Carding Forum

Professional

- Messages

- 2,788

- Reaction score

- 1,323

- Points

- 113

What new industries are banks developing and why do they need it?

More than banks: what new areas are financial institutions mastering?

Banking institutions are increasingly not only working to maintain the loyalty of their customers, but also entering new, non-traditional markets for them.

PaySpace Magazine has studied which non-banking services are gaining popularity among financial institutions.

Why do banks need it

The competition in the banking sector is getting more and more every day. Both in the world in general and in particular.

Financial institutions improve their websites and mobile applications, add services that are in demand (Apple Pay, Google Pay), and quickly respond to changes in laws.

For example, after the Law on Currency and Foreign Exchange Operations came into force, a little more than a week has passed, and more than seven banks have already presented one of the most popular functionality among consumers - online currency exchange. Some did it at exactly 12 at night on February 7.

Many banks have introduced functionality for online currency exchange.

Timely response to changes in the financial market allows banks to stay “on a par” with competitors. But to get better, they need to expand the range of services and opportunities they provide.

In addition, one should not forget about the growing competition from fintech companies, as well as ignore the fact that non-financial IT companies are gradually beginning to experiment with their own payment instruments.

Examples of that are Amazon, which at the end of 2018 was seriously engaged in the development of its payment system Amazon Pay, and Alibaba Group, whose Alipay system is being developed in more and more countries.

Sales

By the way, about Amazon and Alibaba. As sales companies enter the financial market, banks are gradually becoming interested in sales.

The key word here is "little by little." Banks do not plan to compete with retail giants, but they do not mind making the sale of goods and services another source of income.

Although, it is worth noting that some banks do go further. For example, Market from Bank is a full-fledged marketplace that allows you to buy goods from sellers both at full price and in installments.

However, it is difficult to talk about the profitability of such a solution without statistics due to the presence of fairly strong competitors in the face of Rozetka and EVO.company marketplaces.

Insurance

One of the areas that more and more banks are seeing as promising is insurance. There is even a separate term for this type of service - bancassurance (bank insurance).

Organization of a system for cross-selling insurance policies through an extensive network of banking divisions / branches or the acquisition by a bank of insurance companies already operating in the market

Bancassurance (bank insurance).

Banks do not need to create a subsidiary and spend additional time and resources to obtain licenses for the provision of various types of insurance services. Banks act as intermediaries between the client and the insurance company.

Both parties benefit from this collaboration. Banks - increased liquidity, insurance - an increase in the number of customers and points of sale.

Venture investments

With the number of new startups popping up every day, it's not surprising that many banking institutions are interested in venture capital investments.

Banks provide funds for starting new businesses with a high level of risk, counting on a high profitability of their investments.

But money isn't the only reason banks get venture capital investments. Oddly enough, many financial institutions invest in their seemingly competitors - in fintech startups.

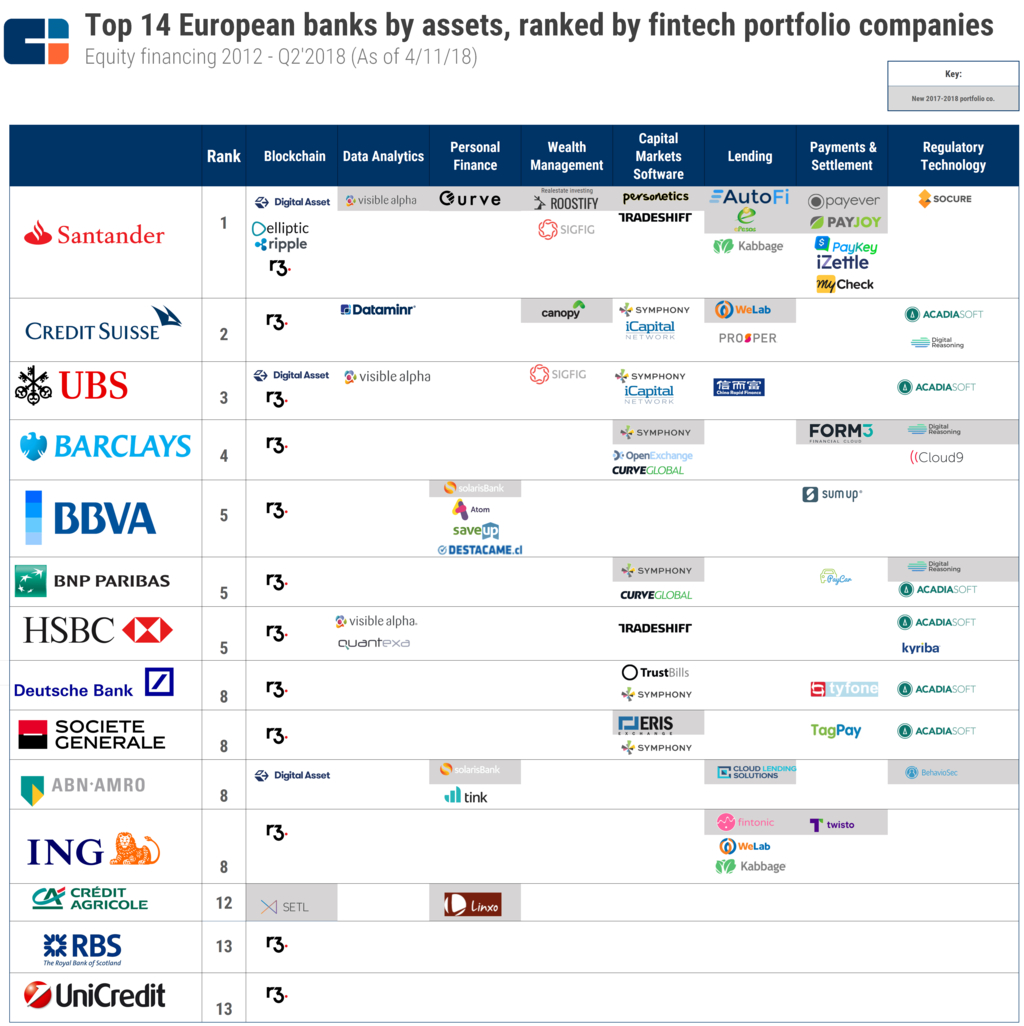

This is confirmed by data from CB Insights. The portal's analysts have studied which fintech startups the top European banks have invested in:

In the future, a financial product or technology created by a young company can be introduced or used in a banking institution. This will save the time and money required to develop such a product from scratch.

VIP services

The provision of additional services for premium clients is also very popular with financial institutions. The VIP-class card differs in price (most often a standard monthly payment or the presence of a deposit for a minimum amount determined by the bank) and an abundance of additional services.

Each bank tries to add something of its own to the standard package. Among the most popular:

And even that's not all

Separately, it is worth remembering the offline services provided at the cash desks of banks. For example, utility bills and money transfers.

Also, among insolvent banks at one time, direct sales of property were popular: office equipment, bank safes, ATMs, furniture and others.

The list goes on and on. Now it is very difficult to identify any trends in the choice of markets or service sectors that financial institutions are beginning to master.

To increase liquidity and greater customer loyalty, banks try to "be where their potential customer is." And, if you do not win back part of the audience, then at least become an intermediary between the client and the company whose services he needs.

More than banks: what new areas are financial institutions mastering?

Banking institutions are increasingly not only working to maintain the loyalty of their customers, but also entering new, non-traditional markets for them.

PaySpace Magazine has studied which non-banking services are gaining popularity among financial institutions.

Why do banks need it

The competition in the banking sector is getting more and more every day. Both in the world in general and in particular.

Financial institutions improve their websites and mobile applications, add services that are in demand (Apple Pay, Google Pay), and quickly respond to changes in laws.

For example, after the Law on Currency and Foreign Exchange Operations came into force, a little more than a week has passed, and more than seven banks have already presented one of the most popular functionality among consumers - online currency exchange. Some did it at exactly 12 at night on February 7.

Many banks have introduced functionality for online currency exchange.

Timely response to changes in the financial market allows banks to stay “on a par” with competitors. But to get better, they need to expand the range of services and opportunities they provide.

In addition, one should not forget about the growing competition from fintech companies, as well as ignore the fact that non-financial IT companies are gradually beginning to experiment with their own payment instruments.

Examples of that are Amazon, which at the end of 2018 was seriously engaged in the development of its payment system Amazon Pay, and Alibaba Group, whose Alipay system is being developed in more and more countries.

Sales

By the way, about Amazon and Alibaba. As sales companies enter the financial market, banks are gradually becoming interested in sales.

The key word here is "little by little." Banks do not plan to compete with retail giants, but they do not mind making the sale of goods and services another source of income.

Although, it is worth noting that some banks do go further. For example, Market from Bank is a full-fledged marketplace that allows you to buy goods from sellers both at full price and in installments.

However, it is difficult to talk about the profitability of such a solution without statistics due to the presence of fairly strong competitors in the face of Rozetka and EVO.company marketplaces.

Insurance

One of the areas that more and more banks are seeing as promising is insurance. There is even a separate term for this type of service - bancassurance (bank insurance).

Organization of a system for cross-selling insurance policies through an extensive network of banking divisions / branches or the acquisition by a bank of insurance companies already operating in the market

Bancassurance (bank insurance).

Banks do not need to create a subsidiary and spend additional time and resources to obtain licenses for the provision of various types of insurance services. Banks act as intermediaries between the client and the insurance company.

Both parties benefit from this collaboration. Banks - increased liquidity, insurance - an increase in the number of customers and points of sale.

Venture investments

With the number of new startups popping up every day, it's not surprising that many banking institutions are interested in venture capital investments.

Banks provide funds for starting new businesses with a high level of risk, counting on a high profitability of their investments.

But money isn't the only reason banks get venture capital investments. Oddly enough, many financial institutions invest in their seemingly competitors - in fintech startups.

This is confirmed by data from CB Insights. The portal's analysts have studied which fintech startups the top European banks have invested in:

In the future, a financial product or technology created by a young company can be introduced or used in a banking institution. This will save the time and money required to develop such a product from scratch.

VIP services

The provision of additional services for premium clients is also very popular with financial institutions. The VIP-class card differs in price (most often a standard monthly payment or the presence of a deposit for a minimum amount determined by the bank) and an abundance of additional services.

Each bank tries to add something of its own to the standard package. Among the most popular:

- Priority Pass

- personal concierge and personal banker

- discounts on goods and services of partners

- safe deposit box rental

- collection and security service for the transportation of large amounts or valuables

- increased amount of insurance

- urgent cash withdrawal anywhere in the world in case of card loss

And even that's not all

Separately, it is worth remembering the offline services provided at the cash desks of banks. For example, utility bills and money transfers.

Also, among insolvent banks at one time, direct sales of property were popular: office equipment, bank safes, ATMs, furniture and others.

The list goes on and on. Now it is very difficult to identify any trends in the choice of markets or service sectors that financial institutions are beginning to master.

To increase liquidity and greater customer loyalty, banks try to "be where their potential customer is." And, if you do not win back part of the audience, then at least become an intermediary between the client and the company whose services he needs.