Carding Forum

Professional

Understanding the causes and consequences of the "boom" of ICO investments in the post-Soviet space

The investment market of the post-Soviet space.

2021 has become the year of a new "gold rush". More than 400 projects entered the new capital market from the post-Soviet countries alone.

One of the main reasons for this boom is that entrepreneurs and enterprising engineers have gained access to the global money market. The more global the idea was, the more it found a response among network users who, thanks to ICOs and cryptocurrencies, suddenly became private investors.

Ban or Fail is a principle that has turned heads and frightened institutional and professional investors.

The takeoff was followed by a very rapid decline. But the market did not die, it transformed

A new round is already being formed, professional investors who have adapted their risk assessment algorithms are marching over the ashes of private investments. With capital, they turn the “survival game” into a systemic investment activity.

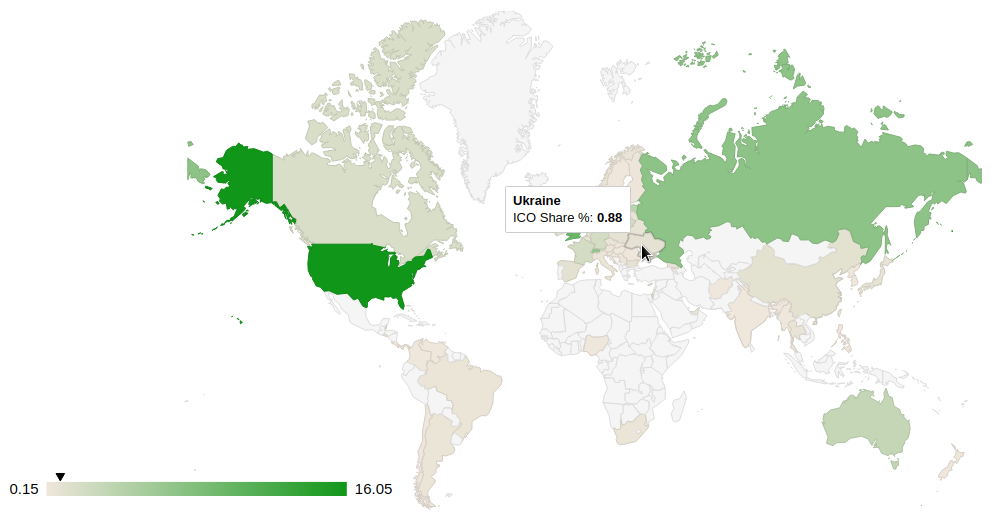

A simple fact that many neglect focusing on globalization is that the countries of the post-Soviet geography are in the leading positions in terms of the volume of ICO investments. As of 10/22/2018, Russia is in fourth place in the world with 7.07% market share. The TOP-25 includes: Estonia (3.98%), Ukraine (0.88%) and Georgia (0.59%).

This means that in a short time in our latitudes a significant segment of the new capital market has formed. It has good potential for raising money from local and foreign projects. The only question is, what are the rules to play?

We divide the global capital market in terms of the “rules of the game”:

Weaknesses become strong

So far, all the crowd-oriented international projects and the latest scammers are running to Asia to try their luck there, stepping on the rake of the difference in mentality and culture.

Projects from post-Soviet countries have their own window of opportunity at home - the cost of raising capital is lower, and the conditions are their own, understandable and in their native language

Multiple analysis of projects allows us to identify 7 significant weaknesses of Slavic projects, which significantly complicate raising money in the global market, but are solved by attracting investments in the local segment:

Weaknesses become strengths.

Types of ICO investors who work in the post-Soviet space

There are about 100 funds operating in the region and about 400 other private investors who invest in ICOs and blockchain projects.

The main types of investors in the post-Soviet market:

Types of ICO investors who work in the post-Soviet space.

The capital market is diverse, which makes it possible for entrepreneurs to look for investors for various tasks and with a wide range of conditions for obtaining capital. In fact, the market is still at the stage of the initial formation of the “rules of the game”.

The investment market of the post-Soviet space.

2021 has become the year of a new "gold rush". More than 400 projects entered the new capital market from the post-Soviet countries alone.

One of the main reasons for this boom is that entrepreneurs and enterprising engineers have gained access to the global money market. The more global the idea was, the more it found a response among network users who, thanks to ICOs and cryptocurrencies, suddenly became private investors.

Ban or Fail is a principle that has turned heads and frightened institutional and professional investors.

The takeoff was followed by a very rapid decline. But the market did not die, it transformed

A new round is already being formed, professional investors who have adapted their risk assessment algorithms are marching over the ashes of private investments. With capital, they turn the “survival game” into a systemic investment activity.

A simple fact that many neglect focusing on globalization is that the countries of the post-Soviet geography are in the leading positions in terms of the volume of ICO investments. As of 10/22/2018, Russia is in fourth place in the world with 7.07% market share. The TOP-25 includes: Estonia (3.98%), Ukraine (0.88%) and Georgia (0.59%).

This means that in a short time in our latitudes a significant segment of the new capital market has formed. It has good potential for raising money from local and foreign projects. The only question is, what are the rules to play?

We divide the global capital market in terms of the “rules of the game”:

- The segment is old money (EU territories, Great Britain and the USA) - capital was formed here several generations ago. These markets have rules, traditions, regulation and an eco-system for servicing capital. Here, stability is valued higher than the number of X's.

- Segment - new money (Asia and post-Soviet countries) - investment money is very young, there is no second generation to manage it. Add to this the formula “at the behest, at my will” and we get markets where the number of potential x's in conjunction with a short time interval of their occurrence is not just dizzy - they are dazzling.

Weaknesses become strong

So far, all the crowd-oriented international projects and the latest scammers are running to Asia to try their luck there, stepping on the rake of the difference in mentality and culture.

Projects from post-Soviet countries have their own window of opportunity at home - the cost of raising capital is lower, and the conditions are their own, understandable and in their native language

Multiple analysis of projects allows us to identify 7 significant weaknesses of Slavic projects, which significantly complicate raising money in the global market, but are solved by attracting investments in the local segment:

Weaknesses become strengths.

- Weak English - a banal lack of knowledge of English - is one of the reasons that the post-Soviet market is relatively poorly integrated into the global one, but at the local level this does not create a problem.

- Engineers are not entrepreneurs - we have enough interesting ideas and technological solutions, but often the project team is engineers without entrepreneurial experience. For the old money world, this is a red flag. In our reality, this is an obvious reality and local investors know how to solve it.

- There is no systemic marketing and strategy - the reason is simple, cryptanarchists were the first to work in the industry. They didn't have the necessary background. They gained skills and experience in the process. The old world requires smooth processes. The new one is ready for the fact that the expertise will be increased already in the process of implementation.

- Lack of legal literacy is a problem that has caused many projects to suffer. They are poor at calculating risks, do not look beyond their own jurisdiction. Many people naively believe that they can find a way out of any situation. What is acceptable in our latitudes is a red flag for investors from the world of clear rules.

- There is no middle ground - projects or work, or just an idea. There is no middle ground yet, although the situation is improving. For our realities, an idea backed by people with great influence is viable. In the US and EU markets, projects without a business plan, MVP or even revenue are no longer considered.

- An investor will help - for projects from our geographies, the search for investments is often accompanied by a search for a mentor who will help. In the realities of the old capital market, investment is the belief that the team will implement the project itself. Institutionals do not participate in the development of the project. In the local market, investors often invest who do not just want to increase their funds, but thus create for themselves the opportunity to use their experience in a new area.

- "Young money" - while in the world of old money they are waiting for explanations from regulators. They are looking for investment opportunities in the segment of young capital. There is a different motivation here, which ensures greater efficiency and lower cost of raising money. They are one of the few who are willing to take risks in the current market.

Types of ICO investors who work in the post-Soviet space

There are about 100 funds operating in the region and about 400 other private investors who invest in ICOs and blockchain projects.

The main types of investors in the post-Soviet market:

Types of ICO investors who work in the post-Soviet space.

- Professional cryptocurrency funds (there are about 10 of them). The willingness of these funds to participate is a signal to the others that they can invest. These funds have already formed a team of analysts and have a strong expertise. All processes are debugged. So far, this is the smallest group. All projects want to receive investments from them.

- Funds that have been created by recent ICO investors (there are up to 20 of them). Their plus is in the experience and understanding of the market. But they have problems in the processes and ecosystem of startup development. Therefore, projects should not count on any special help from them.

- Funds that are formed with the help of ICO or want to carry it out.

Classic venture funds (about 30). They have assessed the prospects of investments in blockchain and are ready to develop this industry. - Oligarchs and businessmen. They see a chance to make money, but they do not have the necessary experience. This type of investor creates their own funds or finances existing ones. Their direction is investment of large sums in HYIP projects (Telegram, EOS, etc.) and spot / rare investments in ordinary ones. Their money will not bring much benefit to ordinary projects. In this case, the lack of expertise and culture of funding startups will affect.

- Private investors- two opposite directions can be distinguished here: experienced new wave entrepreneurs and HYIP entrepreneurs who came to earn money in the popular industry.

- Experienced - this category includes former advisors and part of the crypto group, which raised good money during a growing market. They also include successful IT entrepreneurs who have decided to take a new step in their careers. They have experience, and therefore startups can get more than just investment. But due to the volatility in their activities, skepticism and even a certain fatigue are noticeable.

- Hype - this category includes mid-level entrepreneurs with extensive networking. They are accustomed to adapting to new circumstances and starting to work in industries that can bring money. But there is a problem - this category continues to operate according to the old rules, and also ignores or does not fully understand the latest trends. The fact is that a significant part of them started working in the industry at the end of 2017 or at the beginning of 2018. As a result, HYIP investors did not manage to get enough experience in the growing market.

- Family-offices (number 30-40) - they have been operating on the market since the end of 2017. It is highly likely that in 2019 this category will take a leading position and will be either No. 1 or No. 2 after venture funds.

- Retail investors - there were too few of them even at the peak of the ICO hype (compared to other regions). Now there are only those who are connected with the IT industry and have insights on the project in which they want to invest.

- Toxic money is political and medium-sized businesses. This category is not versed in venture investing, but they know that they can make money this way. As a result, a few months after the investment, these investors demand profit and kill the project. Experienced founders avoid dealing with them. Newbies are trying to quickly solve the financial problems of the project. As a result, the startup is at enormous risk. This category does not help much, but rather hinders the development of the ecosystem.

The capital market is diverse, which makes it possible for entrepreneurs to look for investors for various tasks and with a wide range of conditions for obtaining capital. In fact, the market is still at the stage of the initial formation of the “rules of the game”.