Good Carder

Professional

- Messages

- 471

- Reaction score

- 353

- Points

- 63

The US legislative process is governed by the Constitution (primarily Article I), House and Senate rules, and precedents. It is complex, non-linear in practice, and most bills (over 90%) die in committee. The following provides a complete, step-by-step methodology, drawing from official sources like the House Office of the Legislative Counsel (HOLC) Guide to Legislative Drafting, How Our Laws Are Made (Congress.gov), Congressional Research Service (CRS) reports, and Congressional Budget Office (CBO) procedures.

Bills not reported are effectively dead unless discharged (rare).

CBO Process (Step-by-Step Algorithm):

Expanded Justification Elements (often in committee reports or sponsor materials):

CBO estimates are non-partisan and publicly available on CBO.gov.

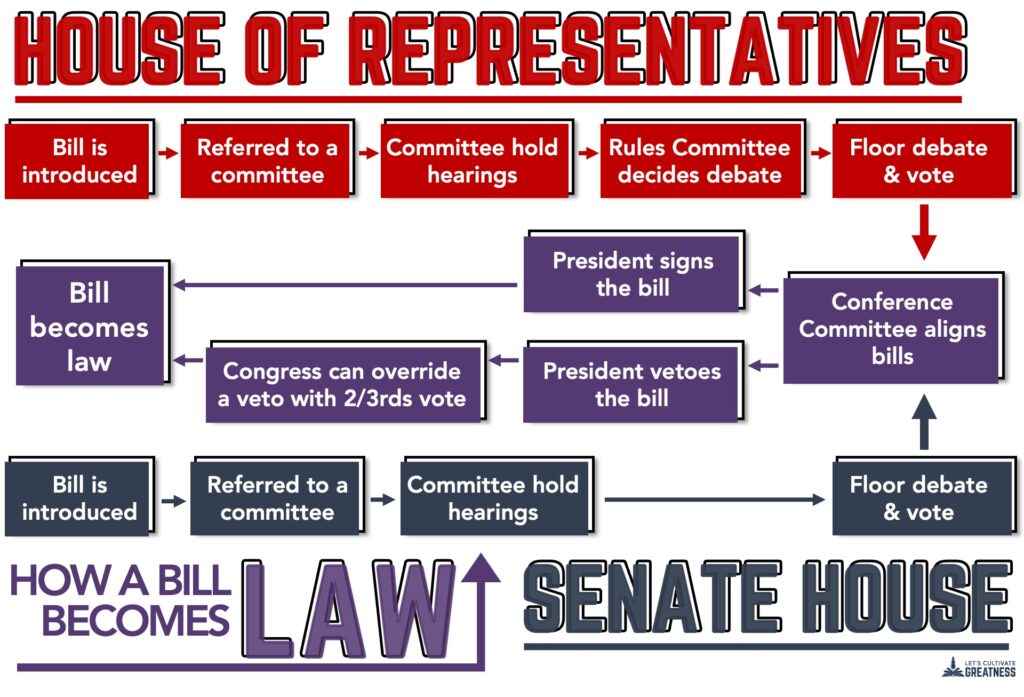

Complete Legislative Process Flowchart (visualized above; standard path shown in second image): Idea → Introduction → Committee (hearings/markup/report) → Floor (debate/vote) → Other Chamber → Conference (if needed) → Enrollment → President → Law (or veto/override).

Tips for Success: Build coalitions early; secure committee chair support; use budget reconciliation for partisan priorities (bypasses filibuster); anticipate CBO score impacts on rules. Track via Congress.gov (bill status, texts, reports).

This methodology is comprehensive but flexible — actual paths vary by politics, urgency, and procedure (e.g., suspension of rules). For drafting templates, see HOLC resources; for live tracking, use Congress.gov.

1. Preparation (Idea to Draft)

- Sources of Ideas: Constituents, lobbyists, executive branch (e.g., President's budget message), state legislatures (memorials), think tanks, or Members' own priorities. Ideas often stem from identified problems needing federal solutions (e.g., interstate commerce clause authority).

- Drafting Process:

- A Member (or staff) consults the House or Senate Office of the Legislative Counsel for professional drafting to ensure clarity, constitutionality, and consistency with existing law.

- Decide form: Bill (most common; becomes "An Act" after one-house passage) or joint resolution (for some matters like continuing appropriations or constitutional amendments). Avoid concurrent/simple resolutions unless non-binding.

- Key Conventions(HOLC style):

- Use "shall" for mandatory duties; "may" for permissive.

- Singular preferred for clarity.

- "Means" = exclusive definition; "includes" = non-exclusive.

- Amend existing law via precise instructions (outside quotes) + quoted new text (inside quotes).

- Detailed Structure of the Document Package (Bill Text): Bills follow a standardized format (HOLC template). A complete introduced bill package is primarily the bill text (printed by Government Publishing Office), plus sponsor's introduction statement in the Congressional Record. No formal "fiscal note" is required at introduction, but major bills often include informal justifications.

Full Structure (Freestanding Bill Example):- Long Title (Caption): "A BILL [or An Act] To [describe purpose in one sentence]."

- Enacting Clause (required): "Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled,"

- Section 1: Short title (e.g., "This Act may be cited as the '[Short Title] Act of [Year].'").

- Findings/Purposes/Preambles (optional; use sparingly to avoid ambiguity): "Whereas..." or policy declarations.

- Definitions (often early or in a dedicated section): Precise, using "means" or "includes."

- Operative Provisions(core body; organized per general template):

- Main rule/general authority.

- Exceptions.

- Special rules (different treatment).

- Transitional rules.

- Other provisions (e.g., enforcement, penalties, reporting requirements).

- Authorization of appropriations (if needed; avoid vague "such sums as may be necessary").

- Effective date (defaults to enactment unless specified; apply to "amendments made by this Act").

- Higher-Level Organization (for complex/omnibus bills): Division → Title → Subtitle → Chapter → Part → Subpart → Section → (a) subsection → (1) paragraph → (A) subparagraph → (i) clause → (I) subclause.

- Technical Elements: Table of contents (if long); savings clauses; severability; conforming amendments.

- Amending Existing Law: Use "strike" / "insert" or full quotes for precision (Ramseyer/Cordon rules later require showing changes in reports).

- Legal/Technical Documentation at This Stage: Draft bill text only. Executive communications (if used) may attach proposed language.

2. Introduction

- House: Sponsor drops bill in the "hopper" (rostrum box) during session. Assigned H.R. number; referred by Speaker/Parliamentarian to committee(s) with jurisdiction (possible multiple referrals).

- Senate: Presented to clerk or on floor; assigned S. number; referred by Parliamentarian.

- Cosponsors: Added post-introduction (unlimited in House until committee action).

- Document Package: Printed bill + Congressional Record entry (sponsor's remarks). Bill is public immediately via Congress.gov.

3. Committee Review (Most Bills Die Here)

- Referral: To standing committee(s) (e.g., Ways & Means for tax).

- Hearings: Public (announced 1 week ahead); witnesses testify; transcripts printed.

- Markup: Amendments voted on; "clean bill" possible.

- Reporting: Committee votes to report favorably (with/without amendments). Quorum required; no proxy voting in House.

- Key Documentation(expands the package):

- Committee Report (e.g., H. Rept. 119-XXX): Purpose; section-by-section analysis; changes in existing law (Ramseyer/Cordon); CBO cost estimate; constitutional authority statement; unfunded mandates statement; vote tally; minority/supplemental views; earmark list (or "none").

- Hearings record.

- Agency views/GAO reports (requested).

Bills not reported are effectively dead unless discharged (rare).

4. Expanded Financial and Economic Justification Algorithm (CBO Scoring)

Bills with budgetary impact require CBO cost estimates upon full committee approval (Congressional Budget Act of 1974). This is the formal "financial/economic justification" — advisory but critical for rules, debate, and scoring against budget resolutions.CBO Process (Step-by-Step Algorithm):

- Receive Bill Language: CBO analyzes exact text post-committee markup.

- Establish Baseline: Compare to current law projections (CBO baseline: 10-year window for spending/revenues; incorporates economic assumptions).

- Provision-by-Provision Analysis:

- Identify direct spending, revenues, or discretionary effects.

- Use data/models from agencies, historical trends, economic literature.

- Incorporate behavioral responses (e.g., how people/firms react).

- Estimate intergovernmental/private-sector mandates (Unfunded Mandates Reform Act).

- Quantify Uncertainty: Explicitly note ranges, assumptions, and limitations in "basis of estimate."

- Dynamic Scoring (for major bills): Optional but used for large tax/spending proposals; includes macroeconomic feedback (e.g., GDP growth effects).

- Output: Formal letter/report with tables (outlays, revenues, deficit impact) + narrative. Includes 5- and 10-year totals.

Expanded Justification Elements (often in committee reports or sponsor materials):

- Cost-benefit analysis (informal).

- Regulatory impact (if applicable).

- Economic modeling (e.g., JCT for tax bills).

CBO estimates are non-partisan and publicly available on CBO.gov.

5. Floor Action

- House: Rules Committee issues special rule (debate limits, amendments). Committee of the Whole for amendments; then full House vote (simple majority). Electronic voting.

- Senate: Motion to proceed; unlimited debate (filibuster possible; cloture at 60 votes). Unanimous consent agreements common. Simple majority passage.

- Documentation: Congressional Record (debate, amendments, votes).

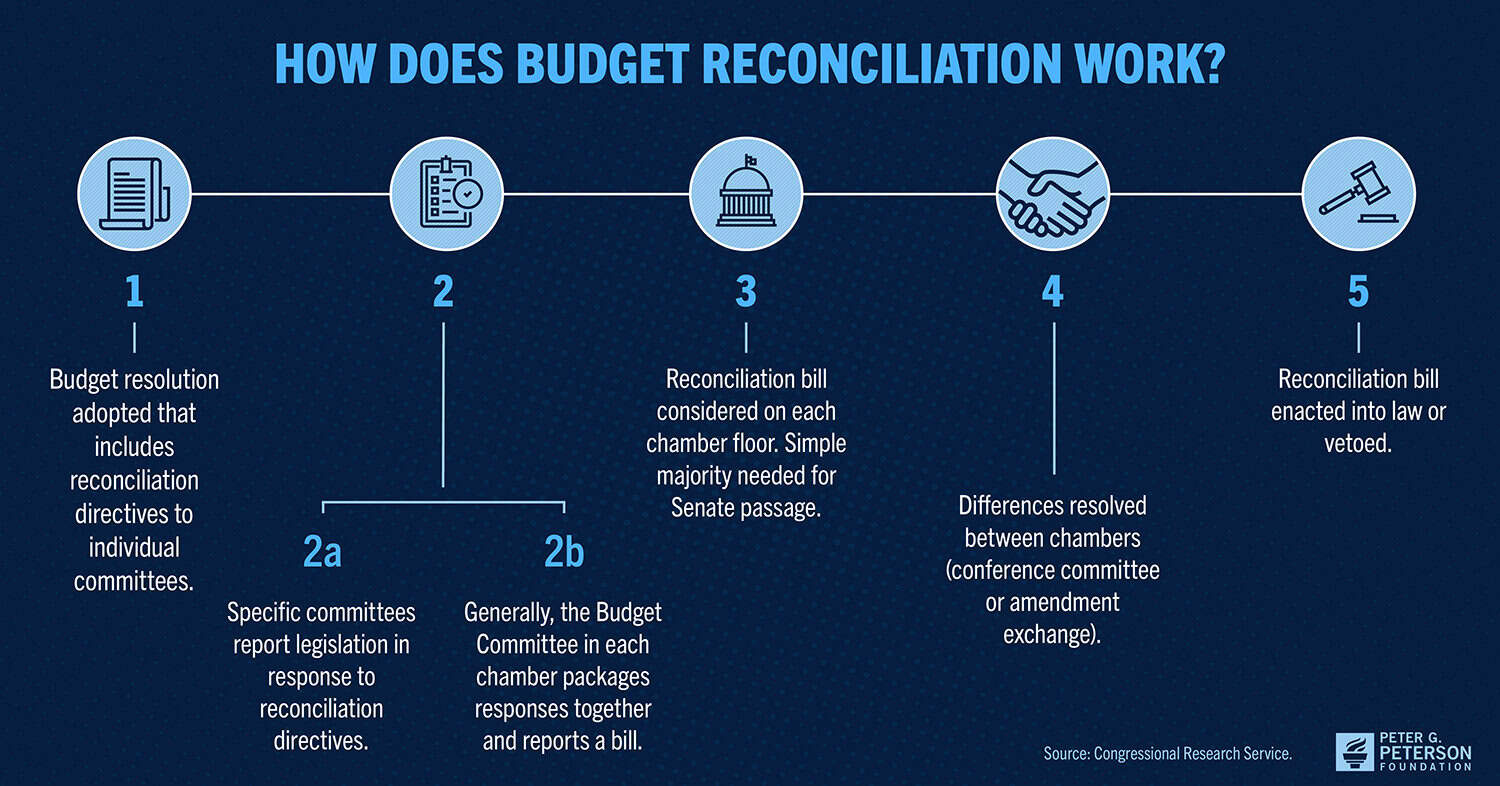

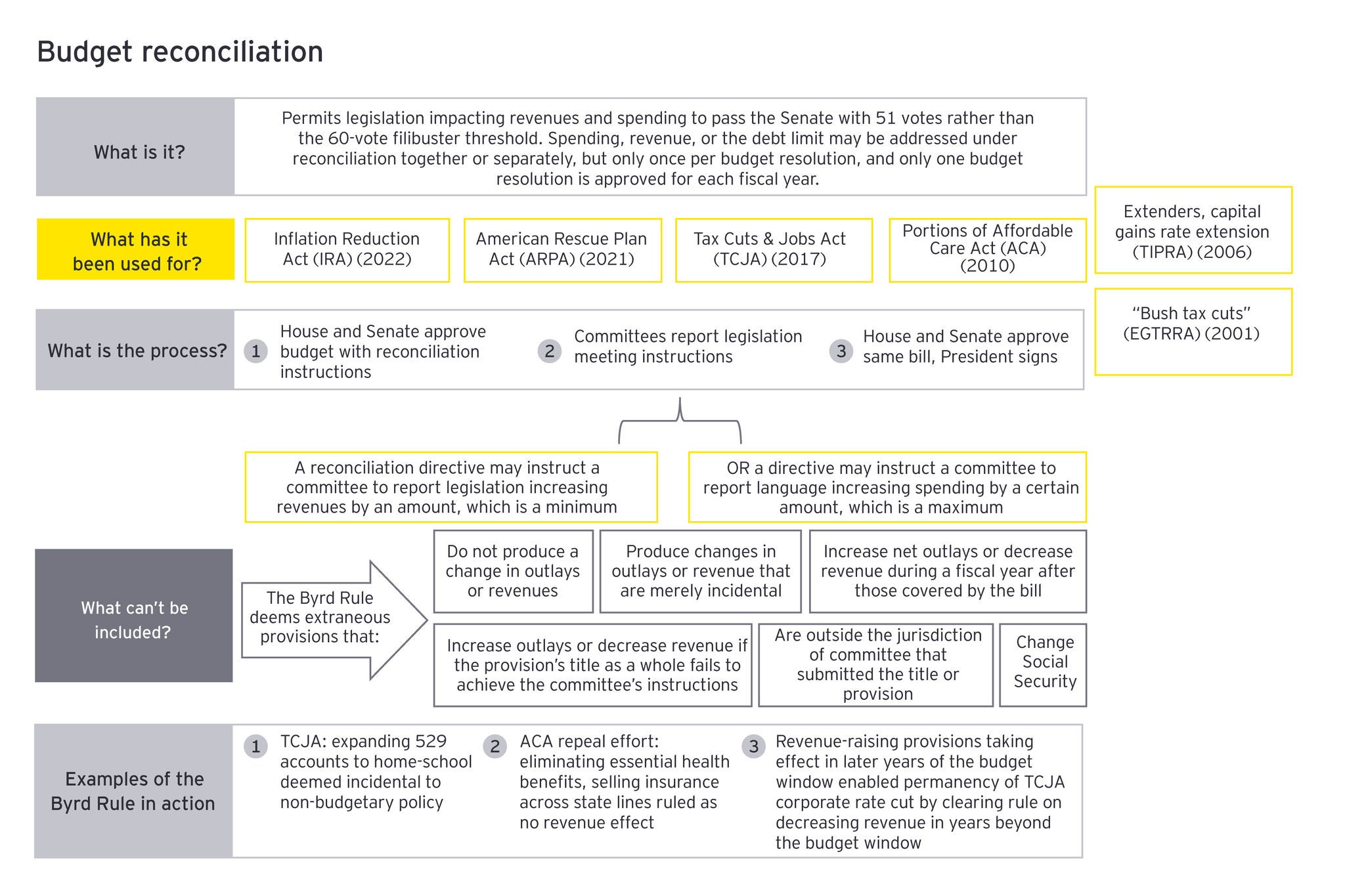

6. Other Chamber + Reconciliation

- Bill goes to second chamber (mirrors process).

- If versions differ: Concurrence or conference committee (conferees negotiate; produces conference report + joint explanatory statement). Both chambers vote up-or-down on report.

- Documentation: Engrossed/enrolled bill; conference report (with earmarks).

7. Presidential Action + Enrollment

- Enrolled bill (parchment copy) presented to President.

- Options: Sign → Public Law (e.g., P.L. 119-XXX); veto (override by 2/3 both houses); pocket veto (if Congress adjourns); or becomes law after 10 days (if in session).

- Final Documentation: Slip law → Statutes at Large → U.S. Code (codified).

Complete Legislative Process Flowchart (visualized above; standard path shown in second image): Idea → Introduction → Committee (hearings/markup/report) → Floor (debate/vote) → Other Chamber → Conference (if needed) → Enrollment → President → Law (or veto/override).

Real-World Examples

- Affordable Care Act (ACA, P.L. 111-148, 2010): Introduced as H.R. 3590 (Senate vehicle). Extensive committee hearings/markups in both chambers. House passed its version; Senate used reconciliation (51-vote threshold) to finalize after Scott Brown election. CBO scored extensively (deficit reduction claimed). Conference avoided via reconciliation. Signed by President Obama after year-long process. Demonstrates committee work, floor amendments, and budget tools.

- Recent Simpler Example: Many infrastructure or appropriations bills follow the full path but use omnibus packaging and unanimous consent for speed.

Tips for Success: Build coalitions early; secure committee chair support; use budget reconciliation for partisan priorities (bypasses filibuster); anticipate CBO score impacts on rules. Track via Congress.gov (bill status, texts, reports).

This methodology is comprehensive but flexible — actual paths vary by politics, urgency, and procedure (e.g., suspension of rules). For drafting templates, see HOLC resources; for live tracking, use Congress.gov.