Papa Carder

Professional

- Messages

- 258

- Reaction score

- 247

- Points

- 43

Imagine an invisible web stretching across the globe: from the dark corners of Russia's dark web to servers in China and street hackers in Nigeria. This is global carding — a multi-billion-dollar credit card fraud industry where your card details are bought, sold, and used to steal. In 2026, with AI making attacks smarter and faster, carding will evolve into a truly global threat. But what exactly is it? Why is it thriving? And how does it affect us all? Let's dive into this exciting yet dangerous world, drawing on the latest data and trends. We'll explore how carders operate globally, which countries are leading the way, and what lies ahead.

The global aspect? Carding knows no borders. Data is stolen in the US, sold in Russia, used in Europe, and the goods are sent to drop addresses (intermediate points) around the world. As of 2026, this is part of a broader cyber fraud, where AI generates fake identities and automates attacks. For example, synthetic identities (fake profiles created from real data) have become a top trend: they allow people to open accounts and take out loans without raising suspicion.

In 2026, carding gained momentum thanks to "fraud-as-a-service" — darknet services where newcomers rent attack tools, like Uber for hackers. This makes it easier to enter the "business": you can buy a ready-made carding kit for $10-50.

Global damage from cybercrime, including carding, exceeds $10 trillion annually. In 2026, the focus is on AI: fraudsters use generative models to create convincing phishing emails or fake voices for "phantom hacker scams" – scams where victims are convinced to transfer money. It's not just the elderly who are at risk: young people (20-29 years old) lose money 44% of the time.

Key stats table for 2026:

Africa: Nigeria (21.28) is a hub for "Nigerian princes" and mule networks (where people launder money for a commission). Asia: China and India are hubs for data theft through hacking. Europe: Romania (14.83) and Ukraine are sources of carding botnets.

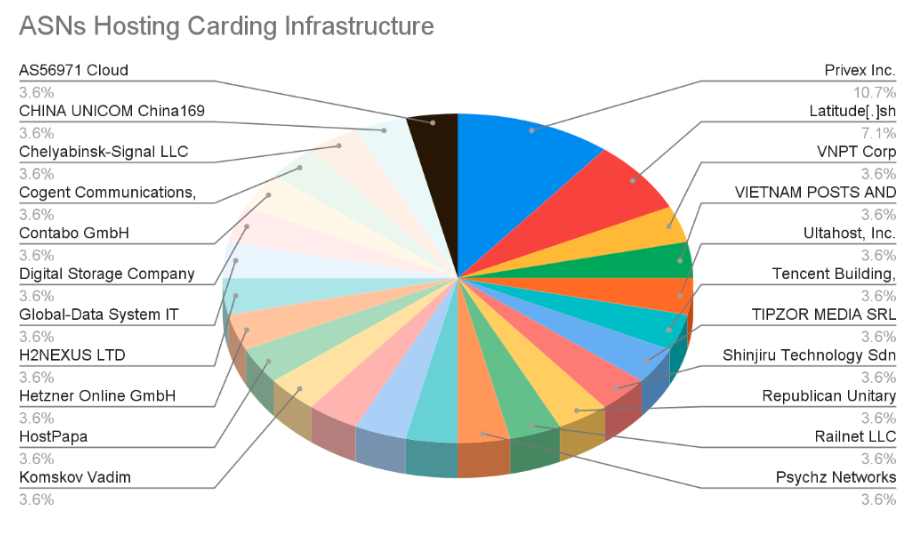

Infrastructure: Carding servers are often located in China (AS56971 Cloud, 3.6%), Vietnam (VNPT Corp, 3.6%), or Latvia (Privex Inc., 10.7%). Fraudsters use VPNs and proxies to disguise themselves.

Banks are responding with tokenization (replacing card numbers with tokens), continuous verification, and AI monitoring. The online fraud protection market will grow to $14.72 billion by 2025, with a compound annual growth rate (CAGR) in the coming years.

Tips: Use 2FA, monitor transactions, and avoid suspicious links. Banks: implement AI orchestration for detection.

Ultimately, global carding is a technological war. While fraudsters evolve, the world is learning to defend itself. But remember: the best defense is awareness. If you notice anything suspicious, report it to your bank or the police. The world is digital, but security is in our hands!

What is carding: From data theft to "carding" into stores

Carding isn't just stealing a credit card from a wallet. It's an entire ecosystem: hackers break into bank or store databases, stealing millions of card numbers, CVV codes, and personal data. These "dumps" are then sold on underground forums like Joker's Stash or in Telegram channels. Buyers — carders — enter this data into online stores, buying gadgets, clothing, or even cryptocurrency, which they then launder.The global aspect? Carding knows no borders. Data is stolen in the US, sold in Russia, used in Europe, and the goods are sent to drop addresses (intermediate points) around the world. As of 2026, this is part of a broader cyber fraud, where AI generates fake identities and automates attacks. For example, synthetic identities (fake profiles created from real data) have become a top trend: they allow people to open accounts and take out loans without raising suspicion.

In 2026, carding gained momentum thanks to "fraud-as-a-service" — darknet services where newcomers rent attack tools, like Uber for hackers. This makes it easier to enter the "business": you can buy a ready-made carding kit for $10-50.

Global Statistics: Billions in Losses and 25% Growth

The numbers are staggering: in 2024, global fraud losses reached $12.5 billion in the US alone, a 25% increase. By 2026, this has evolved: Alloy reports that 67% of companies have seen an increase in attacks thanks to AI, which scales fraud. Globally, the Nilson Report estimates that credit card losses will exceed $165 billion in the US by the end of the decade.Global damage from cybercrime, including carding, exceeds $10 trillion annually. In 2026, the focus is on AI: fraudsters use generative models to create convincing phishing emails or fake voices for "phantom hacker scams" – scams where victims are convinced to transfer money. It's not just the elderly who are at risk: young people (20-29 years old) lose money 44% of the time.

Key stats table for 2026:

| Aspect | Data | Source |

|---|---|---|

| Increase in attacks | 67% of companies noted an increase | Alloy Report |

| Losses in the US (2024) | $12.5 billion | FTC |

| Global check-fraud | $21 billion (80% in America) | Veraphine |

| Synthetic identities | 98% of fraud leaders are concerned | TransUnion |

The Geography of Carding: Where the "Kings" of Fraud Hide

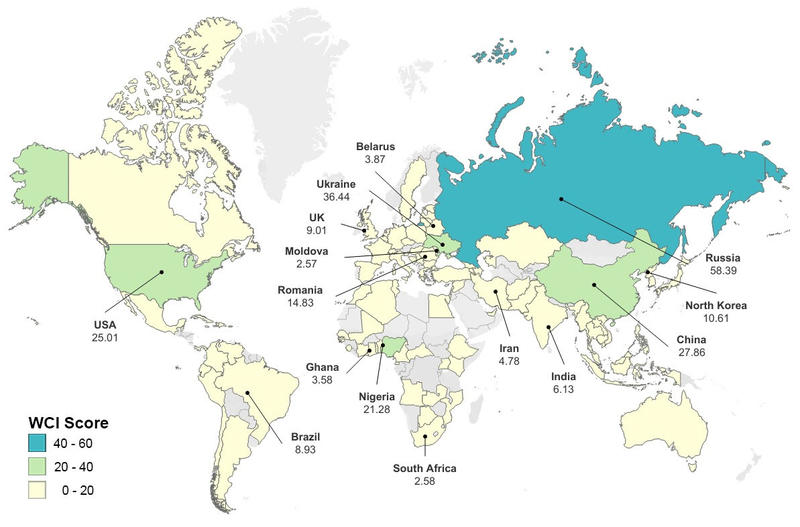

Carding is global, but there are hot spots. According to the Oxford Cybercrime Index, Russia leads with a high score (58.39), followed by China (27.86), Ukraine (36.44), and the US (25.01). This doesn't mean all Russians are hackers, but they have strong networks: forums like Exploit.in and groups like Conti.Africa: Nigeria (21.28) is a hub for "Nigerian princes" and mule networks (where people launder money for a commission). Asia: China and India are hubs for data theft through hacking. Europe: Romania (14.83) and Ukraine are sources of carding botnets.

Infrastructure: Carding servers are often located in China (AS56971 Cloud, 3.6%), Vietnam (VNPT Corp, 3.6%), or Latvia (Privex Inc., 10.7%). Fraudsters use VPNs and proxies to disguise themselves.

Trends 2026: AI, Bots, and New Schemes

In 2026, carding mutates:- AI-boosting: Fraudsters use GenAI for automation: bots "punch" cards by the thousands, mimicking human actions.

- Mule activity: The rise of "mules" — people who transfer stolen goods for a fee. This trend spiked in 2025, and continues.

- Authorized Push Payment (APP) scam: The victim is tricked into transferring money themselves, often through BEC (Business Email Compromise).

- Agentic commerce bots: AI agents make purchases on behalf of users, but fraudsters imitate them.

- Fraud cycles: Seasonal peaks - tax season (account takeover), holidays (carding in stores).

Banks are responding with tokenization (replacing card numbers with tokens), continuous verification, and AI monitoring. The online fraud protection market will grow to $14.72 billion by 2025, with a compound annual growth rate (CAGR) in the coming years.

Consequences and how to protect yourself

Global carding is affecting everyone: prices are rising, insurance costs are increasing, and economies are losing billions. For businesses, it's a loss of trust, and for people, it's the stress of theft.Tips: Use 2FA, monitor transactions, and avoid suspicious links. Banks: implement AI orchestration for detection.

Ultimately, global carding is a technological war. While fraudsters evolve, the world is learning to defend itself. But remember: the best defense is awareness. If you notice anything suspicious, report it to your bank or the police. The world is digital, but security is in our hands!