Everything has been said for a long time, but since no one is listening, you have to constantly go back and repeat everything again. Andre Gide

POS terminal no longer needed or commoditization

What is a POS terminal? It is a compact and secure hardware solution specially designed to accept payments in trade using cards of international payment systems. It solves a variety of tasks including simplifying and standardizing the purchase process, allowing you to get rid of cash and enabling instant verification of the customer's solvency. It sounds solid, there is only one thing but-this technology appeared in 1983, almost 40 years ago!

A complex economy is built around the POS terminal, which involves device manufacturers and software vendors, as well as banks, payment systems and laboratories that check and certify EMVCo L1, L2 and L3 terminals, PCI DSS. The terminal needs to be designed and manufactured in China, certified in laboratories, introduced into the country and cleared, sold, maintained and managed by the life cycle. And all this costs money, which is ultimately reflected in the tariff line for retail businesses on the part of banks and payment systems, which play on the principle-we took our interest, and you spin as you want.

The process of washing out POS terminals from the top of technological progress took place in waves and now we are probably seeing the terminal stage. The stage has passed when Chinese and Korean manufacturers destroyed the monopoly of Ingenico and Verifone on the production of POS devices and the exclusive supply of software. Then, for several years, small mPOS machines showed that the cost of the device can be ten times less. True, we stumbled over the PIN. And finally, due to the directives of payment systems, the issue of cards without an NFC chip will stop by 2021. The concept of SoftPOS-a way to accept payments without using a POS terminal at all-is just the final chord. Today, it is technically possible to accept payments using custom mobile devices — via NFC and QR.

SoftPOS from the site softpos.su

What should happen next? After the PCI SSC (Security Standards Council) releases the new CPoC (Contactless Payments on commercial off-the-shelf) standard, which regulates the use of PIN-code on the mobile phone screen, more and more retail enterprises will rush towards a software solution that will be a symbiosis of the classic acquiring of contactless cards and smartphones and the national and international standard of payment. corporate QR code. The pressure of central banks and the rate war will continue — the issue of acquiring profitability and cost reduction will be more relevant than ever.

However, this is not the end of the process. Acquiring is no longer a service that banks exclusively provide to merchants. Access to payment acceptance and processing is becoming more and more similar to access to water and electricity. There is no more “magic " in this service, which means that it can be controlled and provided by the state. It is more convenient for the state when there are uniform rules of the game: all POS acquiring converges in one national switch, and all market participants follow national standards for software design, security, and functionality. Exactly what MADA (Saudi Payments Network) does in its home market. There is every reason to assume that this will remain a strong trend in all markets where central banks are actively managing payments within the country.

Of course, at the end point, it seems that several major players in the local market will directly accept payments. These will be local large systemically important commercial banks, states, and several multinational players (Google, Apple, and Amazon). They will provide their applications as a service, which will include NFC payments, various QR codes, biometrics, and whatever else they come up with at this point.

POS terminals and classic acquiring will not disappear tomorrow. The payment industry is extremely conservative and new payment methods, with all their convenience and variety, will be introduced for decades. Many countries are just launching contactless projects, QR is actively used only in Asia, where there is a strong growth in sales of POS machines. But the direction of movement is not in doubt and the sale of Ineginco Worldline at the price of Plaid is a vivid example of this.

Cards no longer needed or biometrics

With physical plastic, the situation is no less dramatic. It just so happens that plastic is no longer needed. This specter is based on the so-called ingrained “card experience”, people's conservatism, inertia and uneven development of countries. But Henry Ford has been producing cars in his factories for 10 years, Elon Musk launched his Tesla into space — progress is inexorable and nothing can save the horses. You can see the desperate attempts of individual participants in the payment market to find, in fact, some new use for the disappeared artifact. Which doesn't exist.

The plastic card was too late. For example, VISA is already 62 years old, and the first card was issued by Long Island Bank back in 1951, when Stalin was still alive! The map has certainly gone through a major technological evolution over the years. After the magnetic stripe, Chip&PIN appeared, which, by the way, was not implemented very quickly in the world. And then it was time for contactless cards.

Бесконтактную карту можно просто приложить к терминалу, для совершения оплаты. Цифры на ней теперь нужна разве что для e-commerce, а магнитную полосу продолжают делать из уважения к истории (ради поддержки fallbacks?).

However, the contactless card reached its peak in the late iPhone era. Suddenly it turned out that everyone has a fancy smartphone in their pocket, but not everyone has a bank account. Inclusivity. New word. This was most quickly understood in China, which was very late in the development of the fintech sector from Western countries, but, accordingly, did not have the legacy technologies of the past on its balance sheet. AliPay and WeChat.Pay has completely captured the payment market, making the traditional UnionPay payment system just an addition. Why do I need a bank card if it's convenient to pay without it?

First mobile - first card from BBVA Bank with dynamic CVV from the website nfcw.com

But the Chinese experience is not for everyone. In many countries, the payment card based on the VISA and Mastercard infrastructure has become so entrenched that the victory of QR wallets is still not obvious, even despite numerous pilot projects and the penetration of Asian giants. In the same Switzerland, for example, there are no problems with opening a bank account for a huge population from the rural hinterland in the understanding of India and China. But still, it is convenient to pay by phone, and the answer of VISA and Mastercard is tokenization-MDES and VTS services that allow you to issue an existing card as a” token " inside your smartphone. It is fast, cheap and convenient for the buyer. You don't need a real card anymore — you can pay with a bracelet, ring, or watch. Spanish bank BBVA has already launched exclusively digital card products in the spirit of the digital first concept.

A little less obvious is that it also makes no sense to show her photo on the phone screen — it's just a curtsy to a bygone era, a symbol of continuity and nothing more. There is no card, no chip on the card and, accordingly, there is no need to enter a PIN code anymore — smartphone manufacturers Samsung and Apple will be able to authenticate you by fingerprint or head shape.

The card disappeared, shrinking to a QR square or digital token inside keychains and watches. And this has very serious consequences. For example, e-commerce has traditionally been built around entering card details in a payment form. But if there is no card anymore, then what should I enter and where? The simplest answer is that you don't need to enter anything other than a one-time password in the best traditions of SCA (strong customer authentication). Your payment details are already stored in Apple's systems.Pay, Google.Pay or Sber. Pay and almost everything is done to ensure that the purchase takes place in one touch. This is convenient.

Map makers, in a desperate attempt to save something that no longer exists, are introducing a whole series of innovations — a map with a built-in fingerprint, a vertical map, a map without a number, and an environmental map made from recyclable materials. The idea is to increase the customer's enjoyment of using the card. To make it pleasant to hold it in your hands. Stylish, expensive and technologically advanced. But in fact, it still tastes “retro", and there is nothing more eco-friendly than a QR code or token. These are all small niche solutions that will not radically change the picture and reverse the trend towards the destruction of plastic.

What will happen next? Now to pay Apple.Pay just needs to show your face to the camera of your smartphone. The development of this idea is authentication on the part of the merchant. This is exactly what has been done in China for several years. National biometric databases, roaming between regions, and biometric authentication on the merchant's side are logical, convenient, and cheap for all participants in the process.

Banks are no longer needed or Embedded Finance

Commoditization of payment processing, interference of central banks in payment services directly, identical product lines and, as a result, intense competition, rapid growth of fintech companies and, of course, open banking under the flags of PSD2-like directives. It would seem that it could not be worse, but then there is a knock from below — technology companies have arrived. Samsung, Google, Huawei, Amazon, Apple, Uber and countless smaller organizations began to actively enter the financial services market, not wanting to allow other companies to access their users and, moreover, pay a significant percentage for service.

Today, it is absolutely unclear how the service of banks will be better than the same service provided by a large supermarket chain that has received a banking license. Why would their mobile app be worse? If it turns out that the only difference is only in historically serious barriers to entry to the market, then we are waiting for serious changes. No one likes intermediates that take more money than they add value to the value chain.

It doesn't look like the “supermarkets” will replace the banks completely. They will take their significant share, but their advantage will also be the same limitation-a loyal audience. In addition, people tend to choose simpler solutions — twenty different tokens and wallets in a mobile device-clearly not about this.

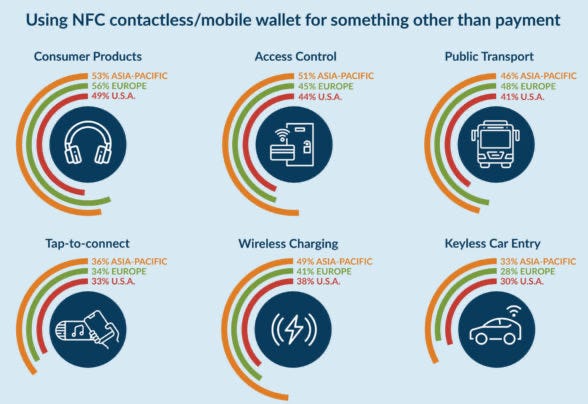

Using NFC from the site nfcw.com

You can also observe the ongoing merger of the payment world and the usual everyday infrastructure. It is already difficult to find a vending machine where the POS terminal is not built in, or at least not stuck on the outside. In urban transport systems, a new project starts almost every day, which allows you to use tokenized cards (mobile phone) for payment, applying them to conventional mounted terminals. Urban transport, such as bicycles or electric scooters, is available with the possibility of contactless payment by card, at least via QR.

In the post-PSD2 world, there are a relatively small number of banks that deal only with service functions for managing user accounts, while all other operations are performed either by the state or by a swarm of fintech organizations that collide on marketplaces and compete under standardized conditions. People will choose between product ecosystems or mobile banking interfaces. It is possible that large companies will make banking services just part of a wider subscription — 10% discount on taxi and here you will also get preferential terms for financial management. The focus will be on functionality and convenience for the end user. Initiatives like managing your personal finances from Excel will become the norm.

Embedded-finance is an opportunity to conveniently and quickly part with money at any time and in any place. A concept that can be called “pay and live". There is no longer any need for POS terminals or physical plastic — everything has been converted to digital form. In essence, we are a step away from the payment method from the TV series Altered Carbon, where the main character simply spat on the sensor.

(c) https://andreifrolov.medium.com/эволюция-платежных-технологий-20-хх-a5c56579055e

POS terminal no longer needed or commoditization

What is a POS terminal? It is a compact and secure hardware solution specially designed to accept payments in trade using cards of international payment systems. It solves a variety of tasks including simplifying and standardizing the purchase process, allowing you to get rid of cash and enabling instant verification of the customer's solvency. It sounds solid, there is only one thing but-this technology appeared in 1983, almost 40 years ago!

A complex economy is built around the POS terminal, which involves device manufacturers and software vendors, as well as banks, payment systems and laboratories that check and certify EMVCo L1, L2 and L3 terminals, PCI DSS. The terminal needs to be designed and manufactured in China, certified in laboratories, introduced into the country and cleared, sold, maintained and managed by the life cycle. And all this costs money, which is ultimately reflected in the tariff line for retail businesses on the part of banks and payment systems, which play on the principle-we took our interest, and you spin as you want.

The process of washing out POS terminals from the top of technological progress took place in waves and now we are probably seeing the terminal stage. The stage has passed when Chinese and Korean manufacturers destroyed the monopoly of Ingenico and Verifone on the production of POS devices and the exclusive supply of software. Then, for several years, small mPOS machines showed that the cost of the device can be ten times less. True, we stumbled over the PIN. And finally, due to the directives of payment systems, the issue of cards without an NFC chip will stop by 2021. The concept of SoftPOS-a way to accept payments without using a POS terminal at all-is just the final chord. Today, it is technically possible to accept payments using custom mobile devices — via NFC and QR.

SoftPOS from the site softpos.su

What should happen next? After the PCI SSC (Security Standards Council) releases the new CPoC (Contactless Payments on commercial off-the-shelf) standard, which regulates the use of PIN-code on the mobile phone screen, more and more retail enterprises will rush towards a software solution that will be a symbiosis of the classic acquiring of contactless cards and smartphones and the national and international standard of payment. corporate QR code. The pressure of central banks and the rate war will continue — the issue of acquiring profitability and cost reduction will be more relevant than ever.

However, this is not the end of the process. Acquiring is no longer a service that banks exclusively provide to merchants. Access to payment acceptance and processing is becoming more and more similar to access to water and electricity. There is no more “magic " in this service, which means that it can be controlled and provided by the state. It is more convenient for the state when there are uniform rules of the game: all POS acquiring converges in one national switch, and all market participants follow national standards for software design, security, and functionality. Exactly what MADA (Saudi Payments Network) does in its home market. There is every reason to assume that this will remain a strong trend in all markets where central banks are actively managing payments within the country.

Of course, at the end point, it seems that several major players in the local market will directly accept payments. These will be local large systemically important commercial banks, states, and several multinational players (Google, Apple, and Amazon). They will provide their applications as a service, which will include NFC payments, various QR codes, biometrics, and whatever else they come up with at this point.

POS terminals and classic acquiring will not disappear tomorrow. The payment industry is extremely conservative and new payment methods, with all their convenience and variety, will be introduced for decades. Many countries are just launching contactless projects, QR is actively used only in Asia, where there is a strong growth in sales of POS machines. But the direction of movement is not in doubt and the sale of Ineginco Worldline at the price of Plaid is a vivid example of this.

Cards no longer needed or biometrics

With physical plastic, the situation is no less dramatic. It just so happens that plastic is no longer needed. This specter is based on the so-called ingrained “card experience”, people's conservatism, inertia and uneven development of countries. But Henry Ford has been producing cars in his factories for 10 years, Elon Musk launched his Tesla into space — progress is inexorable and nothing can save the horses. You can see the desperate attempts of individual participants in the payment market to find, in fact, some new use for the disappeared artifact. Which doesn't exist.

The plastic card was too late. For example, VISA is already 62 years old, and the first card was issued by Long Island Bank back in 1951, when Stalin was still alive! The map has certainly gone through a major technological evolution over the years. After the magnetic stripe, Chip&PIN appeared, which, by the way, was not implemented very quickly in the world. And then it was time for contactless cards.

Бесконтактную карту можно просто приложить к терминалу, для совершения оплаты. Цифры на ней теперь нужна разве что для e-commerce, а магнитную полосу продолжают делать из уважения к истории (ради поддержки fallbacks?).

However, the contactless card reached its peak in the late iPhone era. Suddenly it turned out that everyone has a fancy smartphone in their pocket, but not everyone has a bank account. Inclusivity. New word. This was most quickly understood in China, which was very late in the development of the fintech sector from Western countries, but, accordingly, did not have the legacy technologies of the past on its balance sheet. AliPay and WeChat.Pay has completely captured the payment market, making the traditional UnionPay payment system just an addition. Why do I need a bank card if it's convenient to pay without it?

First mobile - first card from BBVA Bank with dynamic CVV from the website nfcw.com

But the Chinese experience is not for everyone. In many countries, the payment card based on the VISA and Mastercard infrastructure has become so entrenched that the victory of QR wallets is still not obvious, even despite numerous pilot projects and the penetration of Asian giants. In the same Switzerland, for example, there are no problems with opening a bank account for a huge population from the rural hinterland in the understanding of India and China. But still, it is convenient to pay by phone, and the answer of VISA and Mastercard is tokenization-MDES and VTS services that allow you to issue an existing card as a” token " inside your smartphone. It is fast, cheap and convenient for the buyer. You don't need a real card anymore — you can pay with a bracelet, ring, or watch. Spanish bank BBVA has already launched exclusively digital card products in the spirit of the digital first concept.

A little less obvious is that it also makes no sense to show her photo on the phone screen — it's just a curtsy to a bygone era, a symbol of continuity and nothing more. There is no card, no chip on the card and, accordingly, there is no need to enter a PIN code anymore — smartphone manufacturers Samsung and Apple will be able to authenticate you by fingerprint or head shape.

The card disappeared, shrinking to a QR square or digital token inside keychains and watches. And this has very serious consequences. For example, e-commerce has traditionally been built around entering card details in a payment form. But if there is no card anymore, then what should I enter and where? The simplest answer is that you don't need to enter anything other than a one-time password in the best traditions of SCA (strong customer authentication). Your payment details are already stored in Apple's systems.Pay, Google.Pay or Sber. Pay and almost everything is done to ensure that the purchase takes place in one touch. This is convenient.

Map makers, in a desperate attempt to save something that no longer exists, are introducing a whole series of innovations — a map with a built-in fingerprint, a vertical map, a map without a number, and an environmental map made from recyclable materials. The idea is to increase the customer's enjoyment of using the card. To make it pleasant to hold it in your hands. Stylish, expensive and technologically advanced. But in fact, it still tastes “retro", and there is nothing more eco-friendly than a QR code or token. These are all small niche solutions that will not radically change the picture and reverse the trend towards the destruction of plastic.

What will happen next? Now to pay Apple.Pay just needs to show your face to the camera of your smartphone. The development of this idea is authentication on the part of the merchant. This is exactly what has been done in China for several years. National biometric databases, roaming between regions, and biometric authentication on the merchant's side are logical, convenient, and cheap for all participants in the process.

Banks are no longer needed or Embedded Finance

Commoditization of payment processing, interference of central banks in payment services directly, identical product lines and, as a result, intense competition, rapid growth of fintech companies and, of course, open banking under the flags of PSD2-like directives. It would seem that it could not be worse, but then there is a knock from below — technology companies have arrived. Samsung, Google, Huawei, Amazon, Apple, Uber and countless smaller organizations began to actively enter the financial services market, not wanting to allow other companies to access their users and, moreover, pay a significant percentage for service.

Today, it is absolutely unclear how the service of banks will be better than the same service provided by a large supermarket chain that has received a banking license. Why would their mobile app be worse? If it turns out that the only difference is only in historically serious barriers to entry to the market, then we are waiting for serious changes. No one likes intermediates that take more money than they add value to the value chain.

It doesn't look like the “supermarkets” will replace the banks completely. They will take their significant share, but their advantage will also be the same limitation-a loyal audience. In addition, people tend to choose simpler solutions — twenty different tokens and wallets in a mobile device-clearly not about this.

Using NFC from the site nfcw.com

You can also observe the ongoing merger of the payment world and the usual everyday infrastructure. It is already difficult to find a vending machine where the POS terminal is not built in, or at least not stuck on the outside. In urban transport systems, a new project starts almost every day, which allows you to use tokenized cards (mobile phone) for payment, applying them to conventional mounted terminals. Urban transport, such as bicycles or electric scooters, is available with the possibility of contactless payment by card, at least via QR.

In the post-PSD2 world, there are a relatively small number of banks that deal only with service functions for managing user accounts, while all other operations are performed either by the state or by a swarm of fintech organizations that collide on marketplaces and compete under standardized conditions. People will choose between product ecosystems or mobile banking interfaces. It is possible that large companies will make banking services just part of a wider subscription — 10% discount on taxi and here you will also get preferential terms for financial management. The focus will be on functionality and convenience for the end user. Initiatives like managing your personal finances from Excel will become the norm.

Embedded-finance is an opportunity to conveniently and quickly part with money at any time and in any place. A concept that can be called “pay and live". There is no longer any need for POS terminals or physical plastic — everything has been converted to digital form. In essence, we are a step away from the payment method from the TV series Altered Carbon, where the main character simply spat on the sensor.

(c) https://andreifrolov.medium.com/эволюция-платежных-технологий-20-хх-a5c56579055e