Carding Forum

Professional

- Messages

- 2,788

- Reaction score

- 1,323

- Points

- 113

How credit ratings are arranged in the countries with the strongest economies in the world, what are their differences and similarities

What is the difference between the credit rating in the United States and Britain.

Credit score is a system for assessing the creditworthiness of a consumer of financial services. It affects any application that is submitted for various types of loans: from loans for the purchase of goods, real estate to credit cards. If in Ukraine a low credit rating affects the likelihood of getting the next loan, then in other countries, for example, the UK, a consumer with a bad credit history may be refused even a home rental. How credit ratings work in countries with the strongest economies in the world, what are their differences and similarities - read further in the PaySpace Magazine article.

Although the credit scoring systems in the UK and the United States are similar in many ways, they have several significant differences, notes the financial company Self Financial. This is in part due to different data protection laws and what information credit bureaus have access to.

In the UK, lenders and credit bureaus identify individuals using information from the voter list. Such a register contains personal information about all citizens registered to vote in an election. It includes name, address, date of birth and ballot number and is used to determine which constituency a citizen is in and where to send ballots.

In the United States, the Social Security Number (SSN) is used instead of voter list data, a nine-digit code assigned to US citizens and residents. SSN is a unique identifier that is often required for employment, in banks for opening accounts and issuing loans, renting apartments, and also when providing medical services.

Credit bureaus in the US and UK

The main offices in the United Kingdom and the United States are Experian, Equifax and TransUnion. Despite the fact that these are the same companies, they do not share information about the borrower's credit history with each other.

In both countries, credit bureaus collect information about credit history and credit behavior, as well as personal information about the borrower. However, this is where the similarities end. The way bureaus interact with lenders and provide them with information is different in the United States and Britain. In particular, the biggest difference concerns credit scoring - how it is calculated and used.

How credit scoring works in the UK

In Britain, due to bad credit history, they may refuse to rent a home.

In the UK, lenders often have their own credit ratings based on their own criteria and calculations, and do not use credit bureau ratings. At the same time, it is through the scoring of credit bureaus that consumers can find out about their rating.

Note. In February 2020, UK neobank Monzo and the Royal Bank of Scotland (RBS) announced that their customers will now be able to check loan approvals by tracking their credit scores for free through their mobile banking app. To assess creditworthiness, banks use data from the TransUnion credit agency.

Experian clarifies that in the UK, each credit bureau can use different information about the borrower to compile a rating and evaluate it in different ways. So, some data can be assessed positively in one company, and negatively in another. Because of this, the credit rating may differ from one agency to another.

“There is no universal credit rating, as results from different sources are calculated using different formulas and criteria. They will also be rated on different scales, for example, from 1 to 700 or from 1 to 1000. That is why you can get 500 on one scale and 700 on another, even if the information provided is the same, ”says Equifax.

In addition to different approaches to calculating the rating, some UK agencies, such as TransUnion, also distinguish between credit rating and credit score. However, most credit bureaus use these terms as synonyms.

The UK TransUnion Credit Rating System indicates the type of credit risk a borrower may pose to lenders based on the following factors:

British credit bureau Equifax also takes into account the following information:

How the credit rating works in the USA

Several types of credit scoring are used in the United States (including various versions of the FICO and VantageScore), with all major systems using a scale ranging from 300 to 850 points. To make decisions about granting a loan, the scoring of one of the credit bureaus is usually used. The most popular model is FICO, which is used by approximately 90% of American lenders.

As noted by loan officer Barry Paperno, lenders make about a billion loan decisions annually based on FICO scoring.

An example of calculating a credit rating according to FICO.

The UK credit rating takes into account the timeliness and completeness of utility and rental payments. This information works bilaterally - if you have a bad credit history, the consumer may be denied renting a home, even if he provides a certificate of employment and solvency. James, a 32-year-old resident of Bristol, told PaySpace Magazine that due to poor credit, local landlords can only rent out their homes six months in advance.

In the United States, this data is usually not taken into account. Scoring is mainly calculated based on five factors:

Lies idle: attitudes towards old credit cards in the USA and Britain

How credit cards affect the assessment of creditworthiness.

In the UK, credit bureaus evaluate the existence of old credit accounts differently. Equifax (UK) and TransUnion (UK) advise closing all unused credit cards, while Experian (UK) encourages keeping cards free of debt, as this has a positive effect on scoring.

In the States, regardless of the valuation model or bureau, experts agree that the borrower should, if possible, keep old accounts open, since the length of the average credit history is 15% of the FICO credit rating.

The presence of a high credit limit compared to the amount of the loan used in the United States is considered a positive factor, while in the UK a large limit is perceived negatively.

Credit ratings exclude income and savings

Experian (UK) clarifies in its consumer guide that the agency does not take into account income, savings, employment and taxes when calculating the rating, as this information is not included in the credit history. However, lenders can ask about this as clarifying questions and then use the consumer's answers to make the final decision on the loan.

The same goes for credit scoring in the United States. While this does not affect credit history in any way, the general rule in the United States is to keep the debt-to-income ratio below 30%. Otherwise, lenders may feel that the borrower has too much debt to pay off the debt on time.

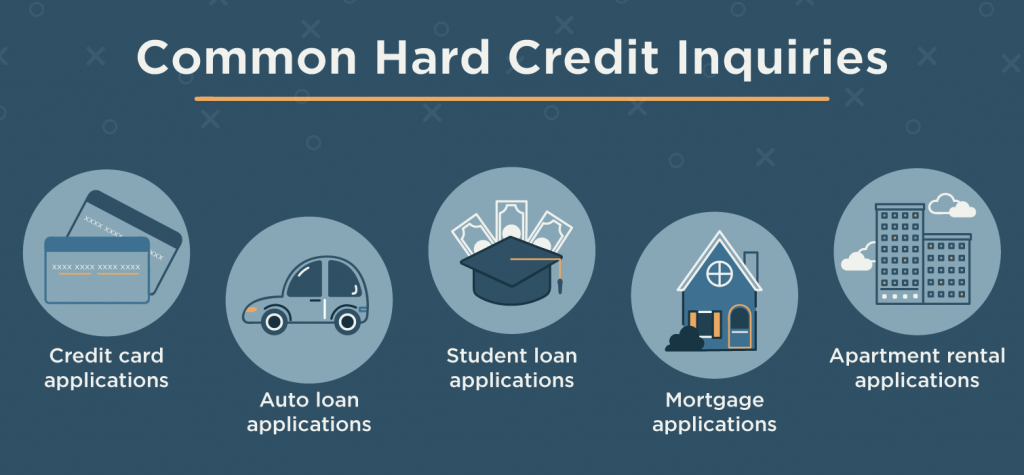

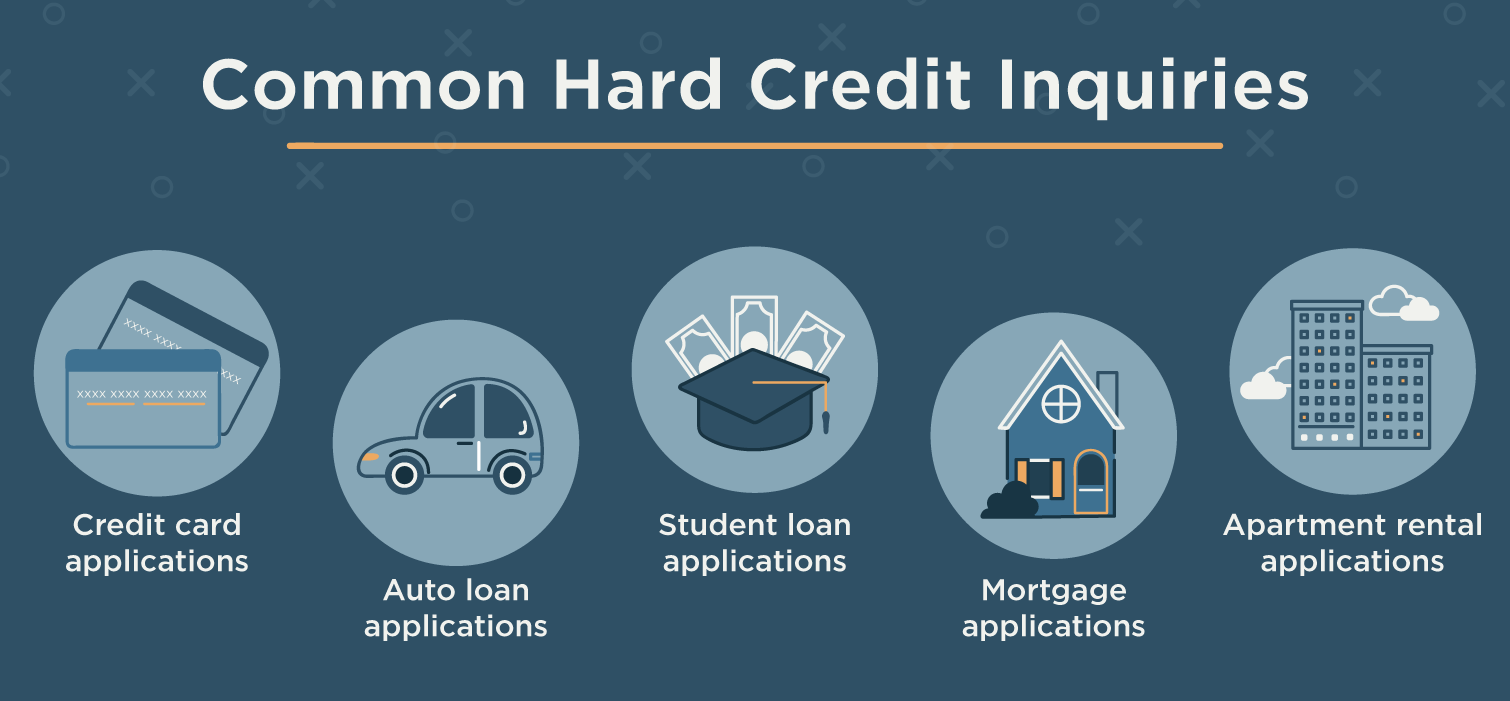

Hard and soft: the impact of the number of requests on credit history

Each new loan application lowers the credit rating.

In the United States and the United Kingdom, requests for the credit history of a borrower applying for a loan affect the rating in the same way. There are two types of such requests - hard inquiry and soft inquiry.

That being said, in both countries, the consumer must give their consent before the company can conduct a thorough credit check.

Financial partners and financial guarantors

In the UK, a financial partner is a person with whom the consumer has a common bank or credit account, be it a spouse, partner, friend or relative.

As Experian (UK) reports, a financial partner's credit history does not affect a consumer's credit history, but lenders can view it when a borrower applies for a new or renewal of an old loan. This is due to the fact that the financial situation of a financial partner can affect the ability of the borrower to repay the debt on time.

“Lenders can take into account the financial behavior of a financial partner, even if you apply for a new loan yourself. If your partner has a bad credit history, this may affect your ability to get a new loan agreement, ”says Equifax (UK).

In the United States, a co-debtor is the one with whom you sign an agreement on obtaining a loan: for the purchase of a car, real estate, etc. In this case, for the issuance or renewal of the loan, the lender will only take into account your general credit accounts, and not the overall financial behavior of the co-signers.

PAYSPACE MAGAZINE HELP

A credit rating is a way to assess how solvent a person is trying to borrow money from a bank or other financial institution. Traditionally, financial institutions determined the creditworthiness of their customers based on data from the credit bureau or their own files about the borrower, assessing the current credit history, income level and the presence of consumer debt. However, today these data are insufficient. Therefore, lenders are increasingly using alternative sources for assessing solvency based on the Big Data trend: the accumulation and correct use of large amounts of information allows you to learn more about a potential borrower than his bank account. How technology is changing modern lending - follow the link in PaySpace Magazine.

What is the difference between the credit rating in the United States and Britain.

Credit score is a system for assessing the creditworthiness of a consumer of financial services. It affects any application that is submitted for various types of loans: from loans for the purchase of goods, real estate to credit cards. If in Ukraine a low credit rating affects the likelihood of getting the next loan, then in other countries, for example, the UK, a consumer with a bad credit history may be refused even a home rental. How credit ratings work in countries with the strongest economies in the world, what are their differences and similarities - read further in the PaySpace Magazine article.

Credit ratings in the US and UK: what are the differences and similarities

What is the difference between credit ratings in the United States and Britain. Photo: iflexion.comAlthough the credit scoring systems in the UK and the United States are similar in many ways, they have several significant differences, notes the financial company Self Financial. This is in part due to different data protection laws and what information credit bureaus have access to.

How is the identification of the borrowerA good credit rating gives you access to high credit card limits, low mortgage rates and other types of loans, potentially saving you a lot of money. Poor rating - to loan refusals

In the UK, lenders and credit bureaus identify individuals using information from the voter list. Such a register contains personal information about all citizens registered to vote in an election. It includes name, address, date of birth and ballot number and is used to determine which constituency a citizen is in and where to send ballots.

In the United States, the Social Security Number (SSN) is used instead of voter list data, a nine-digit code assigned to US citizens and residents. SSN is a unique identifier that is often required for employment, in banks for opening accounts and issuing loans, renting apartments, and also when providing medical services.

Credit bureaus in the US and UK

The main offices in the United Kingdom and the United States are Experian, Equifax and TransUnion. Despite the fact that these are the same companies, they do not share information about the borrower's credit history with each other.

In both countries, credit bureaus collect information about credit history and credit behavior, as well as personal information about the borrower. However, this is where the similarities end. The way bureaus interact with lenders and provide them with information is different in the United States and Britain. In particular, the biggest difference concerns credit scoring - how it is calculated and used.

How credit scoring works in the UK

In Britain, due to bad credit history, they may refuse to rent a home.

In the UK, lenders often have their own credit ratings based on their own criteria and calculations, and do not use credit bureau ratings. At the same time, it is through the scoring of credit bureaus that consumers can find out about their rating.

Note. In February 2020, UK neobank Monzo and the Royal Bank of Scotland (RBS) announced that their customers will now be able to check loan approvals by tracking their credit scores for free through their mobile banking app. To assess creditworthiness, banks use data from the TransUnion credit agency.

Experian clarifies that in the UK, each credit bureau can use different information about the borrower to compile a rating and evaluate it in different ways. So, some data can be assessed positively in one company, and negatively in another. Because of this, the credit rating may differ from one agency to another.

“There is no universal credit rating, as results from different sources are calculated using different formulas and criteria. They will also be rated on different scales, for example, from 1 to 700 or from 1 to 1000. That is why you can get 500 on one scale and 700 on another, even if the information provided is the same, ”says Equifax.

In addition to different approaches to calculating the rating, some UK agencies, such as TransUnion, also distinguish between credit rating and credit score. However, most credit bureaus use these terms as synonyms.

The UK TransUnion Credit Rating System indicates the type of credit risk a borrower may pose to lenders based on the following factors:

- Total debt

- Payment history (including late payments)

- Credit history length

- Bankruptcy and insolvency

- Borrower Information from Voter List

- Borrower's financial partners

British credit bureau Equifax also takes into account the following information:

- Credit history report

- History of payments on credit accounts

- Hard inquiry - when and how often a consumer applies for a loan (displayed in the credit history)

- Public records (voter list and district court decisions)

How the credit rating works in the USA

Several types of credit scoring are used in the United States (including various versions of the FICO and VantageScore), with all major systems using a scale ranging from 300 to 850 points. To make decisions about granting a loan, the scoring of one of the credit bureaus is usually used. The most popular model is FICO, which is used by approximately 90% of American lenders.

As noted by loan officer Barry Paperno, lenders make about a billion loan decisions annually based on FICO scoring.

An example of calculating a credit rating according to FICO.

The UK credit rating takes into account the timeliness and completeness of utility and rental payments. This information works bilaterally - if you have a bad credit history, the consumer may be denied renting a home, even if he provides a certificate of employment and solvency. James, a 32-year-old resident of Bristol, told PaySpace Magazine that due to poor credit, local landlords can only rent out their homes six months in advance.

In the United States, this data is usually not taken into account. Scoring is mainly calculated based on five factors:

- payment history

- Debt

- New loan applications and records in credit history about issued loans and applications (hard inquiries)

- Credit history length

- Types of credits used

Lies idle: attitudes towards old credit cards in the USA and Britain

How credit cards affect the assessment of creditworthiness.

In the UK, credit bureaus evaluate the existence of old credit accounts differently. Equifax (UK) and TransUnion (UK) advise closing all unused credit cards, while Experian (UK) encourages keeping cards free of debt, as this has a positive effect on scoring.

In the States, regardless of the valuation model or bureau, experts agree that the borrower should, if possible, keep old accounts open, since the length of the average credit history is 15% of the FICO credit rating.

The presence of a high credit limit compared to the amount of the loan used in the United States is considered a positive factor, while in the UK a large limit is perceived negatively.

Credit ratings exclude income and savings

Experian (UK) clarifies in its consumer guide that the agency does not take into account income, savings, employment and taxes when calculating the rating, as this information is not included in the credit history. However, lenders can ask about this as clarifying questions and then use the consumer's answers to make the final decision on the loan.

The same goes for credit scoring in the United States. While this does not affect credit history in any way, the general rule in the United States is to keep the debt-to-income ratio below 30%. Otherwise, lenders may feel that the borrower has too much debt to pay off the debt on time.

Hard and soft: the impact of the number of requests on credit history

Each new loan application lowers the credit rating.

In the United States and the United Kingdom, requests for the credit history of a borrower applying for a loan affect the rating in the same way. There are two types of such requests - hard inquiry and soft inquiry.

- Soft inquiry is a credit check as part of a data check that does not appear in the credit history. For example, a credit card issuer checks without the borrower's permission to see if they are eligible for certain credit card offers. Also, soft inquiry occurs when checking the Credit Karma credit scoring and receiving a certificate from work.

- Hard inquiry - checking credit history by a lender or credit card issuer to make a loan decision when applying for a mortgage, home loan or credit card. Shown in credit history.

That being said, in both countries, the consumer must give their consent before the company can conduct a thorough credit check.

Financial partners and financial guarantors

In the UK, a financial partner is a person with whom the consumer has a common bank or credit account, be it a spouse, partner, friend or relative.

As Experian (UK) reports, a financial partner's credit history does not affect a consumer's credit history, but lenders can view it when a borrower applies for a new or renewal of an old loan. This is due to the fact that the financial situation of a financial partner can affect the ability of the borrower to repay the debt on time.

“Lenders can take into account the financial behavior of a financial partner, even if you apply for a new loan yourself. If your partner has a bad credit history, this may affect your ability to get a new loan agreement, ”says Equifax (UK).

In the United States, a co-debtor is the one with whom you sign an agreement on obtaining a loan: for the purchase of a car, real estate, etc. In this case, for the issuance or renewal of the loan, the lender will only take into account your general credit accounts, and not the overall financial behavior of the co-signers.

PAYSPACE MAGAZINE HELP

A credit rating is a way to assess how solvent a person is trying to borrow money from a bank or other financial institution. Traditionally, financial institutions determined the creditworthiness of their customers based on data from the credit bureau or their own files about the borrower, assessing the current credit history, income level and the presence of consumer debt. However, today these data are insufficient. Therefore, lenders are increasingly using alternative sources for assessing solvency based on the Big Data trend: the accumulation and correct use of large amounts of information allows you to learn more about a potential borrower than his bank account. How technology is changing modern lending - follow the link in PaySpace Magazine.