Carding Forum

Professional

- Messages

- 2,788

- Reaction score

- 1,330

- Points

- 113

Today, money can be transferred to another country quickly, and sometimes even free of charge. But have international money transfers always been like this?

How technology affects remittances.

The history of money transfers goes back more than one century - people have long been looking for a way to transfer money abroad without leaving their city. With the development of technology, new ways of transfers have appeared. In this article, we'll look at how innovation has impacted money exchange.

Until a few centuries ago, money transfers were the prerogative of banks. Sometimes they were made only within one country or only between the accounts of one financial institution. Also, some of the translations were carried out by postal operators. Together with the correspondence, the postman could transfer cash or a document prescribing how much money should be given to the recipient from the cash register.

However, this all changed at the beginning of the industrial era. Remittances in the modern sense originated in the 19th century as a response to globalization. More and more people began to work with foreign contractors - there was a need for fast and reliable ways to transfer funds both between companies and between ordinary people who massively immigrated in search of work abroad.

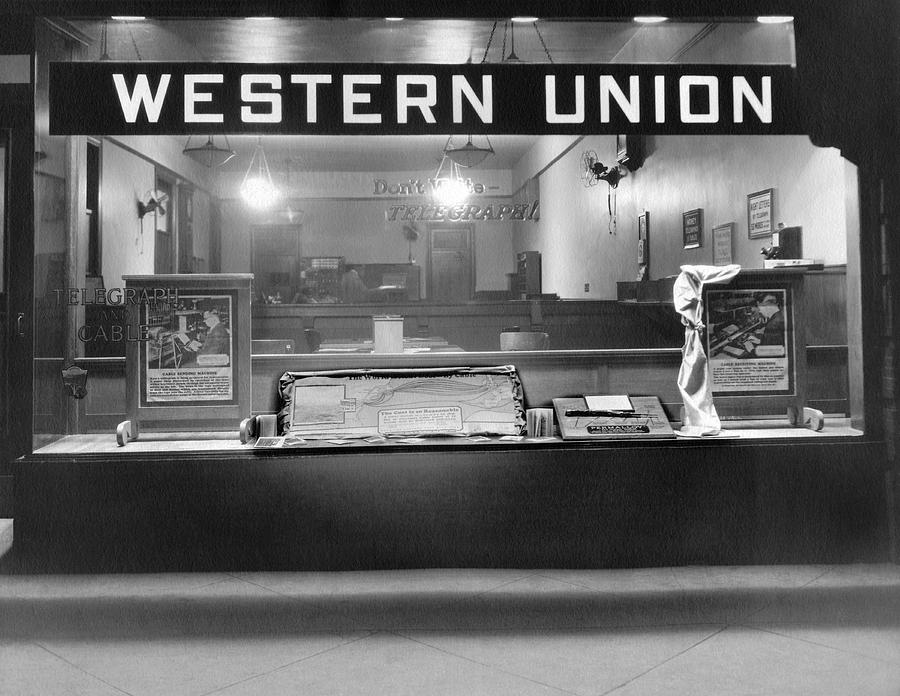

WU Telegraph Office

The first technology to change the usual format of money transfers was the telegraph. In 1871, Western Union (then the telegraph operator on the West Coast of the United States) made the first "wire" money transfer using Morse code. The company accepted and issued cash through its network of telegraph offices throughout the United States. And the information about the amount was transmitted by telegram. A little later, the format was improved - with the advent of Telex in 1926, messages were transmitted using teleprinters. This system was used by banks and money transfer services such as WU.

Teleprinter

After telephone, and subsequently e-mail, replaced the telegraph, money transfers became the main business of Western Union. Since the 1990s, the company has been actively developing in the financial direction. And in 2006 it completely refused to send telegrams.

Therefore, in 1973, a new messaging platform was created - SWIFT. It has enabled banks around the world to send and receive information about financial transactions in a standardized, secure and reliable environment. SWIFT currently has over 10,000 members in over 200 countries. The site processes more than 15 million messages daily. Any financial institution holding a banking license can become a SWIFT member by paying an entry fee and service fee for each message sent.

Despite the fact that SWIFT has resolved the issue of standardizing messages between banks, over time, this payment system also showed drawbacks - the speed and cost of sending transactions. The system tries to solve some of these problems on its own by launching new products. Some are decided by other companies, competing with SWIFT.

PayPal co-founder Peter Thiel and Elon Musk

PayPal was founded in 1998. In fact, it was the first well-known company dealing with cheap and fast (compared to banks of the time) money transfers on the Internet. The system is currently used all over the world mainly for individual transfers and e-commerce. Also, new companies appear on the market that provide fast transfer of funds. For example, TransferWise, CurrencyFair, and TransferGo operate with clearly marked exchange rates and user-friendly interfaces that facilitate international money transfers. Most of these companies charge low fees or even offer the service for free. For example, TransferGo, instead of transferring funds, accepts a deposit into its local bank account and makes a payment to the recipient from its bank account in that person's country.

Before the advent of SWIFT gpi, each bank could not tell the sender the exact time of receipt of funds, the commission for the payment and the success of the transaction in general. After all, the financial institution had information only on its side and could not predict how the correspondent bank and the receiving bank of the transfer would behave.

SWIFT gpi changed the situation - participating banks were able to familiarize themselves with the payment route even before it was sent. This standard made the payment more transparent and predictable for the bank and the client.

Half of global SWIFT payments have already switched to the new standard. Last year, it was even implemented by one bank. In 2021, more than $ 40 trillion was transferred through the SWIFT gpi service.

The only question is whether the new system will be able to bypass SWIFT in popularity and connect a sufficient number of clients. Indeed, now the services of the traditional service are used by 10 thousand banks all over the planet.

In 2021, a number of traditional banks and money transfer services joined Ripple. Most often they use three main Ripple products: XCurrent, XRapid, and XVia.

XCurrent allows the transmission of transaction messages based on the Ripple distributed ledger. Using XCurrent, only fiat currencies can be transferred. Payments are made in real time. More than 120 world banks, payment operators and financial and credit corporations work on xCurrent. Among them are Banco Santander, PNC Financial Services and TransferGo, which previously launched free transfers to India based on this technology.

The technology allows you to process payments in a 24/7 format. While the transfer of money between banks located in different time zones can be delayed due to non-operational time in one of the financial institutions.

XRapid integrates XRP token into a bank transaction. This allows you to reduce the cost of payment processing by 70%, and the processing time of the transaction - up to several minutes. After all, XRapid allows you to convert traditional money into XRP token and make a transfer in cryptocurrency. The testing of this system has already been reported by MoneyGram and Western Union.

We are piloting Ripple-based transfers for some payment corridors. Among them are the US dollar and the Mexican peso. The options we have selected must be compliant with regulatory requirements and be as appropriate as possible for widespread use.

XVia helps large money transfer companies access information in banks. xVia offers a simple interface that allows customers to send international payments with detailed billing information. The project was supported by European and Asian transfer operators FairFX, RationalFX, Exchange4Free, UniPAY and MoneyMatch in order to reduce operating costs, increase transfer speed and transparency of payment traffic.

Banks and financial companies continue to experiment with blockchain and other technologies. As with other financial innovations, the effect of this collaboration can only be appreciated over time.

How technology affects remittances.

The history of money transfers goes back more than one century - people have long been looking for a way to transfer money abroad without leaving their city. With the development of technology, new ways of transfers have appeared. In this article, we'll look at how innovation has impacted money exchange.

Until a few centuries ago, money transfers were the prerogative of banks. Sometimes they were made only within one country or only between the accounts of one financial institution. Also, some of the translations were carried out by postal operators. Together with the correspondence, the postman could transfer cash or a document prescribing how much money should be given to the recipient from the cash register.

However, this all changed at the beginning of the industrial era. Remittances in the modern sense originated in the 19th century as a response to globalization. More and more people began to work with foreign contractors - there was a need for fast and reliable ways to transfer funds both between companies and between ordinary people who massively immigrated in search of work abroad.

Telegraph and Western Union

WU Telegraph Office

The first technology to change the usual format of money transfers was the telegraph. In 1871, Western Union (then the telegraph operator on the West Coast of the United States) made the first "wire" money transfer using Morse code. The company accepted and issued cash through its network of telegraph offices throughout the United States. And the information about the amount was transmitted by telegram. A little later, the format was improved - with the advent of Telex in 1926, messages were transmitted using teleprinters. This system was used by banks and money transfer services such as WU.

Teleprinter

After telephone, and subsequently e-mail, replaced the telegraph, money transfers became the main business of Western Union. Since the 1990s, the company has been actively developing in the financial direction. And in 2006 it completely refused to send telegrams.

SWIFT and banks

Already in the second half of the century, it became clear that telegraph communication was slow. Moreover, it does not have a standardized and secure format for the transmitted data. This is ineffective and dangerous for bank money transfers.Therefore, in 1973, a new messaging platform was created - SWIFT. It has enabled banks around the world to send and receive information about financial transactions in a standardized, secure and reliable environment. SWIFT currently has over 10,000 members in over 200 countries. The site processes more than 15 million messages daily. Any financial institution holding a banking license can become a SWIFT member by paying an entry fee and service fee for each message sent.

Despite the fact that SWIFT has resolved the issue of standardizing messages between banks, over time, this payment system also showed drawbacks - the speed and cost of sending transactions. The system tries to solve some of these problems on its own by launching new products. Some are decided by other companies, competing with SWIFT.

International money transfers online

To send a SWIFT transfer, you need to know the recipient's full bank details, wait a few days and pay a fairly high commission. Therefore, two decades after the launch of SWIFT, there were companies on the market that solved these problems.

PayPal co-founder Peter Thiel and Elon Musk

PayPal was founded in 1998. In fact, it was the first well-known company dealing with cheap and fast (compared to banks of the time) money transfers on the Internet. The system is currently used all over the world mainly for individual transfers and e-commerce. Also, new companies appear on the market that provide fast transfer of funds. For example, TransferWise, CurrencyFair, and TransferGo operate with clearly marked exchange rates and user-friendly interfaces that facilitate international money transfers. Most of these companies charge low fees or even offer the service for free. For example, TransferGo, instead of transferring funds, accepts a deposit into its local bank account and makes a payment to the recipient from its bank account in that person's country.

New SWIFT - Swift gpi

Despite strong competition, SWIFT is finding new ways of profitable money transfers. The SWIFT GPI system was launched two years ago in response to the growing popularity of fast money transfer services and cryptocurrency platforms like Ripple.Before the advent of SWIFT gpi, each bank could not tell the sender the exact time of receipt of funds, the commission for the payment and the success of the transaction in general. After all, the financial institution had information only on its side and could not predict how the correspondent bank and the receiving bank of the transfer would behave.

SWIFT gpi changed the situation - participating banks were able to familiarize themselves with the payment route even before it was sent. This standard made the payment more transparent and predictable for the bank and the client.

Half of global SWIFT payments have already switched to the new standard. Last year, it was even implemented by one bank. In 2021, more than $ 40 trillion was transferred through the SWIFT gpi service.

Blockchain payments

Along with SWIFT GPI, another system for sending money transfers is developing - Ripple. The company promises even cheaper and faster transfers through the use of blockchain technology.The only question is whether the new system will be able to bypass SWIFT in popularity and connect a sufficient number of clients. Indeed, now the services of the traditional service are used by 10 thousand banks all over the planet.

In 2021, a number of traditional banks and money transfer services joined Ripple. Most often they use three main Ripple products: XCurrent, XRapid, and XVia.

XCurrent allows the transmission of transaction messages based on the Ripple distributed ledger. Using XCurrent, only fiat currencies can be transferred. Payments are made in real time. More than 120 world banks, payment operators and financial and credit corporations work on xCurrent. Among them are Banco Santander, PNC Financial Services and TransferGo, which previously launched free transfers to India based on this technology.

The technology allows you to process payments in a 24/7 format. While the transfer of money between banks located in different time zones can be delayed due to non-operational time in one of the financial institutions.

XRapid integrates XRP token into a bank transaction. This allows you to reduce the cost of payment processing by 70%, and the processing time of the transaction - up to several minutes. After all, XRapid allows you to convert traditional money into XRP token and make a transfer in cryptocurrency. The testing of this system has already been reported by MoneyGram and Western Union.

We are piloting Ripple-based transfers for some payment corridors. Among them are the US dollar and the Mexican peso. The options we have selected must be compliant with regulatory requirements and be as appropriate as possible for widespread use.

XVia helps large money transfer companies access information in banks. xVia offers a simple interface that allows customers to send international payments with detailed billing information. The project was supported by European and Asian transfer operators FairFX, RationalFX, Exchange4Free, UniPAY and MoneyMatch in order to reduce operating costs, increase transfer speed and transparency of payment traffic.

Banks and financial companies continue to experiment with blockchain and other technologies. As with other financial innovations, the effect of this collaboration can only be appreciated over time.