Carding Forum

Professional

- Messages

- 2,788

- Reaction score

- 1,322

- Points

- 113

The analytical company J'son & Partners Consulting presented the results of a study of the contactless payment market in the world. According to experts, the share of non-cash payments is growing every year, since they ensure the efficiency, reliability and speed of transactions necessary for the development of a modern economy.

According to the report, despite the emergence of new remote payment services operating on the principle of scanning barcodes or QR codes for payment, most contactless transactions are made using NFC technology.

In addition to bank cards with contactless technology, payments using a mobile phone and other wearable devices are now becoming widespread. The use of contactless payment technology can significantly reduce the time of customer service in retail, HoReCa (hotels and restaurants) and public transport.

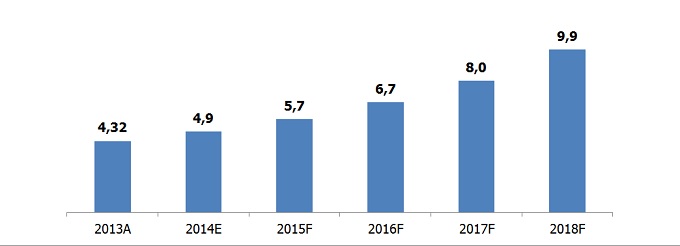

According to experts, in 2020 the turnover of contactless payments in the world amounted to about $ 4.9 billion, and by 2025 it will approach $ 10 billion. The number of installed POS-terminals with NFC support in the world in 2020 increased by 71% and amounted to 21.4 million devices, and by 2019 their number will be 75 million, which will correspond to an average annual growth rate of 28.4%.

Dynamics of the global contactless payment market, billion dollars. Sources: MarketsandMarkets, J'son & Partners Consulting

However, many POS terminals equipped with NFC technology are not used for such operations. Thus, according to Berg Insight estimates, in 2020 only 9 million POS terminals made contactless payments.

Contactless payments affect such areas of activity as transport and logistics, IT and telecommunications services, consumer goods and retail trade, government services and housing and communal services, banking and financial institutions, etc.

Mobile contactless payment market

According to Deloitte estimates, by the end of 2015, 5% of smartphone users with NFC will make contactless transactions at points of sale at least once a month, while in mid-2014 only 0.5% made such transactions. According to Strategy Analytics forecasts, the turnover of mobile NFC payments will reach $ 130 billion by 2020.

At the moment, three major players are entering the market for such payments in the world: Apple, Google and Samsung with Apple Pay systems (the system was launched on October 20, 2014), Android Pay (launched in May 2021) and Samsung Pay (the system will be launched summer 2021), respectively. It should be noted that the Samsung Pay system, in addition to NFC, uses MST (Magnetic secure transmission) technology, which allows a portable device to imitate a regular bank card.

In addition, the latest versions of Android systems have a built-in Google Wallet API that allows you to create applications that provide the user with the ability to make mobile payments, not only using NFC, but also on the Internet.

According to the analytical agency ITG, since the launch of Apple Pay in the United States, by December 2020, about 1.7% of digital payments made in the country passed through the system.

Mobile contactless payment security

The security of such transactions is carried out using a secure module (SE) - a tamper-resistant chip that provides secure storage, payment transactions and storage of confidential data.

When using Host Card Emulation (HCE) technology, which allows emulating a bank card on a phone or tablet, the secure module is virtual and resides in the cloud.

HCE has an open architecture, which allows emulating not only bank cards, but also loyalty program cards, transport cards, passes, etc. The technology allows you to significantly speed up the process of implementing NFC payment services, since there is no need for coordination and coordination with manufacturers phones, in addition, many compatibility problems are solved.

SE and HCE technologies differ significantly, with each having both advantages and disadvantages. HCE allows not only making payments on physical POS terminals like SE, but also making Internet transactions on websites and in applications, however, it is more vulnerable to malware and critical to the presence of an Internet connection.

According to the report, despite the emergence of new remote payment services operating on the principle of scanning barcodes or QR codes for payment, most contactless transactions are made using NFC technology.

In addition to bank cards with contactless technology, payments using a mobile phone and other wearable devices are now becoming widespread. The use of contactless payment technology can significantly reduce the time of customer service in retail, HoReCa (hotels and restaurants) and public transport.

According to experts, in 2020 the turnover of contactless payments in the world amounted to about $ 4.9 billion, and by 2025 it will approach $ 10 billion. The number of installed POS-terminals with NFC support in the world in 2020 increased by 71% and amounted to 21.4 million devices, and by 2019 their number will be 75 million, which will correspond to an average annual growth rate of 28.4%.

Dynamics of the global contactless payment market, billion dollars. Sources: MarketsandMarkets, J'son & Partners Consulting

However, many POS terminals equipped with NFC technology are not used for such operations. Thus, according to Berg Insight estimates, in 2020 only 9 million POS terminals made contactless payments.

Contactless payments affect such areas of activity as transport and logistics, IT and telecommunications services, consumer goods and retail trade, government services and housing and communal services, banking and financial institutions, etc.

Mobile contactless payment market

According to Deloitte estimates, by the end of 2015, 5% of smartphone users with NFC will make contactless transactions at points of sale at least once a month, while in mid-2014 only 0.5% made such transactions. According to Strategy Analytics forecasts, the turnover of mobile NFC payments will reach $ 130 billion by 2020.

At the moment, three major players are entering the market for such payments in the world: Apple, Google and Samsung with Apple Pay systems (the system was launched on October 20, 2014), Android Pay (launched in May 2021) and Samsung Pay (the system will be launched summer 2021), respectively. It should be noted that the Samsung Pay system, in addition to NFC, uses MST (Magnetic secure transmission) technology, which allows a portable device to imitate a regular bank card.

In addition, the latest versions of Android systems have a built-in Google Wallet API that allows you to create applications that provide the user with the ability to make mobile payments, not only using NFC, but also on the Internet.

According to the analytical agency ITG, since the launch of Apple Pay in the United States, by December 2020, about 1.7% of digital payments made in the country passed through the system.

Mobile contactless payment security

The security of such transactions is carried out using a secure module (SE) - a tamper-resistant chip that provides secure storage, payment transactions and storage of confidential data.

When using Host Card Emulation (HCE) technology, which allows emulating a bank card on a phone or tablet, the secure module is virtual and resides in the cloud.

HCE has an open architecture, which allows emulating not only bank cards, but also loyalty program cards, transport cards, passes, etc. The technology allows you to significantly speed up the process of implementing NFC payment services, since there is no need for coordination and coordination with manufacturers phones, in addition, many compatibility problems are solved.

SE and HCE technologies differ significantly, with each having both advantages and disadvantages. HCE allows not only making payments on physical POS terminals like SE, but also making Internet transactions on websites and in applications, however, it is more vulnerable to malware and critical to the presence of an Internet connection.