Lord777

Professional

- Messages

- 2,579

- Reaction score

- 1,511

- Points

- 113

The payment card is the most popular payment tool today, although it seems that its age is coming to an end. In 2013, the number of credit card payments in the United States exceeded the number of check payments, and debit cards reached the same level in 2004. The magnetic card is gradually being replaced by chip cards, and all the plastic can go away due to mobile payments such as Apple Pay.

Let's take a look at what people used before credit cards: where they came from, how they took on the modern form, and why this particular font is stamped on them.

One of the earliest ancestors of modern payment cards is the metal tokens that department stores issued to customers in the early twentieth century to keep track of purchases. Sellers made a fingerprint of the token in the accounting books opposite the buyer's name.

You had to pay the bills: if now you are late in paying the loan they start to bother you with calls, then a hundred years ago a collector would have immediately come to you in a horse-drawn cart and would have taken your property.

But it was only about local business, so entrepreneurs tied customers to themselves. On a journey, these steel plates would not be of any use to you, they would not be accepted anywhere. But traveling with a large amount of cash is not the best idea either now or a hundred years ago. This was taken care of in the 1880s by the American Express company. Due to the need to use credit letters to receive money, the president of the company instructed the head of one of the departments to develop an alternative, which became traveler's checks.

This tool is still used today, and travelers ' cheques are issued in euros and dollars. Only the owner can pay for them, and in case of theft or loss, they are restored at the offices of American Express and partners.

In 1920, Texaco began producing cardboard cards for its customers to use at gas stations. It soon became clear that the cardboard for refills is not suitable, it is too easy to get dirty. Therefore, Farrington Manufacturing has released steel embossed cards. They helped automate the payment process — the clerk needed to make a fingerprint of the data. A document that is issued when buying with a bank card is called a slip. The company found the Farrington 7B font to be the most suitable for squeezing out letters. It is still used for stamping plastic cards.

In the 1940s and 1950s, during the "trade boom" in the United States, the cashless payment system began to replace checkbooks. Credit cards were initiated by John S. Biggins, a consumer credit specialist at Flatbush National Bank in Brooklyn, who established the Charge-it system in 1946: customers paid for goods with receipts, the store gave receipts to the bank and paid for goods from customers ' accounts. This chain has not changed, but its speed has increased.

Founded in 1950, Diners Club was the first independent credit card company to start using cards primarily for travel and entertainment purposes. According to legend, it all started with a wallet forgotten at home — the founder of the company in 1949 could not pay for dinner in a restaurant. The goal of the project was to allow visitors to such establishments not to be limited to cash. The club issued cards, acted as guarantors for obligations, paid bills, and members of the club received a statement once a month and had to pay the entire amount to the club in two weeks.

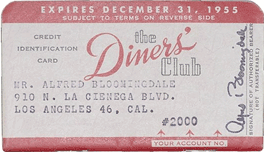

In 1950, the first 200 Diners Club credit cards were issued. They were mostly friends of the company's founder. Cards were accepted in 14 restaurants in New York. The cards were made out of paper, and on the back were addresses and restaurants where they were accepted.

This is what some of the first Diners Club cards looked like:

The cards were made of paper. By the end of 1950, there were already 20,000 cardholders who could pay at 285 restaurants. Since the mid-1950s, the company has entered the international market, on the American Stock Exchange, and in 1981 it was bought by Citibank.

In the USSR, the first credit cards began to operate in 1969, when the stores "Birch" began to accept Diners Club for payment. Since 2004, Diners Club plastic cards from the United States and Canada have received the MasterCard logo, and they can be used to pay at any point where cards of this system are accepted. On July 1, 2008, Discover Financial Services purchased Diners Club International for $ 165 million.

Until 1958, Diners Club had no competitors-they didn't physically exist. Until the BankAmericard cards appeared.

In 1958, Bank of America began its experiment to reduce the costs associated with payments in small businesses. 60 thousand BankAmericard credit cards were sent to residents of Fresno, California. These were ready-to-use cards that didn't require filling out a bank application. Now such carelessness would have ended in disaster, but in the 1950s everything went smoothly.

The card limit was set at $ 500. Translated into today's prices, this is more than 4 thousand dollars. Data didn't go to the bank instantly, no one could follow the loan — in theory, you could buy a huge amount of goods and hide from the police in the woods, with a car, a tent and a supply of food for twenty years.

By 1959, there were more than two million such cards, and twenty thousand entrepreneurs accepted them for payments. These figures will become more revealing if we mention that at that time, when making a purchase, a fingerprint of data from the card was made on the slip receipt. Without convenient terminals, computers, or the Internet. Data embedded on the card helps automation.

Bank of America began to provide its system to other American banks, but not everyone was satisfied with this. Imagine that the Alfa-Bank credit card says Sberbank in large letters — a very strange situation. So I had to invent a new name for the system that wasn't associated with a specific bank.

So the "Visa" mark appeared on the cards, and Bank of America transferred operations with them to National Bank Americard, a company specially created for this purpose. Later it was renamed Visa USA, then Visa International.

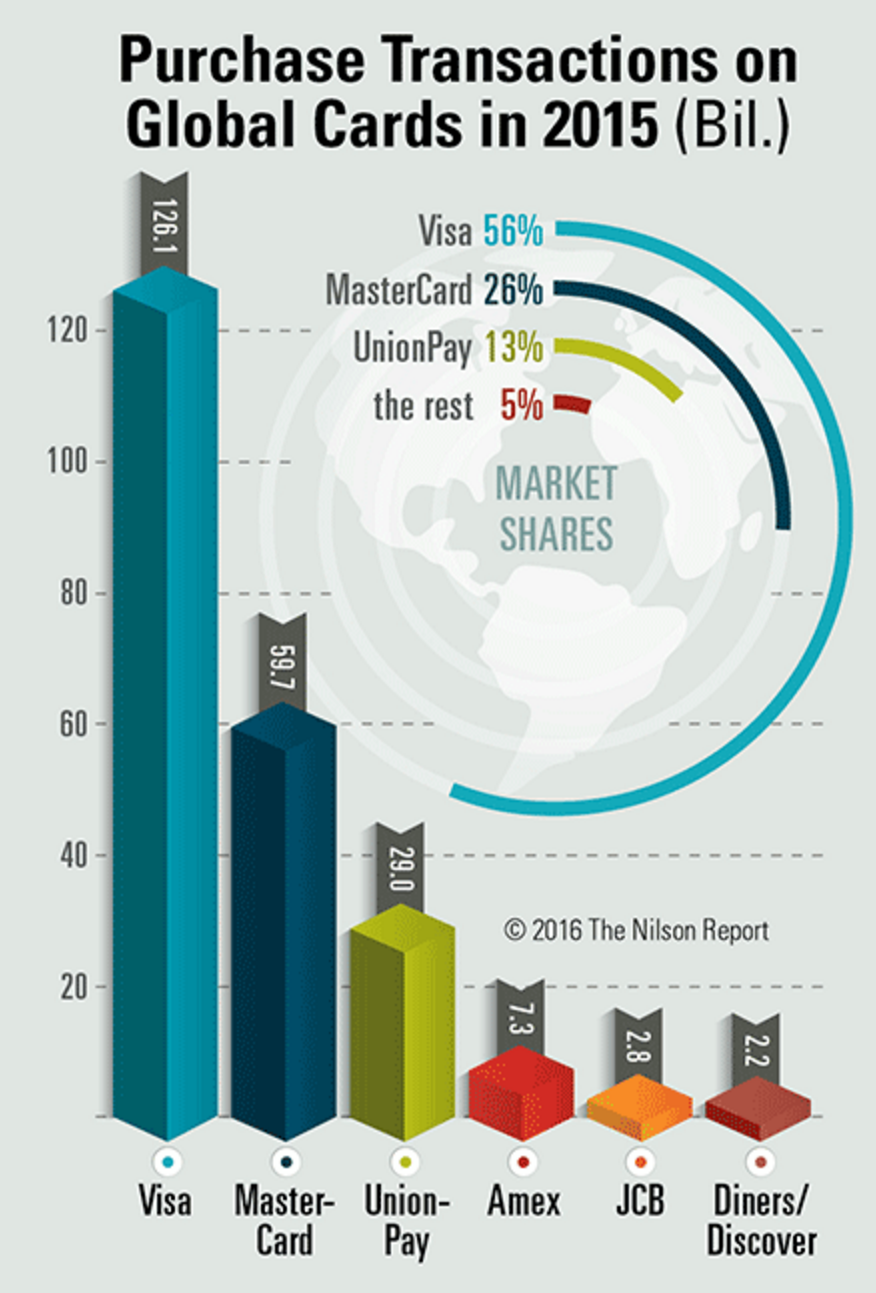

In terms of transaction volume for 2016, the leader of payment systems is Visa with 56%. It is followed by MasterCard with 26%. China's UnionPay takes an honorable third place, with most of its turnover coming from domestic operations.

Infographic: Nilsonreport

The MasterCard system was created as a competitor to BankAmericard and was originally called Interbank. The company was founded in 1966, when several banks agreed to use a single system and formed the Interbank Card Association.

In 1968, MasterCard entered the European market with the help of the European Eurocard system — the agreement provided for mutual acceptance of payments in the two systems.

From its foundation to 1979, the product from the association was called "Master Charge: The Interbank Card", and in 1979 the system acquired its current name — MasterCard. In 1996, the company signed a contract with AT&T to create an operational infrastructure to reduce the time required to process requests. By 1998, there were ATMs accepting MasterCard in Antarctica.

In 2014, MasterCard partnered with Apple to integrate mobile wallet functionality into the iPhone.

The first cards had identification numbers. In the receipts at the establishments where they were accepted, the numbers were entered manually. First, the task was simplified by data embedded on the card, and later by imprinters.

The device made a slip by typing the card number on the form. Such imprinters and standard forms for them are still sold. On Banks.<url> in 2010 discussed whether in addition to the POS-terminal, a manual imprinter is needed that will work when there is no communication or electricity.

The video shows instructions for using the imprinter.

In 1960, the first plastic card with a magnetic stripe was made. IBM had a hand in this. The goal was to develop a way to store data securely — barcodes and perforations are no different in reliability. So we decided to use a magnetic storage medium that was already used to store information in computers.

The photo below shows a prototype of a magnetic stripe card made by IBM. Engineer Forrest Perry tried to glue the strip, but it broke. He told his wife about this, and she suggested that they try to melt the strip into plastic using a regular iron. the impromptu experiment went well.

Now the production of cards with a magnetic stripe is as follows: a plastic base is printed — both sides of the card are covered with two sheets of laminate, the magnetic stripe is fixed on the surface and placed in a thermal press, in which this sandwich is processed at a temperature of 160 degrees.

The first magnetic stripe on the card was on the front side.

The first prototype of a magnetic stripe card

The magnetic layer of a bank card contains three track bars. Previously, the third track stored the PIN code for card operation at ATMs that do not have access to the network. Now only two are used.

The world's first functioning ATM appeared at Barclays in 1967 in North London. But he didn't accept plastic cards, but paper vouchers. You could get no more than 10 pounds at a time. Vending machines with chocolates were already commonplace at that time, and it was they, as well as the bank branch closed at night, that prompted the Scottish inventor John Sheppard-Barron to come up with the idea of automating money receipt.

John Sheppard-Barron received the Order of the British Empire in 2005 for his invention, and a year later the same order was awarded to James Goodfellow as the creator of the PIN code.

The first ATMs for accepting bank cards were installed by Lloyds Bank in the UK in 1972. These machines were developed by IBM. The development of telecommunications made it possible to create entire ATM networks that could be used by several banks. In Russia, the first ATMs appeared in 1991 in the World Trade Center and in the American express office.

In the late seventies, the first payment terminals for magnetic stripe cards appeared in the United States — EFTPOS. Of course, such cards could be accepted in stores before, but only with the help of imprinters.

IBM 3663 cash register

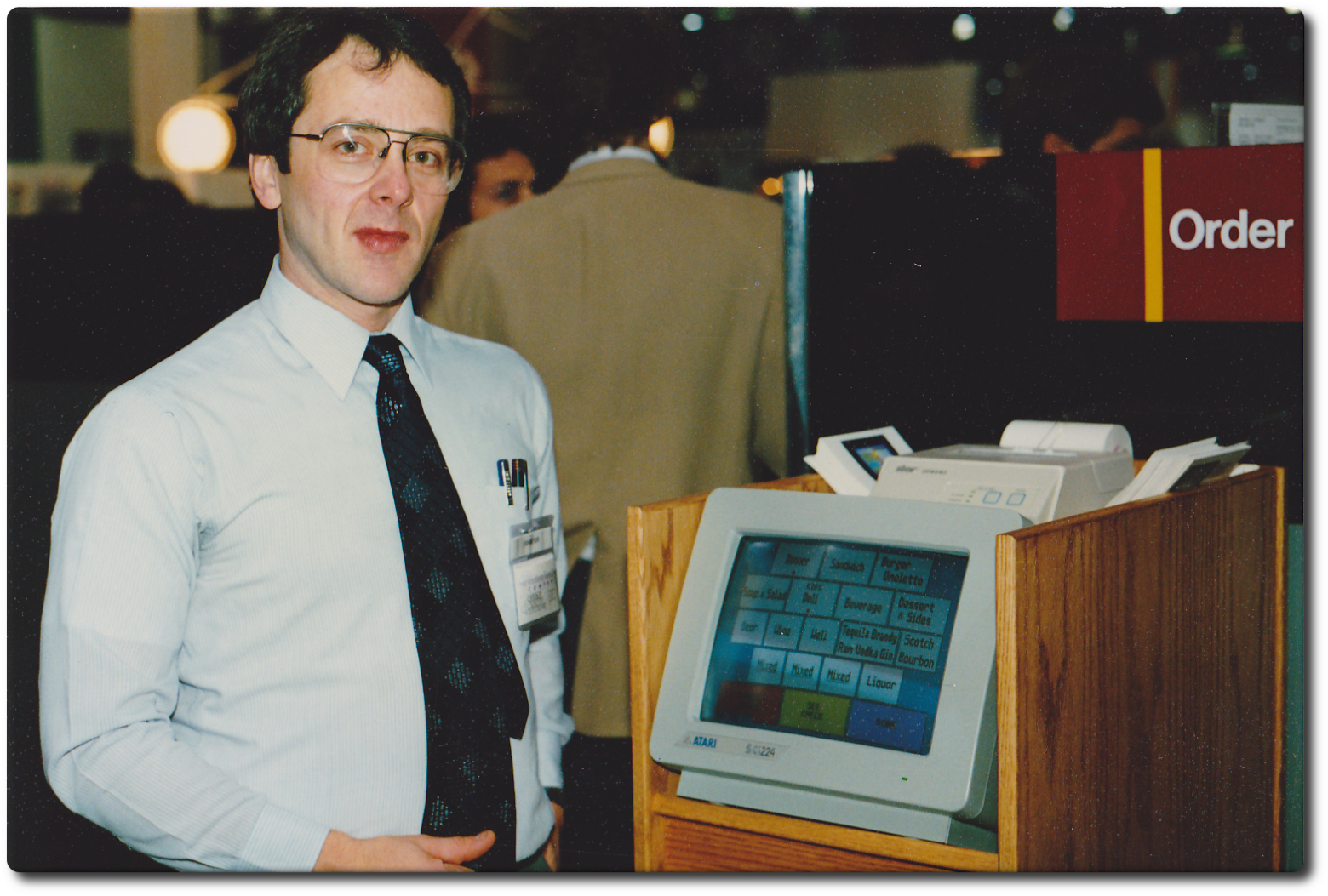

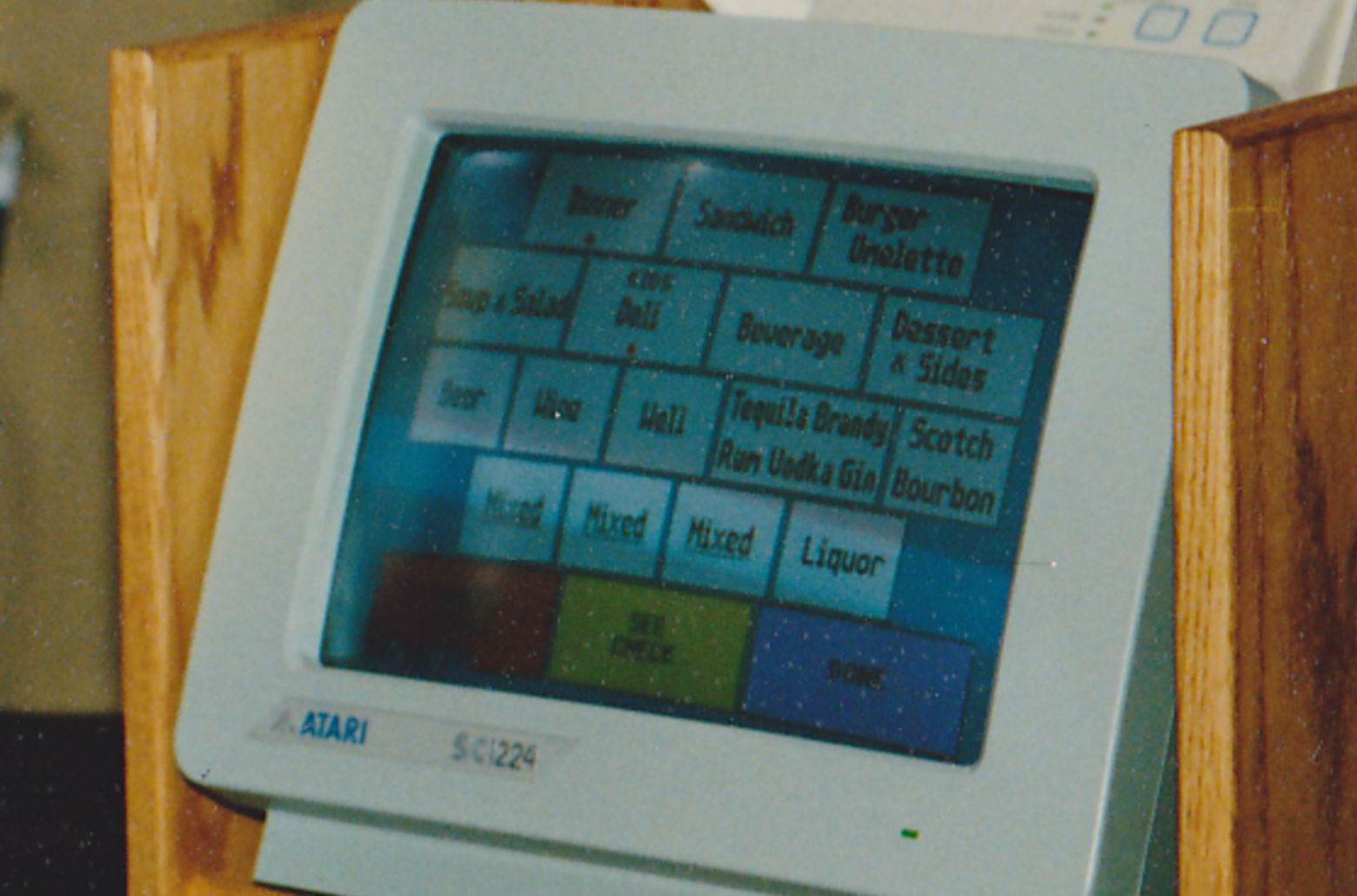

In 1986, a touchscreen was used for the first time in a cash register with support for magnetic stripe cards. It was a ViewTouch-branded POS based on the Atari 520ST 16-bit computer with a 12-inch Atari SC1224 color touch screen. The device was presented by engineer Eugene Mosher at ComDex on November 17, 1986.

The device was first installed in several restaurants in the United States and Canada.

In the early 1990s, Europe began to develop standards for bank smart cards-plastic cards with a built-in chip that closely resembles a SIM card. A patent for the technology was granted in 1982, and in 1983, chip cards for paying phone bills began to be produced in France. These cards are also used in the French healthcare system. And it was in France in 1992 that all debit cards were microchipped. In the 1990s, SIM cards appeared on smart cards-"full-size" SIM cards.

An RFID chip installed inside the card allows you to make contactless payments using PayPass and payWave technologies. Below is a Visa payWave ad for the Russian market.

In 2012, MasterCard introduced a card with a keyboard and an LCD screen. The microcomputer inside the card generates one-time passwords and stores the transaction history in memory, as well as shows the account balance.

This is what a modern card acceptance terminal looks like. Such terminals are connected to the bank via a mobile network and can be powered by batteries, which makes them convenient, for example, for paying in restaurants. Some devices support contactless payment, but they are still a minority — especially in the conservative United States.

Credit card scams started right after they appeared. Savvy Americans realized that having a large credit limit, you can collect goods, sell some of them and go to another state or country.

The next wave was the Internet commerce boom in the mid-1990s. The sites now have “buy”buttons. The attackers used stolen card numbers and well-known names — such as Mickey Mouse, Lex Luther, John Wayne, and Bill Clinton. At that time, the systems did not require checking the payer's name and matching it with the card number, and sellers had to change this.

The presence of ATMs on every corner has led to the spread of another type of fraud: making a copy from the card using a skimmer. The device, sometimes almost invisible, is installed on the slot for receiving a plastic card. The skimmer makes a copy, but in order to fully use it later, you need to find out the pin code. In this case, miniature video cameras aimed at the keyboard come to the rescue. Many people do not cover the keyboard with their hands when typing, and not all ATMs are equipped with a protective panel above it. The photo below shows an example of a skimmer and ATM with a video camera installed by fraudsters (pay attention to the upper-left corner of the ATM), as well as an overlay on the keyboard, which is used instead of a camera to get a PIN code.

Even if you know about skimmers and are able to identify such an overlay, you can not relax. Sometimes they put a lock on the ATM doors that opens with a card — so that you can withdraw money at night when the bank is closed. And they also put skimmers on this device.

Sometimes scammers don't bother installing skimmers on ATMs of other banks. Instead, they set up their own ATMs. In 2015, in Udmurtia, fraudsters bought debited ATMs and placed them around Moscow. They did not give out money, but read information from the magnetic tape of the card and the pin code, after which they reported a "breakdown" and returned the card to the owner.

Skimmers are used not only in ATMs. Technologies have long gone ahead — in three seconds, a fraudster can put such a device on the terminal for paying for purchases with bank cards in a store.

When the fraudster has card details and PIN codes — he can go and spend money. Like the Bulgarian Konstantin Kavrakov, who withdrew money, including from a copy of Bill Gates ' bank card. When the fraudster was arrested in 2015, he was found with several Citi Visa, Standard Chartered MasterCard, Citibank MasterCard, Citi MasterCard, Citibank Visa, East-west Bank Vice credit cards, a blank credit card, checks for transactions and 76 thousand Philippine pesos (about 1,700 US dollars).

You can do without a copy of the cards by getting the original one. This requires the fraudster's personal presence at the ATM. The thief puts the loop in the card reader and waits. The victim receives the money, but cannot withdraw the card. The attacker is called to help to see the PIN code for himself, but nothing works — and he advises to contact the bank. There is a PIN code, it remains to pull out the card in the loop and withdraw all the money.

Many people constantly carry with them several bank cards, loyalty cards, a work pass, a gym membership card — that is, a large amount of plastic. Several projects are trying to save us from this problem by using devices that store data from multiple cards at the same time. In Russia, this is Cardberry. In January 2016, the startup unveiled the card in Las Vegas at CES. The cards are already being used by beta testers in Teremka, Shokoladnitsa, and other establishments. But — in the form of loyalty cards. You can only add bank cards in the plans, so there are security issues here.

A similar project appeared a little earlier in the US — Coin, this card supports NFC. After pre-ordering, this card was waited for two years, but now its status is unclear.

Perhaps LG will enter this market.

The second possible replacement for bank cards is mobile devices. Apple Pay and Android Pay use NFC in mobile gadgets. But while Apple is looking to a future where all payment terminals will be able to accept contactless payments, Samsung is using LoopPay's technology to work with older magnetic stripe-reading terminals.

Plastic cards can also become a thing of the past thanks to biometric identification systems for bank customers. German Gref, the head of Sberbank, hopes to introduce a system of voice recognition and identification by appearance in the next two to three years. But it will work only in Russia, and in other countries-only with Sberbank. In response to this statement, the VTB24 representative said that there are no goals for implementing any technology related to the refusal to use cards.

Mastercard, meanwhile, is testing a payment scheme using selfies.

(c) https://habr.com/ru/articles/394993/

Let's take a look at what people used before credit cards: where they came from, how they took on the modern form, and why this particular font is stamped on them.

One of the earliest ancestors of modern payment cards is the metal tokens that department stores issued to customers in the early twentieth century to keep track of purchases. Sellers made a fingerprint of the token in the accounting books opposite the buyer's name.

You had to pay the bills: if now you are late in paying the loan they start to bother you with calls, then a hundred years ago a collector would have immediately come to you in a horse-drawn cart and would have taken your property.

But it was only about local business, so entrepreneurs tied customers to themselves. On a journey, these steel plates would not be of any use to you, they would not be accepted anywhere. But traveling with a large amount of cash is not the best idea either now or a hundred years ago. This was taken care of in the 1880s by the American Express company. Due to the need to use credit letters to receive money, the president of the company instructed the head of one of the departments to develop an alternative, which became traveler's checks.

This tool is still used today, and travelers ' cheques are issued in euros and dollars. Only the owner can pay for them, and in case of theft or loss, they are restored at the offices of American Express and partners.

In 1920, Texaco began producing cardboard cards for its customers to use at gas stations. It soon became clear that the cardboard for refills is not suitable, it is too easy to get dirty. Therefore, Farrington Manufacturing has released steel embossed cards. They helped automate the payment process — the clerk needed to make a fingerprint of the data. A document that is issued when buying with a bank card is called a slip. The company found the Farrington 7B font to be the most suitable for squeezing out letters. It is still used for stamping plastic cards.

In the 1940s and 1950s, during the "trade boom" in the United States, the cashless payment system began to replace checkbooks. Credit cards were initiated by John S. Biggins, a consumer credit specialist at Flatbush National Bank in Brooklyn, who established the Charge-it system in 1946: customers paid for goods with receipts, the store gave receipts to the bank and paid for goods from customers ' accounts. This chain has not changed, but its speed has increased.

Diners Club

Founded in 1950, Diners Club was the first independent credit card company to start using cards primarily for travel and entertainment purposes. According to legend, it all started with a wallet forgotten at home — the founder of the company in 1949 could not pay for dinner in a restaurant. The goal of the project was to allow visitors to such establishments not to be limited to cash. The club issued cards, acted as guarantors for obligations, paid bills, and members of the club received a statement once a month and had to pay the entire amount to the club in two weeks.

In 1950, the first 200 Diners Club credit cards were issued. They were mostly friends of the company's founder. Cards were accepted in 14 restaurants in New York. The cards were made out of paper, and on the back were addresses and restaurants where they were accepted.

This is what some of the first Diners Club cards looked like:

The cards were made of paper. By the end of 1950, there were already 20,000 cardholders who could pay at 285 restaurants. Since the mid-1950s, the company has entered the international market, on the American Stock Exchange, and in 1981 it was bought by Citibank.

In the USSR, the first credit cards began to operate in 1969, when the stores "Birch" began to accept Diners Club for payment. Since 2004, Diners Club plastic cards from the United States and Canada have received the MasterCard logo, and they can be used to pay at any point where cards of this system are accepted. On July 1, 2008, Discover Financial Services purchased Diners Club International for $ 165 million.

Until 1958, Diners Club had no competitors-they didn't physically exist. Until the BankAmericard cards appeared.

Visa

In 1958, Bank of America began its experiment to reduce the costs associated with payments in small businesses. 60 thousand BankAmericard credit cards were sent to residents of Fresno, California. These were ready-to-use cards that didn't require filling out a bank application. Now such carelessness would have ended in disaster, but in the 1950s everything went smoothly.

The card limit was set at $ 500. Translated into today's prices, this is more than 4 thousand dollars. Data didn't go to the bank instantly, no one could follow the loan — in theory, you could buy a huge amount of goods and hide from the police in the woods, with a car, a tent and a supply of food for twenty years.

By 1959, there were more than two million such cards, and twenty thousand entrepreneurs accepted them for payments. These figures will become more revealing if we mention that at that time, when making a purchase, a fingerprint of data from the card was made on the slip receipt. Without convenient terminals, computers, or the Internet. Data embedded on the card helps automation.

Bank of America began to provide its system to other American banks, but not everyone was satisfied with this. Imagine that the Alfa-Bank credit card says Sberbank in large letters — a very strange situation. So I had to invent a new name for the system that wasn't associated with a specific bank.

So the "Visa" mark appeared on the cards, and Bank of America transferred operations with them to National Bank Americard, a company specially created for this purpose. Later it was renamed Visa USA, then Visa International.

In terms of transaction volume for 2016, the leader of payment systems is Visa with 56%. It is followed by MasterCard with 26%. China's UnionPay takes an honorable third place, with most of its turnover coming from domestic operations.

Infographic: Nilsonreport

MasterCard

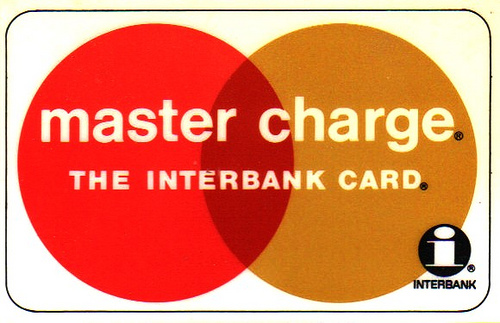

The MasterCard system was created as a competitor to BankAmericard and was originally called Interbank. The company was founded in 1966, when several banks agreed to use a single system and formed the Interbank Card Association.

In 1968, MasterCard entered the European market with the help of the European Eurocard system — the agreement provided for mutual acceptance of payments in the two systems.

From its foundation to 1979, the product from the association was called "Master Charge: The Interbank Card", and in 1979 the system acquired its current name — MasterCard. In 1996, the company signed a contract with AT&T to create an operational infrastructure to reduce the time required to process requests. By 1998, there were ATMs accepting MasterCard in Antarctica.

In 2014, MasterCard partnered with Apple to integrate mobile wallet functionality into the iPhone.

How cards are accepted

The first cards had identification numbers. In the receipts at the establishments where they were accepted, the numbers were entered manually. First, the task was simplified by data embedded on the card, and later by imprinters.

The device made a slip by typing the card number on the form. Such imprinters and standard forms for them are still sold. On Banks.<url> in 2010 discussed whether in addition to the POS-terminal, a manual imprinter is needed that will work when there is no communication or electricity.

The video shows instructions for using the imprinter.

In 1960, the first plastic card with a magnetic stripe was made. IBM had a hand in this. The goal was to develop a way to store data securely — barcodes and perforations are no different in reliability. So we decided to use a magnetic storage medium that was already used to store information in computers.

The photo below shows a prototype of a magnetic stripe card made by IBM. Engineer Forrest Perry tried to glue the strip, but it broke. He told his wife about this, and she suggested that they try to melt the strip into plastic using a regular iron. the impromptu experiment went well.

Now the production of cards with a magnetic stripe is as follows: a plastic base is printed — both sides of the card are covered with two sheets of laminate, the magnetic stripe is fixed on the surface and placed in a thermal press, in which this sandwich is processed at a temperature of 160 degrees.

The first magnetic stripe on the card was on the front side.

The first prototype of a magnetic stripe card

The magnetic layer of a bank card contains three track bars. Previously, the third track stored the PIN code for card operation at ATMs that do not have access to the network. Now only two are used.

The world's first functioning ATM appeared at Barclays in 1967 in North London. But he didn't accept plastic cards, but paper vouchers. You could get no more than 10 pounds at a time. Vending machines with chocolates were already commonplace at that time, and it was they, as well as the bank branch closed at night, that prompted the Scottish inventor John Sheppard-Barron to come up with the idea of automating money receipt.

John Sheppard-Barron received the Order of the British Empire in 2005 for his invention, and a year later the same order was awarded to James Goodfellow as the creator of the PIN code.

The first ATMs for accepting bank cards were installed by Lloyds Bank in the UK in 1972. These machines were developed by IBM. The development of telecommunications made it possible to create entire ATM networks that could be used by several banks. In Russia, the first ATMs appeared in 1991 in the World Trade Center and in the American express office.

In the late seventies, the first payment terminals for magnetic stripe cards appeared in the United States — EFTPOS. Of course, such cards could be accepted in stores before, but only with the help of imprinters.

IBM 3663 cash register

In 1986, a touchscreen was used for the first time in a cash register with support for magnetic stripe cards. It was a ViewTouch-branded POS based on the Atari 520ST 16-bit computer with a 12-inch Atari SC1224 color touch screen. The device was presented by engineer Eugene Mosher at ComDex on November 17, 1986.

The device was first installed in several restaurants in the United States and Canada.

In the early 1990s, Europe began to develop standards for bank smart cards-plastic cards with a built-in chip that closely resembles a SIM card. A patent for the technology was granted in 1982, and in 1983, chip cards for paying phone bills began to be produced in France. These cards are also used in the French healthcare system. And it was in France in 1992 that all debit cards were microchipped. In the 1990s, SIM cards appeared on smart cards-"full-size" SIM cards.

An RFID chip installed inside the card allows you to make contactless payments using PayPass and payWave technologies. Below is a Visa payWave ad for the Russian market.

In 2012, MasterCard introduced a card with a keyboard and an LCD screen. The microcomputer inside the card generates one-time passwords and stores the transaction history in memory, as well as shows the account balance.

This is what a modern card acceptance terminal looks like. Such terminals are connected to the bank via a mobile network and can be powered by batteries, which makes them convenient, for example, for paying in restaurants. Some devices support contactless payment, but they are still a minority — especially in the conservative United States.

Fraud

Credit card scams started right after they appeared. Savvy Americans realized that having a large credit limit, you can collect goods, sell some of them and go to another state or country.

The next wave was the Internet commerce boom in the mid-1990s. The sites now have “buy”buttons. The attackers used stolen card numbers and well-known names — such as Mickey Mouse, Lex Luther, John Wayne, and Bill Clinton. At that time, the systems did not require checking the payer's name and matching it with the card number, and sellers had to change this.

The presence of ATMs on every corner has led to the spread of another type of fraud: making a copy from the card using a skimmer. The device, sometimes almost invisible, is installed on the slot for receiving a plastic card. The skimmer makes a copy, but in order to fully use it later, you need to find out the pin code. In this case, miniature video cameras aimed at the keyboard come to the rescue. Many people do not cover the keyboard with their hands when typing, and not all ATMs are equipped with a protective panel above it. The photo below shows an example of a skimmer and ATM with a video camera installed by fraudsters (pay attention to the upper-left corner of the ATM), as well as an overlay on the keyboard, which is used instead of a camera to get a PIN code.

Even if you know about skimmers and are able to identify such an overlay, you can not relax. Sometimes they put a lock on the ATM doors that opens with a card — so that you can withdraw money at night when the bank is closed. And they also put skimmers on this device.

Sometimes scammers don't bother installing skimmers on ATMs of other banks. Instead, they set up their own ATMs. In 2015, in Udmurtia, fraudsters bought debited ATMs and placed them around Moscow. They did not give out money, but read information from the magnetic tape of the card and the pin code, after which they reported a "breakdown" and returned the card to the owner.

Skimmers are used not only in ATMs. Technologies have long gone ahead — in three seconds, a fraudster can put such a device on the terminal for paying for purchases with bank cards in a store.

When the fraudster has card details and PIN codes — he can go and spend money. Like the Bulgarian Konstantin Kavrakov, who withdrew money, including from a copy of Bill Gates ' bank card. When the fraudster was arrested in 2015, he was found with several Citi Visa, Standard Chartered MasterCard, Citibank MasterCard, Citi MasterCard, Citibank Visa, East-west Bank Vice credit cards, a blank credit card, checks for transactions and 76 thousand Philippine pesos (about 1,700 US dollars).

You can do without a copy of the cards by getting the original one. This requires the fraudster's personal presence at the ATM. The thief puts the loop in the card reader and waits. The victim receives the money, but cannot withdraw the card. The attacker is called to help to see the PIN code for himself, but nothing works — and he advises to contact the bank. There is a PIN code, it remains to pull out the card in the loop and withdraw all the money.

Replacing cards

Many people constantly carry with them several bank cards, loyalty cards, a work pass, a gym membership card — that is, a large amount of plastic. Several projects are trying to save us from this problem by using devices that store data from multiple cards at the same time. In Russia, this is Cardberry. In January 2016, the startup unveiled the card in Las Vegas at CES. The cards are already being used by beta testers in Teremka, Shokoladnitsa, and other establishments. But — in the form of loyalty cards. You can only add bank cards in the plans, so there are security issues here.

A similar project appeared a little earlier in the US — Coin, this card supports NFC. After pre-ordering, this card was waited for two years, but now its status is unclear.

Perhaps LG will enter this market.

The second possible replacement for bank cards is mobile devices. Apple Pay and Android Pay use NFC in mobile gadgets. But while Apple is looking to a future where all payment terminals will be able to accept contactless payments, Samsung is using LoopPay's technology to work with older magnetic stripe-reading terminals.

Plastic cards can also become a thing of the past thanks to biometric identification systems for bank customers. German Gref, the head of Sberbank, hopes to introduce a system of voice recognition and identification by appearance in the next two to three years. But it will work only in Russia, and in other countries-only with Sberbank. In response to this statement, the VTB24 representative said that there are no goals for implementing any technology related to the refusal to use cards.

Mastercard, meanwhile, is testing a payment scheme using selfies.

(c) https://habr.com/ru/articles/394993/