculating the annuity rate.

Here:

Interest rate per month (i)

Calculating the interest rate for an annuity.

i = 0.00487 (expressed in decimal),

K = 0.00487 * (1 + 0.00487) 36 /((1 + 0.00487) 36 - 1) = 0.030351304

Payment = 0.030351304 * 12000 = 364.22 $.

The total amount is 364.22 * 36 = 13111.92 (overpayment of 1111.92 $).

DEBIT CARD

A debit card (payment card) is a bank card associated with a customer's personal or current account, intended primarily for making non-cash payments in merchants.

Payments can be made using:

As with any other personal account, debit cardholders in most cases have access to:

In addition, banks can offer additional services:

Stimulating buying activity

To increase the volume of transactions on a card account, many banks resort to using special incentive programs:

Types of cards

Payment systems offer banks the following types of cards:

The bank itself may offer special packages of services that will be provided to the holder additionally within the framework of the service (in addition to those offered by the payment system).

In addition, debit cards can be:

CREDIT CARD

A credit card ("CC") is a bank card with funds available in the account within the pre-approved credit limit. Accordingly, the receipt of a credit card is always associated with the signing of a loan agreement or acceptance of the terms of the offer.

Overdraft

Overdraft cards can be distinguished as a separate subspecies of bank cards, since they combine the properties of both debit cards (when settlements in merchants and cash withdrawals are made at the expense of the client's own funds) and credit (after exhausting their own funds, the client can use the credit limit).

Credit limit

The amount of available funds within the limit established by the agreement is, in fact, a consumer loan without guarantors and collateral.

The contract must include:

The limit can be revised by the bank at regular intervals. The client himself can initiate such a procedure by submitting an application to the bank. In this case, the bank may take into account additional documents confirming the client's solvency or the level of his permanent income.

The moment of issuing such a loan can be considered the issuance of cash in self-service devices or payment for goods/services from the funds of the limit.

In the first case (cash withdrawal), banks often charge additional fees (for example, a fixed minimum payment) and also do not provide a grace period.

In the second, when paying from the account, the commission may be less or completely absent, and a deferral is provided for the funds used (the period and the countdown procedure are described in the agreement).

Credit card details

The appearance of credit cards is no different from other bank cards. Of the main details, the following are applied to the credit card:

The card can be equipped with:

PAYMENT SYSTEM QIWI

QIWI is a Russian multi-platform payment system launched in 2007. Initially, the business was based on a large network of payment terminals through which it was possible to replenish a mobile phone account, pay fines and make other payments.

However, in 2004 the brand joined forces with the international system Visa, and "QIWI Wallet" acted as a co-branded product (Visa QIWI Wallet), providing users with all the capabilities of bank cards.

Currently, the QIWI brand belongs to the United System of Instant Payments CJSC. The latter also owns: Qiwi Bank (it was he who bought the Tochka service for entrepreneurs from Otkritie FC, and also acquired Rapida, another payment system), Qiwi Advertising, the payment service of the same name, two lottery organizers (Lotto Master "and" Lotto Integrator ") and the supplier of fiscal registrars Paykiosk.

There are about 150 thousand terminals in the self-service points network. The turnover of the system in 2017 is more than 910 billion rubles, the net profit of the service in the same year is 4 billion rubles.

The geography of presence has increased to 17 countries (in 9 of them, services are provided by companies operating under a franchise).

Key features of the QIWI service

Payment for goods and services from an e-wallet account (including banking services, housing and communal services, services of companies providing communications and Internet access, as well as fines).

BANK CARD

A bank card is a unique identifier of the user/account and the bank in which it is served, most often printed on a plastic card of a given format. The card does not have to be physical, it can be virtual, then the issue (issue) of the card will actually represent the issuance by the bank of a unique number to the user and other details necessary for making payments. Several current accounts can be linked to the same customer number at once. Thanks to the card number, banks can correlate the current account with the operation being carried out (debit or credit).

The format of the card is defined by the ISO/IEC 7810 standard. The dimensions specified in it are indicated in the image below.

Bank card sizes.

The most common format is ID-1 (85.60 ? 53.98 mm, with a thickness of 0.76 mm).

Attributes

The most important attribute applied to the card is the number. But he's not the only one. Additionally, the following information can be applied:

Number

The number can be represented as a sequence of 13, 16 or 19 digits. The most common are sixteen-digit numbers. The rest have already practically gone out of circulation.

The rules for generating numbers are described in the international standard ISO/IEC 7812.

The sequence is written in four blocks of 4 digits. The information that is recorded in the number can be designated as follows:

Decoding the number on the bank card.

Views

Bank cards can be:

Depending on the territory of action

By type of settlement

By appointment

Loyalty programs

To attract a new audience, payment systems often hold their own promotions (in cooperation directly with their partners).

However, banks themselves often stimulate the demand for card products by:

BITCOIN MINING

To avoid chaos in the Bitcoin network, only one member of the network shares the information collected about transactions at a given time, and the rest update their records based on his data packet. This stage is called mining. Such a member of the network is chosen at random.

When a block is created, its author receives a reward for the successful execution of mathematical operations, this is the first transaction of the block. Then, other translations that have not yet been entered into any block are written into the block. The block creator can control the composition of the block and select transactions.

The unit of measurement for mining performance is hash per second (hash/s), which also means one of the parameters of the power of a graphics card. GPU resources are used to compute the hash, which leads to the formation of a new block. However, the more people who want to create blocks, the less chances miners with home computers have - you can already find companies selling equipment or data center capacities specifically for mining. This leads to the fact that the probability of outperforming a more powerful processor in performing the same operation is reduced to almost zero.

In addition to the task to calculate the hash with the correct amount, when creating a block, there is a "complexity" parameter that adjusts the numerical value of the result. The lower the target value, the more difficult it is to complete the task. Approximately every 2 weeks, the system complicates the requirements for new block headers to maintain an average speed of 1 block per 10 minutes. Additionally, it is worth noting that the hash result is completely unpredictable, which makes it impossible to cheat to achieve the desired result.

It is possible to form blocks at the same time, which leads to branching, since several blocks consider the same fragment of the chain as a parent due to the parallel formation of blocks by all miners.

Moreover, it is theoretically possible to gain control over the entire system: if you control more than 50% of the power of the bitcoin network, then the chain of transactions created by the fraudster with incorrect data will be accepted by the “correct” part of the network as the main one, since the system considers the longer blockchain correct. Operations that are not included in the main branch are queued for inclusion in a new block, but the reward for them is not repeated, which explains how bitcoins can disappear.

To prevent the value of Bitcoin from decreasing, the system is programmed to automatically reduce the amount of reward for creating a block by half every several years. And there is also a limit on the maximum number of bitcoins in the system: 21 million. This figure is the sum of the members of a decreasing geometric progression. Initially, for each new block, you could get 50 units of cryptocurrency. Then twice more the bonus was cut in half - again a decreasing geometric progression. It is easy enough to predict that by 2031 bitcoins will no longer be profitable when creating new blocks, since the reward will not exceed 1 bitcoin.

To simplify the mining task, pools have been created that consolidate small miners and are visible to the system as one miner with huge computing power. Upon successful block generation, the reward is distributed among the pool members. Lack of pool membership - too little bonus per block.

It is becoming clear that the time has come to stimulate such an ardent interest in cryptocurrencies with new ways of income. Several years ago, “other” cryptocurrencies appeared, based on the same technology, but with different scripts and some features. We will talk about them in a separate article.

CHARGEBACK (RETURN)

Chargeback is a back money, the term is used exclusively in relation to transactions with card accounts (bank cards). This procedure is designed to protect the cardholder from direct (without the owner's permission or consent) debiting of funds from the account. A harder version of the refund.

It is the responsibility of the recipient to prove the correctness of the payment. The procedure is initiated by the owner of the bank card through the issuing bank.

Refunds are possible when using such international payment systems as VISA and MasterCard. The Russian payment system Mir is no exception (here the term “dispute” appears instead of the term “chargeback”).

The bank cannot refuse to initialize the refund procedure, since when connected to the payment system, it accepts the rules of the latter, in which this procedure is explicitly spelled out.

The most common causes of chargeback

The processing time for applications for refunds can be about 120 days (VISA) or 180 days (MasterCard). The Mir system stipulates a “reasonable time frame”. However, for most standard operations, the chargeback procedure is performed within 30 days.

BITCOIN

You will learn:

Perhaps it would be nice to invent an analogue of cash for the Internet. Pay in a couple of clicks without confirming your identity and commission, store money on your computer with the possibility of instant sale or exchange. And also so that this currency is independent of the banking system of any state.

This is how Bitcoin can be described in a nutshell. The emergence of such a means of payment is a logical step in the development of mathematical algorithms on which many modern technologies are based, especially around large amounts of data.

What is Bitcoin?

First of all, any cryptocurrency is an uncontrolled payment instrument for carrying out p2p transactions (between users), available only online, which, among other things, has no restrictions on emission, countries of work or requirements for currency holders.

Bitcoin payments are made directly between the owners of special wallets, in the sense of similar to Internet wallets for electronic money (QIWI, WebMoney, Yandex.Money). However, the payment process takes place without the involvement of intermediate participants such as settlement banks or payment system aggregators in the scenario of accepting payments in favor of the online store.

The anonymity of virtual money is ensured by a digital signature. Anyone can understand from what name of which wallet (address) the message is written. This is similar to the nickname in your favorite game, only without the possibility of fake. Checking the integrity of the message is provided by the hashing method - the assignment of a numerical code to the data, calculated mathematically. In addition, each member of the network maintains its own records of all members of the network and their operations. Records of completed transactions are transmitted in batches (blocks) between all participants in the system.

The cryptocurrency is decentralized, i.e. no one controls the issue and movement of funds. Any money we all are used to can be artificially devalued by the Central Banks: it is enough to print an excess number of monetary units, for example, to cover the public debt. This means that anyone can print, or rather create from nowhere (extract) bitcoins by connecting to a special network.

Since transfers are generally carried out without intermediaries, the commission can be equated to zero, which adds to the advantages of cryptocurrency in comparison with traditional means of payment. Of course, for exchanging virtual currency for dollars or euros, each platform charges its own percentage. However, in relation to the total turnover, these figures are not much more than zero.

Thanks to the transfer to the recipient's account through the processing of the transaction by the network and the elimination of dependence on banks, the transfer reaches the recipient's address instantly.

The differences between virtual currency do not end there. While a credit card payment can always be revoked in the event of an error, this is not possible for Bitcoin, which allows the possibility of fraud without any protection or insurance, as would be the case when using 3DS in card transactions.

How to earn bitcoins?

Basic cryptocurrencies do not imply the accrual of interest on the account balance, which makes it difficult to make a profit. However, some exchanges or wallet management platforms offer bonus "pennies": a bitcoin unit can be divided, for example, as a pound into cents - 1 satoshi (satoshi) is 0.00000001 BTC. The bonus can be obtained for clicks on banners, transitions to advertising sites, creating a new wallet or other fairly simple actions on special sites - bitcoin "faucets", English. Bitcoin faucet,).

You can usually get about 0.0001 bitcoins for free and with little or no effort, but if you are lucky, you will encounter a bonus that is closer to a whole unit of cryptocurrency. Unfortunately, withdrawing the trophy right away is not always allowed by the rules of sites that distribute "crypto kopecks": you will first have to accumulate at least 0.001 BTC. In addition, you cannot endlessly receive, albeit a small, but free reward - you can often find a time limit until the next opportunity to receive a task. And yet, the freedom of action is not limited in everything: for a referral brought into the system, you can usually get a bonus too. And to simplify the process of mining cryptocurrency in this way, aggregators have appeared that allow you to log in to several sites of this topic at the same time and switch between them much faster.

Like other currencies, bitcoins are traded on special exchanges, which makes it possible to earn money, if, of course, you are familiar with this area of activity. When there was enough virtual money for people to buy it, bitcoin exchanges opened, which also means the formation of the starting market price. Now the rise in prices for bitcoin is fantastically rapid and looks like blowing up another economic bubble, but experts disagree on the likelihood that it will burst in the near future. Some people compare the rampant interest in cryptocurrencies with pyramid schemes.

In addition to sites with free bonus satoshi, it is possible to receive bitcoins from other holders as a donation or incoming payment. To do this, it is enough to provide a "wallet number" - your address in the bitcoin network.

Finally, the most difficult way to become the owner of this means of payment is mining. It is enough to run a special script on your computer and you can already make money out of nowhere! The logic of this script is open and transparent, you do not need to look for it in the secret dungeons of the Internet. The maximum possible number of bitcoins in existence is of course 21 million coins. New bitcoins are created on the principle of "credit me X out of nowhere" for the computer performing complex mathematical operations to optimize the hash of the block header in the block chain of transactions. Currently, about 15 million units of cryptocurrency have been issued. At the beginning of the life of bitcoin, you could get 50 BTC for each operation performed, but every few years this figure is automatically reduced to avoid an oversupply of virtual money, so the more people who want to join the network, the lower the reward.

How do I use bitcoins?

To start using the cryptocurrency, it is enough to register the "address" (wallet) to which the charges will be received, then install the official program for working with Bitcoin. To start accepting payments, there is no need to conclude agreements with the bank, providing a pile of documents and the maiden name of a great-grandmother. The file with your address will be stored on your computer, and if necessary, you can open it on another device as a USB flash drive. By the way, there is a known case when a man was looking for a winchester with bitcoins equivalent to $ 7.5 million in a landfill, which he threw away without thinking.

The future of bitcoin

Bitcoin has already gone beyond the cryptocurrency. Services have emerged to solve fundamental problems in copyright, insurance, and even account management. This is just the beginning!

Unfortunately, the penetration of the latest technologies into the life of the average person is usually slowed down by the unavailability of the legal framework.

In the case of blockchain, global banks have already created the R3 consortium for a deeper study of cryptocurrencies (Goldman Sachs, JP Morgan, Credit Suisse, Barclays) and now the organization has more than 20 largest banks. The consortium is also engaged in the creation of blockchain-based solutions outside the financial industry.

R3 plans to prepare a plan for introducing cryptocurrencies into the banking industry as a tool for completing daily tasks, and not just as a currency. In the Russian Federation, blockchain is supported primarily by Qiwi and Sberbank. Some time ago, the Bitruble trademark was registered, but then followed by a number of loud statements from representatives of the state financial system about the impossibility of free use of cryptocurrencies in the foreseeable future.

German Gref, in the course of one of the Finnopolis innovation technology forums, urged not to exaggerate the dangers of cryptocurrencies, which the government has announced over the past years.

“This is definitely not something that needs to be banned”, Gref assured.

In the Russian Federation, accepting payments in bitcoins is legally prohibited, however, some global trading platforms are already offering to connect a module for accepting cryptocurrencies to the site.

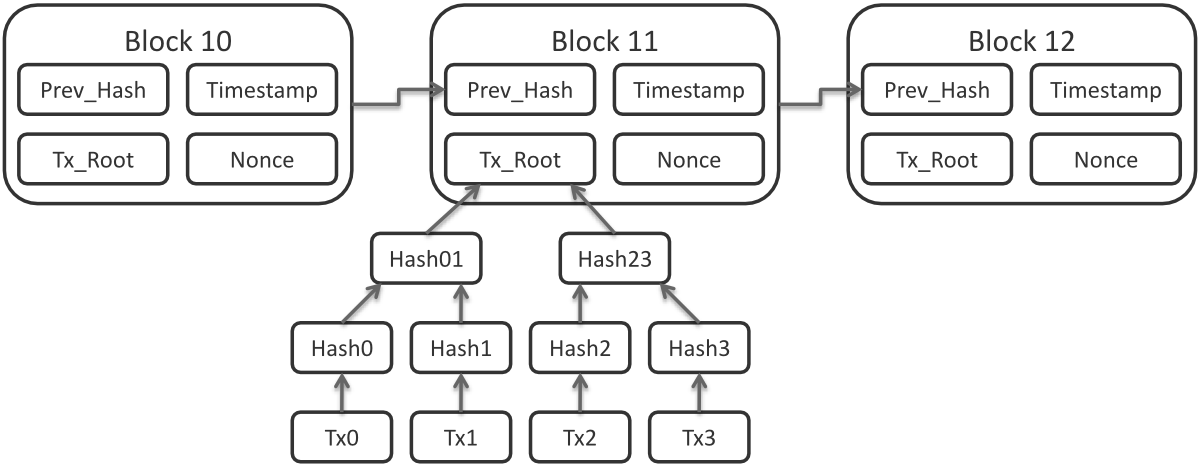

BLOCKCHAIN

Bitcoin differs from other means of payment in that each "coin" stores the entire history of transactions that have been performed in the entire history of the existence of a particular unit of cryptocurrency. In addition, each member of the bitcoin network has data on all transactions performed, which excludes the possibility of introducing non-existent transactions. Individual operations are combined into blocks to reduce the amount of data and simplify information exchange on the network. The block data is not encrypted in any way, which allows anyone to double-check transfers or find out the balance of a specific address.

Blockchain technology.

A Bitcoin address is an alphanumeric code derived from a mathematical transformation of the public key, for example 175tWpb9Н1S7NmH4Zx6rewF9WQrcZv245W. This character sequence can be stored as a barcode or QR code for easy access. However, if the address and access data to it are lost, it is impossible to gain access to the wallet. “Recovering the password” will not work either - only one unique pair of public (public) + private (private) key is possible for one address. However, you can create as many addresses as you like, which has several advantages.

In simple words, the bitcoin network is a community of address holders ("wallets"), who, when making transfers, inform all other owners of bitcoin addresses about the operation and each writes the fact of the transaction in his own version of the network's payment history, like in a notebook.

A block or piece of transaction history is called a sequential blockchain. Each such block of data of the bitcoin network refers to the previous one, which provides protection against overwriting or data substitution. In other words, a block is a leaf from the network's ledger, which means that it is theoretically possible to recover the network data mathematically with a deliberate attempt to introduce an error.

Any block has a serial number and a link to the address of the previous block, or rather its hash. So, in theory, you can build all existing blocks in a chain and restore the history of the entire network! There are specialized sites (eng. Blockchain explorer) where you can view this data.

It is easy to guess that the entire bitcoin payment history takes up an incredible amount of data. The first versions of wallet programs were focused on downloading and working with a full base of operations. Thus, the program can work completely autonomously, without having to go online. In June 2015, the database size was over 42 GB! Consequently, it takes almost more than a day to download and process the database during the first launch.

Cryptocurrencies continue to gain popularity and now it is quite difficult to store and process the entire amount of data on your laptop. The next step in the development of such applications was "thin clients" that store offline only links to blocks and their headers, downloading details for the desired block if necessary. This type of application is suitable for most users as it supports any payment events, but makes it impossible to mine bitcoins on a home computer. Mining or mining cryptocurrency - a topic for a separate material, but note that in the last couple of years, mining has become a separate business: data centers have appeared that provide power for mining; it became possible to purchase mining equipment from special firms; there are known cases of finding empty territories of former factories, densely packed with computers engaged in round-the-clock mining of cryptocurrency.

For the owner of a bitcoin address, this all means that anyone is able to study the history of his bitcoin address and calculate the current amount on the account (this is how the network client application works, showing the balance). To add maximum anonymity, you can use each bitcoin address for a single transaction along the way, raising the chances of generating a block to create a piece of new bitcoin. Another way is to shuffle transactions, which advanced wallets are already able to do. It is worth noting that the public history of an address does not imply the publicity of the address-owner pair. That is, until you yourself disclose the information that you own a certain wallet, it will remain your secret.

Since all participants have data on all network operations, disabling even half of the addresses will not be able to destroy the network, which means absolute distribution, which is one of the self-defense mechanisms of the technology. But let us note that there is a theoretical probability of gaining control over 51% of the network, which will open up the possibility of fraudulent operations fraudulently.

Applications of blockchain technology

Blockchain technology is like a diamond safe, in which anyone can put anything, anyone else will see what is supposed to be there, but only its owner can remove or change an item. Based on the principles of the blockchain network, a number of technologies have been created that help solve some of the fundamental problems of the modern world.

First of all, let's look at the problem of running out of bitcoins. As you know, every 4 years the reward for creating a new block in the transaction chain is halved and approximately by 2040 the limit of 21 million created cryptocurrency units will be reached, which already now motivates engineers around the world to create Bitcoin analogues. Some of them are quite popular, especially due to the still high rewards and the possibility of mining at home. Here is an approximate ratio of the rates of various cryptocurrencies:

User authorization and authentication

EmcSSH - a customized storage for public keys (passwords) and lists of users entitled to authorized access.

This blockchain application helps to solve the problem of the human factor in protecting data from unauthorized access. Instead of a login-password link, the user will have a specific key file located in the blockchain. If a file is stolen, it is still possible to generate a new key or block access.

EmcSSL. This platform is an extension of the custom SSL protocol. In this case, the blockchain is a place where digital prints of certificates of individual users or organizations are stored.

On the basis of such a branch of blockchain development, you can create an absolutely secure authorization system in banking services or other sites.

Emc InfoCard - Virtual Business Card

The technology allows you to create a single questionnaire, for example, for registration on sites. Moreover, it becomes possible to update your details on all business cards ever issued!

Jurisprudence

EmcTTS It is now possible to store a digital fingerprint of a version of a document inside bitcoin.

TTS can become indispensable in the design of all types of transactions - thanks to this technology, it is easy to track the time of creation of a version of a document and its content, which negates any attempts to substitute contracts or other fraudulent transactions.

Emc DPO. TTS-like document filing technology.

Features in limiting the rights to edit files, as well as in the public history of their changes. It can be used for electronic document management and storage of a heap of papers: from a cadastral passport to TIN.

Emc Atom. Certification of transactions.

A tool for concluding transactions without the participation of a notary and other related bodies.

Cybersecurity

Emc DNS. An alternative DNS method for distributing addresses on the network, protected from spoofing and other types of attacks.

Payments and transfers

Fast virtual transactions - Micropayments with maximum speed without registration.

On May 16, 2013 the WebMoney payment system announced the introduction of the title units "WMX" - 1 WMX is equivalent to 0.001 BTC. For a WebMoney user, it is enough to create an additional wallet of the corresponding type. Working with WMX is similar to interaction with other WebMoney virtual wallets. Received WMX can be used instantly since there is no need to wait for the transaction to be included in the block. In addition, it is possible to return erroneous or fraudulent transactions. Additionally, there is an exchange of WMX for other currencies within WebMoney. This became possible because the transfer of WMX to Webmoney does not create transactions in the "Bitcoin" system, since according to the "Property Rights Storage Agreement", WMX is the right to receive bitcoins, and not the bitcoins themselves.

TOKENIZATION

Tokenization is a technology that helps secure mobile payments. Most contactless payments, including mobile payments (ApplePay, SamsungPay) involve the transfer of card data, in particular its number. At the time of payment, the electronic device may be compromised (for example, the transmitted information will be read by a fraudster located in the immediate vicinity of the card or smartphone).

Tokenization technology allows replacing the real number of the customer's card with a unique generated code - a token (or "token"), which will be used only for a specific purchase. The attacker will no longer be able to use the information received, since the real card number is not explicitly transmitted, and the token has already been used. A new token will be issued for the next purchase.

Thus, even after reading the smartphone signal at the time of purchase and receiving the data transmitted by it via the wireless communication protocol, the attacker only has a generated code (token) in his hands, which will no longer be accepted for payment. At the same time, the issuing bank can easily track an attempt to reuse the token.

In fact, the issuance of the token is initiated by the application that stores the data of the original card (services such as ApplePay or SamsungPay). A similar scheme is implemented by the online service of secure Internet payments MasterPass from MasterCard (the data of the card itself is not transferred to the online store).

At the moment, tokenization is supported by the VISA and MasterCard payment systems , the Russian system "Mir" plans to introduce the technology as early as 2017.

LONG ENTRY

Long record (Airline addendum data) is a payment gateway request in favor of the acquiring bank when paying for air tickets with an extended set of data describing the purchase object (tickets).

Long entry is a mandatory requirement of the international payment systems VISA and MasterCard when ordering and paying for tickets for air travel.

The request must contain the following information for each flight segment (one flight with takeoff and landing):

MPOS TERMINAL

An mPOS terminal (mobile POS terminal) is a miniature device that allows you to accept bank cards for payment using a smartphone/tablet, in other words, to carry out mobile acquiring.

mPOS is an abbreviation for English. mobile Point Of Sale, translated as "mobile point of sale".

The card reader (reader) can be connected to a smartphone or tablet via an audio jack (3.5 mm mini-jack, most often used to connect headphones), microUSB (the main port for connecting chargers and data cables) or a wireless communication protocol (for example, Bluetooth).

Each type of connection has its own advantages and disadvantages. But all mPOS terminals differ from stationary versions in the following aspects.

Benefits

Disadvantages

POS TERMINAL

A POS terminal is a terminal equipment (hardware and software complex) for the physical receipt of payments from various bank cards or merchant acquiring. The terminal can work with cards equipped with a magnetic stripe, chips (microprocessors) or NFC tags (contactless technology).

POS is an abbreviation for English which translates as "point of sale".

Sometimes a POS terminal in trade means a cashier's workplace (all equipment with working programs for receiving payments). Such terminals are included in POS-systems, which make it possible to facilitate the work of sales personnel due to the wide range of capabilities of the complex.

The main difference between bank POS terminals and POS systems is that the terminal is a separate device that prints and stores fiscal information that is subject to mandatory certification, and POS systems do not need certification, since the work with fiscal accounting is either transferred to the cash register or to POS terminals.

Virtual POS terminals work without client-side hardware to read data from the card. The information is entered by the bank card holder independently through the web interface, and is processed on the side of the bank and (or) payment service.

The problem of POS terminals is their short range. An mPOS terminal is used to receive payments at the exit , which is used in conjunction with a smartphone or tablet.

SOFTWARE DEVELOPMENT KIT (SDK)

SDK (from the English "Software Development Kit" - "set of programs for development") is a set of necessary software products (libraries, scripts, etc.), designed to facilitate the process of developing and testing code for specific software platforms (software packages , hardware platforms, etc.).

The manufacturer of the software (hardware or software and hardware) platform is interested in the influx of new programmers who expand the scope of the main product and therefore offers the SDK most often free of charge. To expand the functionality of the SDK and simplify development, integrated development environments (IDEs) can be used that interact with the SDK.

Often platform vendors rename their proposed SDKs:

RESPONSIBLE STORAGE

Secure storage is a legal term used in relation to a situation in which material values (for example, a delivery object) were not accepted by the recipient and, for objective reasons, must be stored at the expense of the recipient's funds, the latter, in turn, must immediately notify the sender of the refusal to accept and ensure the safety of the received goods/cargo.

The term should in no way be confused with the usual storage of inventory items under a storage agreement.

Refusal to accept goods or cargo may be caused by various reasons, the grounds for refusal may be the requirements of applicable laws, other legal acts or the terms of the concluded agreement between the sender and the recipient.

A controversial situation of safekeeping can be resolved in several ways.

PAYMENT SYSTEM MASTERCARD

MasterCard is a global payment system that works with bank cards of the same name.

MasterCard Inc. Is a transnational corporation that unites tens of thousands of banks and other financial organizations in 210 countries around the world to work with MasterCard cards. The central office is located in the USA (New York).

The company has existed since 1966. It was created to counterbalance the increasingly popular VISA payment system. The first name was “Interbank Card Association”, the name was changed to “MasterCard” only in 1979.

Corporation MasterCard Inc. owns not only the MasterCard payment system, its main assets also include:

MasterCard offers its customers the following additional services and services:

Types of cards

MAESTRO

Maestro is the name of a debit bank card that works in the global MasterCard payment system. The Maestro card is accepted for payment through terminals (at cash desks), for withdrawing cash from ATMs (self-service terminals). Maestro cards can be prepaid.

Maestro cards were launched in 1992.

Maestro is also a global service (processing) that works with the cards of the same name (it began its work in 1990).

The key feature of Maestro cards is that information from a chip or magnetic stripe must be read and transferred to the issuing bank for approval. Manual entry of card details (number, expiration date, etc.) will be rejected by the bank. Payment from these cards without the owner's signature (for cards with a magnetic stripe) or without entering a PIN code (for cards with a microchip) is not possible.

When paying over the Internet (online payment), Maestro cards require a security code in accordance with 3-D Secure technology. These can be one-time passwords in SMS to the linked phone number, codes received at the ATM, or a special PIN code for online purchases. There is no CVC2 or CVV2 code on Maestro cards.

Direct analogue of Maestro cards - VISA Electron.

GLOBAL DISTRIBUTION SYSTEM (GDS)

GDS (from the English "Global Distribution System") is an international reservation system. Apply to:

The largest GDSs include:

FULFILLMENT

Order fulfillment is a complex of operations to accompany the client's goods from the moment of its registration (order, purchase) to issue. The word used in the field of Internet commerce has no analogue and therefore is used without translation. The English word "fulfillment" is most often translated as "completion" of something.

The fulfillment service involves such a set of operations to support the purchase as:

Benefits of order fulfillment for e-commerce

- Differentiated loan payment

- Annuity loan payment

- Debit card

- Credit card

- Payment system QIWI

- Bank card

- Bitcoin mining

- Chargeback (return)

- Bitcoin

- Blockchain

- Tokenization

- Long entry

- mPOS terminal

- POS terminal

- Software Development Kit (SDK)

- Responsible storage

- Payment system MasterCard

- Maestro

- Global Distribution System (GDS)

- Fulfillment

DIFFERENTIATED LOAN PAYMENT

Differentiated payment is one of the options for repayment of loans/credits, where the amount of payment decreases closer to the end of the loan term.

The word comes from the Latin differentia (difference, difference).

The discrepancy (difference) in the amounts of payments on differentiated payments arises primarily due to the fact that after the next payment is made, the body of the debt decreases, and therefore the amount that is calculated as interest for the use of the loan.

And the more the debt body decreases, the less the total payment becomes.

Differences from annuity

The easiest to understand and the most popular in the banking environment is the annuity method of repaying loans (in equal installments). Differentiated calculation is used as the only alternative to the well-established approach.

Benefits of differentiated payments

- The total amount of the overpayment on the loan is lower than in the case of an annuity.

- The loan can be repaid much earlier than the due date.

- The more you make a payment, the less subsequent payments will be.

- The financial burden on the payer significantly decreases over time.

Disadvantages

- Complicated calculation formula.

- Lack of a clear payment schedule (if the borrower makes payments more than the original schedule, the subsequent minimum payment is recalculated, albeit downward, but in any case, this value becomes unstable and requires a new current payment schedule).

- At the beginning of payments, the burden on the payer is noticeably greater than at the end. Few may find this approach useful when planning a budget.

Formula for calculation

Each payment consists of two main parts:

- repayment of the body of the debt (denoted in the formula "OD");

- payment of interest on a loan (designation "Pr").

Then the monthly payment ("EP") will be calculated as follows:

EP = OD + Pr

The payment of the principal debt (“OD”) is calculated as follows:

OD = SK/No,

Where:

- SK - the loan amount,

- No - the total number of payments.

The charge on accrued interest ("Pr") is calculated based on the balance of the debt for the current period and the interest rate.

Pr = OZ * St/12

Where "St" is the rate in percent per annum, expressed in decimal form, and "OZ" is the remaining amount of debt.

OZ = SK - (OD * N)

- SK is the loan amount.

- OD is a monthly payment to pay off the principal debt.

- N is the number of payments already made.

The general formula is then as follows.

EP = SK/No + (SK - (SK/No) * N) * St/12

Calculation example

Let the loan amount be 260,000 $, the interest rate is 13.9% per annum, the loan term is 5 years (60 months).

The principal payment will be calculated as follows:

260,000/60 = 4333.33 $/month.

Then the final payment for the first month will be equal to

EP = 4333.33 + (260000-4333.33 * 0) * 0.139/12 = 7345 $

In the second month

EP = 4333.33 + (260000-4333.33 * 1) * 0.139/12 = 7294.81 $

In third

EP = 4333.33 + (260000-4333.33 * 2) * 0.139/12 = 7244.61 $

Etc.

In the last

EP = 4333.33 + (260000-4333.33 * 59) * 0.139/12 = 4383.53 $

The total loan amount will be 351,855, 83 $. (overpayment 91,855.83 $). For comparison, with an annuity calculation, the total loan amount will be 362,177.4 $. (overpayment - 102,177.4 $), the monthly payment will be fixed - 6036.3 $.

An example of a payment schedule for a loan with differentiated payments

The data in the table below corresponds to the loan mentioned above (260 thousand rubles at 13.9% for 5 years).

| Month | Loan balance | Basic payment | Percentage | Final payment |

|---|---|---|---|---|

| 1 | 260000.00 | 4333.33 | 3011.67 | 7345.00 |

| 2 | 255666.67 | 4333.33 | 2961.47 | 7294.81 |

| 3 | 251333.33 | 4333.33 | 2911.28 | 7244.61 |

| 4 | 247000.00 | 4333.33 | 2861.08 | 7194.42 |

| 5 | 242666.67 | 4333.33 | 2810.89 | 7144.22 |

| 6 | 238333.33 | 4333.33 | 2760.69 | 7094.03 |

| 7 | 234000.00 | 4333.33 | 2710.50 | 7043.83 |

| 8 | 229666.67 | 4333.33 | 2660.31 | 6993.64 |

| 9 | 225333.33 | 4333.33 | 2610.11 | 6943.44 |

| 10 | 221000.00 | 4333.33 | 2559.92 | 6893.25 |

| 11 | 216666.67 | 4333.33 | 2509.72 | 6843.06 |

| 12 | 212333.33 | 4333.33 | 2459.53 | 6792.86 |

| 13 | 208000.00 | 4333.33 | 2409.33 | 6742.67 |

| 14 | 203666.67 | 4333.33 | 2359.14 | 6692.47 |

| 15 | 199333.33 | 4333.33 | 2308.94 | 6642.28 |

| 16 | 195000.00 | 4333.33 | 2258.75 | 6592.08 |

| 17 | 190666.67 | 4333.33 | 2208.56 | 6541.89 |

| 18 | 186333.33 | 4333.33 | 2158.36 | 6491.69 |

| 19 | 182000.00 | 4333.33 | 2108.17 | 6441.50 |

| 20 | 177666.67 | 4333.33 | 2057.97 | 6391.31 |

| 21 | 173333.33 | 4333.33 | 2007.78 | 6341.11 |

| 22 | 169000.00 | 4333.33 | 1957.58 | 6290.92 |

| 23 | 164666.67 | 4333.33 | 1907.39 | 6240.72 |

| 24 | 160333.33 | 4333.33 | 1857.19 | 6190.53 |

| 25 | 156000.00 | 4333.33 | 1807.00 | 6140.33 |

| 26 | 151666.67 | 4333.33 | 1756.81 | 6090.14 |

| 27 | 147333.33 | 4333.33 | 1706.61 | 6039.94 |

| 28 | 143000.00 | 4333.33 | 1656.42 | 5989.75 |

| 29 | 138666.67 | 4333.33 | 1606.22 | 5939.56 |

| 30 | 134333.33 | 4333.33 | 1556.03 | 5889.36 |

| 31 | 130000.00 | 4333.33 | 1505.83 | 5839.17 |

| 32 | 125666.67 | 4333.33 | 1455.64 | 5788.97 |

| 33 | 121333.33 | 4333.33 | 1405.44 | 5738.78 |

| 34 | 117000.00 | 4333.33 | 1355.25 | 5688.58 |

| 35 | 112666.67 | 4333.33 | 1305.06 | 5638.39 |

| 36 | 108333.33 | 4333.33 | 1254.86 | 5588.19 |

| 37 | 104000.00 | 4333.33 | 1204.67 | 5538.00 |

| 38 | 99666.67 | 4333.33 | 1154.47 | 5487.81 |

| 39 | 95333.33 | 4333.33 | 1104.28 | 5437.61 |

| 40 | 91000.00 | 4333.33 | 1054.08 | 5387.42 |

| 41 | 86666.67 | 4333.33 | 1003.89 | 5337.22 |

| 42 | 82333.33 | 4333.33 | 953.69 | 5287.03 |

| 43 | 78000.00 | 4333.33 | 903.50 | 5236.83 |

| 44 | 73666.67 | 4333.33 | 853.31 | 5186.64 |

| 45 | 69333.33 | 4333.33 | 803.11 | 5136.44 |

| 46 | 65000.00 | 4333.33 | 752.92 | 5086.25 |

| 47 | 60666.67 | 4333.33 | 702.72 | 5036.06 |

| 48 | 56333.33 | 4333.33 | 652.53 | 4985.86 |

| 49 | 52000.00 | 4333.33 | 602.33 | 4935.67 |

| 50 | 47666.67 | 4333.33 | 552.14 | 4885.47 |

| 51 | 43333.33 | 4333.33 | 501.94 | 4835.28 |

| 52 | 39000.00 | 4333.33 | 451.75 | 4785.08 |

| 53 | 34666.67 | 4333.33 | 401.56 | 4734.89 |

| 54 | 30333.33 | 4333.33 | 351.36 | 4684.69 |

| 55 | 26000.00 | 4333.33 | 301.17 | 4634.50 |

| 56 | 21666.67 | 4333.33 | 250.97 | 4584.31 |

| 57 | 17333.33 | 4333.33 | 200.78 | 4534.11 |

| 58 | 13000.00 | 4333.33 | 150.58 | 4483.92 |

| 59 | 8666.67 | 4333.33 | 100.39 | 4433.72 |

| 60 | 4333.33 | 4333.33 | 50.19 | 4383.53 |

ANNUITY LOAN PAYMENT

An annuity payment is a loan/loan payment option that involves the payment of the principal amount and interest on it in equal installments throughout the entire loan period at regular intervals.

The word "annuity" is borrowed from the French language. Annuite - "annuity".

An annuity can mean either a loan agreement (in some cases, an insurance agreement), or the payment itself under such an agreement.

An alternative to annuity is differentiated payment.

Types of annuities

When making calculations, banks can use the following annuities:

- post-numerando (first, the principal is paid, and then the amount of interest);

- prenumerado (interest first, then principal).

The procedure for calculating the annuity payment

First of all, borrowers must understand that the amount and procedure for payment of the loan is established by the bank in the agreement (the payment schedule can be drawn up in a separate application). And therefore, the bank has the right to independently determine the formula by which the next payment will be calculated.

Banking formula

For example, some bank uses the following calculation formula (clause 3.1.1 of the General Conditions for Consumer Lending):

Bank annuity payment formula.

Here:

- Pl -annuitetny payment (per month);

- P annual - interest rate in percent per annum;

- S - loan amount;

- T - loan term in months.

Pl = (260,000 * 13.9/(12 * 100))/(1- (1 + 13.9/(12 * 100)) -5 * 12 = 3011.6667/(1-1.0115833 -60 ) = 3011.6667/(1-0.501073) = 6036.29 $

The total amount is 6036.29 * 12 months * 5 years = 362177.4 $ (overpayment - 102,177.4 $).

A variant of the repayment schedule for such a loan.

| MONTH OF PAYMENT | MAIN DEBT | INTEREST | AMOUNT TO PAY | REMAINING BASIC DEBT |

|---|---|---|---|---|

| September 2018 | 2,966.85 | 3,069.42 | 6,036.27 | 257,033.15 |

| October 2018 | 3,099.75 | 2,936.52 | 6,036.27 | 253,933.40 |

| November 2018 | 3,038.46 | 2,997.81 | 6,036.27 | 250 894.94 |

| December 2018 | 3,169.88 | 2 866.39 | 6,036.27 | 247,725.06 |

| January 2019 | 3 111.76 | 2,924.51 | 6,036.27 | 244,613.30 |

| February 2019 | 3 148.49 | 2 887.78 | 6,036.27 | 241,464.81 |

| March 2019 | 3,461.53 | 2,574.74 | 6,036.27 | 238,003.28 |

| April 2019 | 3,226.53 | 2 809.74 | 6,036.27 | 234,776.75 |

| May 2019 | 3 354.03 | 2 682.24 | 6,036.27 | 231,422.72 |

| June 2019 | 3 304.21 | 2732.06 | 6,036.27 | 228 118.51 |

| July 2019 | 3430.09 | 2 606.18 | 6,036.27 | 224,688.42 |

| August 2019 | 3 383.72 | 2652.55 | 6,036.27 | 221 304.70 |

| September 2019 | 3423.66 | 2612.61 | 6,036.27 | 217,881.04 |

| October 2019 | 3,547.05 | 2489.22 | 6,036.27 | 214,333.99 |

| November 2019 | 3,505.95 | 2,530.32 | 6,036.27 | 210,828.04 |

| December 2019 | 3 627.63 | 2 408.64 | 6,036.27 | 207,200.41 |

| January 2020 | 3,590.82 | 2,445.45 | 6,036.27 | 203,609.59 |

| February 2020 | 3,639.13 | 2,397.14 | 6,036.27 | 199,970.46 |

| March 2020 | 3 833.86 | 2 202.41 | 6,036.27 | 196 136.60 |

| April 2020 | 3,727.11 | 2,309.16 | 6,036.27 | 192,409.49 |

| May 2020 | 3844.06 | 2 192.21 | 6,036.27 | 188,565.43 |

| June 2020 | 3816.25 | 2 220.02 | 6,036.27 | 184,749.18 |

| July 2020 | 3,931.34 | 2 104.93 | 6,036.27 | 180,817.84 |

| August 2020 | 3,907.46 | 2 128.81 | 6,036.27 | 176,910.38 |

| September 2020 | 3,953.46 | 2,082.81 | 6,036.27 | 172,956.92 |

| October 2020 | 4,065.70 | 1 970.57 | 6,036.27 | 168,891.22 |

| November 2020 | 4,047.88 | 1,988.39 | 6,036.27 | 164,843.34 |

| December 2020 | 4,158.14 | 1,878.13 | 6,036.27 | 160685.20 |

| January 2021 | 4143.99 | 1,892.28 | 6,036.27 | 156,541.21 |

| February 2021 | 4,188.23 | 1,848.04 | 6,036.27 | 152,352.98 |

| March 2021 | 4,411.73 | 1,624.54 | 6,036.27 | 147,941.25 |

| April 2021 | 4289.75 | 1,746.52 | 6,036.27 | 143,651.50 |

| May 2021 | 4 395.10 | 1,641.17 | 6,036.27 | 139 256.40 |

| June 2021 | 4 392.28 | 1,643.99 | 6,036.27 | 134,864.12 |

| July 2021 | 4 495.49 | 1,540.78 | 6,036.27 | 130,368.63 |

| August 2021 | 4 497.21 | 1,539.06 | 6,036.27 | 125,871.42 |

| September 2021 | 4,550.30 | 1,485.97 | 6,036.27 | 121 321.12 |

| October 2021 | 4650.22 | 1,386.05 | 6,036.27 | 116,670.90 |

| November 2021 | 4658.91 | 1,377.36 | 6,036.27 | 112,011.99 |

| December 2021 | 4,756.57 | 1,279.70 | 6,036.27 | 107,255.42 |

| January 2022 | 4,770.07 | 1,266.20 | 6,036.27 | 102,485.35 |

| February 2022 | 4826.38 | 1 209.89 | 6,036.27 | 97658.97 |

| March 2022 | 4,994.93 | 1,041.34 | 6,036.27 | 92,664.04 |

| April 2022 | 4,942.33 | 1,093.94 | 6,036.27 | 87,721.71 |

| May 2022 | 5,034.08 | 1 002.19 | 6,036.27 | 82,687.63 |

| June 2022 | 5,060.10 | 976.17 | 6,036.27 | 77,627.53 |

| July 2022 | 5149.40 | 886.87 | 6,036.27 | 72,478.13 |

| August 2022 | 5 180.63 | 855.64 | 6,036.27 | 67,297.50 |

| September 2022 | 5,241.79 | 794.48 | 6,036.27 | 62,055.71 |

| October 2022 | 5327.30 | 708.97 | 6,036.27 | 56,728.41 |

| November 2022 | 5,366.56 | 669.71 | 6,036.27 | 51,361.85 |

| December 2022 | 5,449.48 | 586.79 | 6,036.27 | 45,912.37 |

| January 2023 | 5,494.25 | 542.02 | 6,036.27 | 40,418.12 |

| February 2023 | 5 559.11 | 477.16 | 6,036.27 | 34,859.01 |

| March 2023 | 5,664.57 | 371.70 | 6,036.27 | 29,194.44 |

| April 2023 | 5 691.62 | 344.65 | 6,036.27 | 23,502.82 |

| May 2023 | 5,767.76 | 268.51 | 6,036.27 | 17,735.06 |

| June 2023 | 5826.90 | 209.37 | 6,036.27 | 11,908.16 |

| July 2023 | 5,900.22 | 136.05 | 6,036.27 | 6,007.94 |

| August 2023 | 6,007.94 | 70.93 | 6,078.87 | 0.00 |

Formula according ("On consumer loans)

Defines a formula of the following type.

Formula of annuity payment on consumer loan.

The smallest positive solution to the equation is the base period interest rate.

Here:

- DP k - the amount of the k-th payment;

- q k - the number of payments from the date of issue;

- e k - the number of shares of the main period from q of the k -th payment to the k-th;

- i - rate expressed in decimal;

- m is the number of payments.

General formula with coefficient for annuity

Monthly payment = annuity rate * loan amount.

The greatest difficulty is the calculation of the coefficient (K):

Calculating the annuity rate.

Here:

- i - the interest rate on the loan per month;

- n is the number of payments (months).

Interest rate per month (i)

Calculating the interest rate for an annuity.

i = 0.00487 (expressed in decimal),

K = 0.00487 * (1 + 0.00487) 36 /((1 + 0.00487) 36 - 1) = 0.030351304

Payment = 0.030351304 * 12000 = 364.22 $.

The total amount is 364.22 * 36 = 13111.92 (overpayment of 1111.92 $).

DEBIT CARD

A debit card (payment card) is a bank card associated with a customer's personal or current account, intended primarily for making non-cash payments in merchants.

Payments can be made using:

- merchant acquiring (with POS terminals),

- mobile aciring (with mPOS terminals),

- internet acquiring.

As with any other personal account, debit cardholders in most cases have access to:

- Internet banking and/or mobile application for account management;

- receiving translations from other users and organizations, creating your own;

- making various payments (utilities, taxes, fines, etc. from your personal account).

In addition, banks can offer additional services:

- special conditions for deposits;

- buying currencies;

- issue of additional cards to the main personal account (including other payment systems or with a personal design);

- timely notification of transactions and available balance (SMS, Push, E-mail).

Stimulating buying activity

To increase the volume of transactions on a card account, many banks resort to using special incentive programs:

- accrual of bonuses (with the possibility of converting into funds on the account, into discounts when paying, etc.);

- discounts in the network of partners;

- accrual of interest on the balance (subject to special conditions);

- cashback (cash-back - refund from purchases);

- reduction in the cost of service (for example, when special conditions for the balance and/or turnover are met).

Types of cards

Payment systems offer banks the following types of cards:

- classic/standard (with a basic set of services and services);

- Gold/"Gold" (cards with additional discounts and loyalty programs from the payment system and directly from the issuing bank, as well as with increased limits on payments and loans. For example, Visa Gold provides emergency cash withdrawal abroad, support in other emergency situations for travelers, including those with health insurance and legal assistance);

- Platinum/"Platinum" (in addition to the benefits of "gold" cards, purchase insurance and extended warranty service are added);

- Other premium cards (Visa Signature, Visa Infinite, Visa Black, World Mastercard Black Edition, World Elite Mastercard, etc., which offer various additional services and terms of service, emphasize the status of the owner).

The bank itself may offer special packages of services that will be provided to the holder additionally within the framework of the service (in addition to those offered by the payment system).

In addition, debit cards can be:

- social (for such categories of holders as students, students and retirees);

- salary (served within the framework of salary projects);

- virtual (for payments on the Internet or for connecting to Apple Pay, Google Pay, Samsung Pay, such cards do not have a physical carrier);

- co-badging (combining two payment systems at once, designed primarily for travelers);

- instant/unnamed (issued to the client immediately, without waiting for release, as opposed to nominal).

CREDIT CARD

A credit card ("CC") is a bank card with funds available in the account within the pre-approved credit limit. Accordingly, the receipt of a credit card is always associated with the signing of a loan agreement or acceptance of the terms of the offer.

Overdraft

Overdraft cards can be distinguished as a separate subspecies of bank cards, since they combine the properties of both debit cards (when settlements in merchants and cash withdrawals are made at the expense of the client's own funds) and credit (after exhausting their own funds, the client can use the credit limit).

Credit limit

The amount of available funds within the limit established by the agreement is, in fact, a consumer loan without guarantors and collateral.

The contract must include:

- interest,

- date of monthly payment,

- repayment procedure,

- procedure for calculating the next payment,

- commissions for the main types of transactions.

The limit can be revised by the bank at regular intervals. The client himself can initiate such a procedure by submitting an application to the bank. In this case, the bank may take into account additional documents confirming the client's solvency or the level of his permanent income.

The moment of issuing such a loan can be considered the issuance of cash in self-service devices or payment for goods/services from the funds of the limit.

In the first case (cash withdrawal), banks often charge additional fees (for example, a fixed minimum payment) and also do not provide a grace period.

In the second, when paying from the account, the commission may be less or completely absent, and a deferral is provided for the funds used (the period and the countdown procedure are described in the agreement).

- If, within the specified period, the funds are deposited to the card account in full, then the interest on the loan will not be charged.

- If the funds are partially deposited, the interest will be calculated based on the difference between the amount originally taken and deposited later.

Credit card details

The appearance of credit cards is no different from other bank cards. Of the main details, the following are applied to the credit card:

- number (13, 16 or 19 characters, most often 16);

- BIN of the bank that issued the card;

- expiration date;

- surname and name of the owner in Latin;

- additional identification code (CVV, CSC, CVC or other analogs);

- payment system logo and type of card product;

- client's signature.

The card can be equipped with:

- chip,

- magnetic stripe,

- the NFC module.

PAYMENT SYSTEM QIWI

QIWI is a Russian multi-platform payment system launched in 2007. Initially, the business was based on a large network of payment terminals through which it was possible to replenish a mobile phone account, pay fines and make other payments.

However, in 2004 the brand joined forces with the international system Visa, and "QIWI Wallet" acted as a co-branded product (Visa QIWI Wallet), providing users with all the capabilities of bank cards.

Currently, the QIWI brand belongs to the United System of Instant Payments CJSC. The latter also owns: Qiwi Bank (it was he who bought the Tochka service for entrepreneurs from Otkritie FC, and also acquired Rapida, another payment system), Qiwi Advertising, the payment service of the same name, two lottery organizers (Lotto Master "and" Lotto Integrator ") and the supplier of fiscal registrars Paykiosk.

There are about 150 thousand terminals in the self-service points network. The turnover of the system in 2017 is more than 910 billion rubles, the net profit of the service in the same year is 4 billion rubles.

The geography of presence has increased to 17 countries (in 9 of them, services are provided by companies operating under a franchise).

Key features of the QIWI service

Payment for goods and services from an e-wallet account (including banking services, housing and communal services, services of companies providing communications and Internet access, as well as fines).

- Transfers (involving cards and electronic wallets).

- Issuance of virtual cards linked to an electronic wallet.

- Issue of physical bank cards Visa (unnamed, registered or with nicknames for gamers, as well as with payment by installments - the "Conscience" card).

- Funding the account in a variety of ways (from bank transfers to payment from a mobile phone account).

- Application for mobile phones with support for contactless payment (NFC) and special authorization technology in payment terminals (by QR code).

BANK CARD

A bank card is a unique identifier of the user/account and the bank in which it is served, most often printed on a plastic card of a given format. The card does not have to be physical, it can be virtual, then the issue (issue) of the card will actually represent the issuance by the bank of a unique number to the user and other details necessary for making payments. Several current accounts can be linked to the same customer number at once. Thanks to the card number, banks can correlate the current account with the operation being carried out (debit or credit).

The format of the card is defined by the ISO/IEC 7810 standard. The dimensions specified in it are indicated in the image below.

Bank card sizes.

The most common format is ID-1 (85.60 ? 53.98 mm, with a thickness of 0.76 mm).

Attributes

The most important attribute applied to the card is the number. But he's not the only one. Additionally, the following information can be applied:

- Expiration date (validity can be from 1 year to 5 years).

- Security code (three-digit number on the back, used for authentication).

- Holder name (optional).

- Owner's signature field (optional).

- The card can be equipped with:

- Magnetic stripe.

- Microprocessor/chip.

- One-time password generator (with a built-in display) and a keyboard for entering a permanent one.

- NFC module (to support contactless payments).

Number

The number can be represented as a sequence of 13, 16 or 19 digits. The most common are sixteen-digit numbers. The rest have already practically gone out of circulation.

The rules for generating numbers are described in the international standard ISO/IEC 7812.

The sequence is written in four blocks of 4 digits. The information that is recorded in the number can be designated as follows:

Decoding the number on the bank card.

- The first number reflects the industry of the issuer (for example, 4 and 5 - banking and finance).

- The first 6 digits are the bank identifier (BIN or Issuer identifier number/IIN).

- The next 9 digits are the Individual account identification.

- The last digit is the check one.

Views

Bank cards can be:

Depending on the territory of action

- local (operating on the territory of one state/region),

- global (accepted worldwide).

By type of settlement

- Debit (contact a special bank account, debit transactions are made only within the available balance).

- Credit (linked to a pre-approved credit limit).

- Debit with overdraft (combine the properties of the first and second cards).

- Prepaid/Gift (cards without a fixed owner, linked to an impersonal account).

- Virtual (most often these are debit or prepaid cards, which are issued without a plastic carrier, are used for transactions on the Internet).

By appointment

- for payments (in trade and service enterprises, in online stores);

- for the accumulation of funds (can contact the deposit);

- for business needs (corporate cards/business cards, cards for collection);

- social (for the payment of pensions, scholarships to students);

- salary (most often debit);

- to form an additional security factor (with a built-in one-time password generator).

Loyalty programs

To attract a new audience, payment systems often hold their own promotions (in cooperation directly with their partners).

However, banks themselves often stimulate the demand for card products by:

- Issue of co-badging cards (they can work in several payment systems at once).

- Issuing cards in cooperation with their partners (large merchants offering miles accumulation, getting discounts on certain services, etc.).

- Carrying out one-time or periodic promotions with discounts.

- Bonus systems (accumulation of points converted into discounts).

- Cashback.

- Interest on the balance.

- Free service (subject to special conditions for the volume of transactions and/or account balances).

BITCOIN MINING

To avoid chaos in the Bitcoin network, only one member of the network shares the information collected about transactions at a given time, and the rest update their records based on his data packet. This stage is called mining. Such a member of the network is chosen at random.

When a block is created, its author receives a reward for the successful execution of mathematical operations, this is the first transaction of the block. Then, other translations that have not yet been entered into any block are written into the block. The block creator can control the composition of the block and select transactions.

The unit of measurement for mining performance is hash per second (hash/s), which also means one of the parameters of the power of a graphics card. GPU resources are used to compute the hash, which leads to the formation of a new block. However, the more people who want to create blocks, the less chances miners with home computers have - you can already find companies selling equipment or data center capacities specifically for mining. This leads to the fact that the probability of outperforming a more powerful processor in performing the same operation is reduced to almost zero.

In addition to the task to calculate the hash with the correct amount, when creating a block, there is a "complexity" parameter that adjusts the numerical value of the result. The lower the target value, the more difficult it is to complete the task. Approximately every 2 weeks, the system complicates the requirements for new block headers to maintain an average speed of 1 block per 10 minutes. Additionally, it is worth noting that the hash result is completely unpredictable, which makes it impossible to cheat to achieve the desired result.

It is possible to form blocks at the same time, which leads to branching, since several blocks consider the same fragment of the chain as a parent due to the parallel formation of blocks by all miners.

Moreover, it is theoretically possible to gain control over the entire system: if you control more than 50% of the power of the bitcoin network, then the chain of transactions created by the fraudster with incorrect data will be accepted by the “correct” part of the network as the main one, since the system considers the longer blockchain correct. Operations that are not included in the main branch are queued for inclusion in a new block, but the reward for them is not repeated, which explains how bitcoins can disappear.

To prevent the value of Bitcoin from decreasing, the system is programmed to automatically reduce the amount of reward for creating a block by half every several years. And there is also a limit on the maximum number of bitcoins in the system: 21 million. This figure is the sum of the members of a decreasing geometric progression. Initially, for each new block, you could get 50 units of cryptocurrency. Then twice more the bonus was cut in half - again a decreasing geometric progression. It is easy enough to predict that by 2031 bitcoins will no longer be profitable when creating new blocks, since the reward will not exceed 1 bitcoin.

To simplify the mining task, pools have been created that consolidate small miners and are visible to the system as one miner with huge computing power. Upon successful block generation, the reward is distributed among the pool members. Lack of pool membership - too little bonus per block.

It is becoming clear that the time has come to stimulate such an ardent interest in cryptocurrencies with new ways of income. Several years ago, “other” cryptocurrencies appeared, based on the same technology, but with different scripts and some features. We will talk about them in a separate article.

CHARGEBACK (RETURN)

Chargeback is a back money, the term is used exclusively in relation to transactions with card accounts (bank cards). This procedure is designed to protect the cardholder from direct (without the owner's permission or consent) debiting of funds from the account. A harder version of the refund.

It is the responsibility of the recipient to prove the correctness of the payment. The procedure is initiated by the owner of the bank card through the issuing bank.

Refunds are possible when using such international payment systems as VISA and MasterCard. The Russian payment system Mir is no exception (here the term “dispute” appears instead of the term “chargeback”).

The bank cannot refuse to initialize the refund procedure, since when connected to the payment system, it accepts the rules of the latter, in which this procedure is explicitly spelled out.

The most common causes of chargeback

- Double write-off of the purchase amount for one product (service).

- The transaction was not authorized.

- The product/service does not correspond to the declared description.

- The goods were not delivered (service was not provided) or not delivered in full.

The processing time for applications for refunds can be about 120 days (VISA) or 180 days (MasterCard). The Mir system stipulates a “reasonable time frame”. However, for most standard operations, the chargeback procedure is performed within 30 days.

BITCOIN

You will learn:

- What is Bitcoin?

- How do you earn it?

- How to use it

- What is its future?

Perhaps it would be nice to invent an analogue of cash for the Internet. Pay in a couple of clicks without confirming your identity and commission, store money on your computer with the possibility of instant sale or exchange. And also so that this currency is independent of the banking system of any state.

This is how Bitcoin can be described in a nutshell. The emergence of such a means of payment is a logical step in the development of mathematical algorithms on which many modern technologies are based, especially around large amounts of data.

What is Bitcoin?

First of all, any cryptocurrency is an uncontrolled payment instrument for carrying out p2p transactions (between users), available only online, which, among other things, has no restrictions on emission, countries of work or requirements for currency holders.

Bitcoin payments are made directly between the owners of special wallets, in the sense of similar to Internet wallets for electronic money (QIWI, WebMoney, Yandex.Money). However, the payment process takes place without the involvement of intermediate participants such as settlement banks or payment system aggregators in the scenario of accepting payments in favor of the online store.

The anonymity of virtual money is ensured by a digital signature. Anyone can understand from what name of which wallet (address) the message is written. This is similar to the nickname in your favorite game, only without the possibility of fake. Checking the integrity of the message is provided by the hashing method - the assignment of a numerical code to the data, calculated mathematically. In addition, each member of the network maintains its own records of all members of the network and their operations. Records of completed transactions are transmitted in batches (blocks) between all participants in the system.

The cryptocurrency is decentralized, i.e. no one controls the issue and movement of funds. Any money we all are used to can be artificially devalued by the Central Banks: it is enough to print an excess number of monetary units, for example, to cover the public debt. This means that anyone can print, or rather create from nowhere (extract) bitcoins by connecting to a special network.

Since transfers are generally carried out without intermediaries, the commission can be equated to zero, which adds to the advantages of cryptocurrency in comparison with traditional means of payment. Of course, for exchanging virtual currency for dollars or euros, each platform charges its own percentage. However, in relation to the total turnover, these figures are not much more than zero.

Thanks to the transfer to the recipient's account through the processing of the transaction by the network and the elimination of dependence on banks, the transfer reaches the recipient's address instantly.

The differences between virtual currency do not end there. While a credit card payment can always be revoked in the event of an error, this is not possible for Bitcoin, which allows the possibility of fraud without any protection or insurance, as would be the case when using 3DS in card transactions.

How to earn bitcoins?

Basic cryptocurrencies do not imply the accrual of interest on the account balance, which makes it difficult to make a profit. However, some exchanges or wallet management platforms offer bonus "pennies": a bitcoin unit can be divided, for example, as a pound into cents - 1 satoshi (satoshi) is 0.00000001 BTC. The bonus can be obtained for clicks on banners, transitions to advertising sites, creating a new wallet or other fairly simple actions on special sites - bitcoin "faucets", English. Bitcoin faucet,).

You can usually get about 0.0001 bitcoins for free and with little or no effort, but if you are lucky, you will encounter a bonus that is closer to a whole unit of cryptocurrency. Unfortunately, withdrawing the trophy right away is not always allowed by the rules of sites that distribute "crypto kopecks": you will first have to accumulate at least 0.001 BTC. In addition, you cannot endlessly receive, albeit a small, but free reward - you can often find a time limit until the next opportunity to receive a task. And yet, the freedom of action is not limited in everything: for a referral brought into the system, you can usually get a bonus too. And to simplify the process of mining cryptocurrency in this way, aggregators have appeared that allow you to log in to several sites of this topic at the same time and switch between them much faster.

Like other currencies, bitcoins are traded on special exchanges, which makes it possible to earn money, if, of course, you are familiar with this area of activity. When there was enough virtual money for people to buy it, bitcoin exchanges opened, which also means the formation of the starting market price. Now the rise in prices for bitcoin is fantastically rapid and looks like blowing up another economic bubble, but experts disagree on the likelihood that it will burst in the near future. Some people compare the rampant interest in cryptocurrencies with pyramid schemes.

In addition to sites with free bonus satoshi, it is possible to receive bitcoins from other holders as a donation or incoming payment. To do this, it is enough to provide a "wallet number" - your address in the bitcoin network.